Assessing the strength of the recent residential real estate expansion

Published as part of the Financial Stability Review, November 2021.

Credit-fuelled residential real estate booms can pose major risks to financial stability. Residential real estate (RRE) booms and busts have frequently been associated with deep recessions and financial crises, especially when the RRE boom is fuelled by debt.[1] The real estate bubble in the United States ahead of the global financial crisis (GFC) is possibly the most prominent recent example. In a boom, a feedback loop of rising prices and rising credit growth can result in a later correction of overvalued RRE prices affecting the economy and financial system through several channels. A collapse in RRE prices can weigh on household expenditure via wealth effects and/or confidence. High household indebtedness can further contribute to a reduction in consumption and can lead to defaults on loans if debts prove unsustainable. Investment and corporate loans can be impaired if the RRE price boom has been accompanied by a twin construction boom. Finally, the bursting of a real estate bubble can severely affect the credit supply and amplify the downturn as the value of available collateral shrinks and losses impair banks’ intermediation capacity.[2]

Euro area RRE markets have seen a continued expansion throughout the pandemic, but how concerning are these developments compared with the past? This box compares recent RRE developments at the euro area level with the period ahead of the GFC, compiling indicators into risk ratings across three dimensions: (i) price pressures, (ii) lending dynamics, and (iii) household balance sheet strength.[3] The analysis is complemented by an assessment of lending standards.

First, house price dynamics and overvaluation are already at levels similar to those observed at the height of the pre-GFC cycle in 2007. The average risk rating across price indicators, which covers four indicators related to real RRE price dynamics and overvaluation estimates, stands close to the pre-GFC levels of 2007 and well above the levels of 2005 (see Chart A, panel a). The recent increase in the average risk rating reflects changes in the overvaluation estimates, which are currently above the levels observed in 2007 for the euro area aggregate.

Second, vulnerabilities stemming from mortgage lending developments are currently below pre-GFC levels, but they are slowly increasing and are heterogeneous across countries. The average risk rating across lending indicators, which summarise information from three measures of mortgage loan dynamics and mortgage loan spreads, indicates low risk overall (see Chart A, panel b). This is in stark contrast to the pre-GFC period in 2005 and 2007 when the risk rating stood at higher levels. While the analysis of aggregate credit dynamics is reassuring from a financial stability perspective, there are several euro area countries where annual household mortgage credit growth is already above 7% and accelerating.

Chart A

Price developments are at levels similar to those observed at the height of the pre-GFC cycle in 2007, but lending developments paint a more benign picture

Sources: ECB, Eurostat and ECB calculations.

Notes: The lower and upper hinges correspond to the 25th and 75th percentiles. The upper/lower whisker extends from the hinge to the 90th/10th percentile. 2021 data are from the first quarter. Panel a: the average risk rating across price indicators covers the average three-year real growth of house prices, residential price index relative to trend, the house price-to-income ratio, and overvaluation estimates based on an econometric model (inverted demand equation). In 2014 all 19 euro area countries are covered; in 2021, 2007 and 2005 some countries are missing due to data unavailability (Cyprus in 2021; Latvia, Lithuania, Luxembourg, Malta, Slovenia and Slovakia in 2007; Estonia, Latvia, Lithuania, Luxembourg, Malta, Slovenia and Slovakia in 2005). Panel b: the average risk rating across lending indicators covers the average three-year real growth of loans to households for house purchase, deviation of the loans to households for house purchase from the trend, and household loan spread. In 2021 all 19 euro area countries are covered, in earlier years some countries are missing due to data unavailability (Cyprus, Estonia, Latvia, Lithuania, Malta and Slovakia in 2007; Cyprus, Estonia, Latvia, Lithuania, Malta, Slovenia and Slovakia in 2005). The data unavailability inevitably results in an unbalanced sample, which might potentially affect the distribution at different points in time.

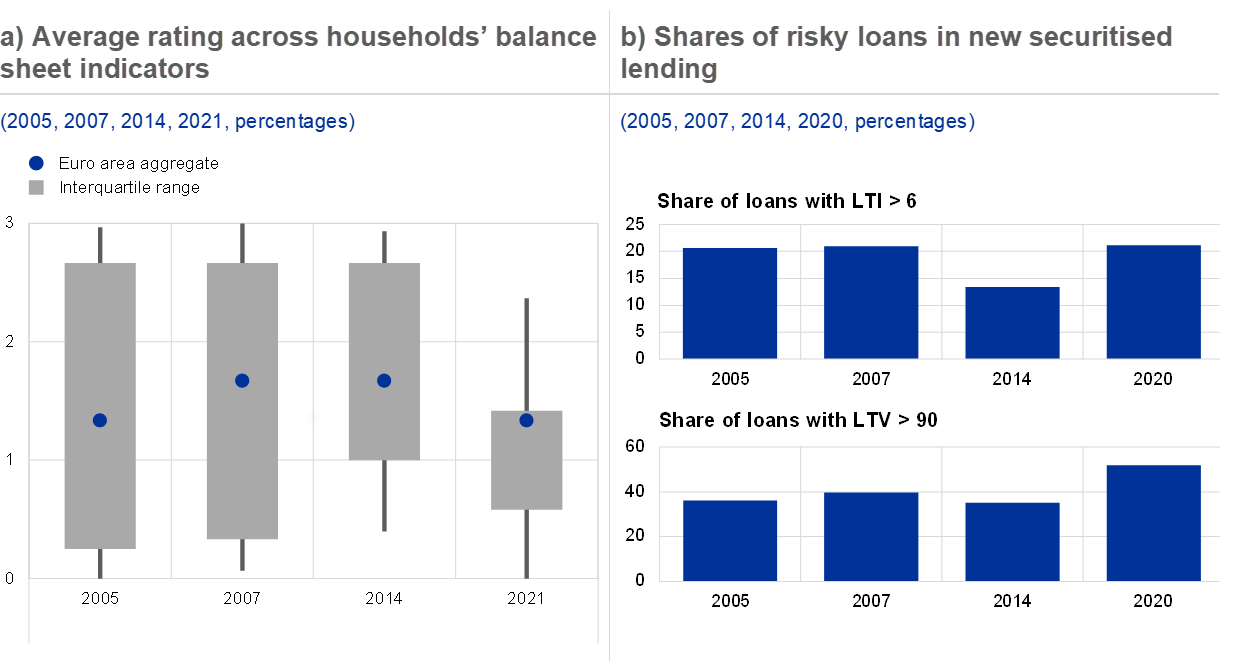

Third, household balance sheet vulnerabilities appear to be lower than in the pre-GFC period. Collectively, household debt levels and debt service burdens currently signal similar risk to 2005 and lower risk on average than in 2007 (see Chart B, panel a). In addition, although during the pre-GFC period a quarter of countries had a high-risk signal, hardly any countries currently have a risk signal above medium, which is reassuring from a financial stability perspective. However, this more benign picture also reflects households’ low borrowing costs, which points to risks stemming from possible tighter financing conditions in the future.[4]

Fourth, the risk profile of new loans for house purchase seems to be at similar levels to the pre-GFC period, according to some parameters.[5] Strong price and lending increases are particularly concerning if they are coupled with a deterioration of the risk profile of loans as measured, for example, by the loan-to-value (LTV) and the loan-to-income (LTI) ratios.[6] The share of loans with LTV ratios above 90% in newly originated loans currently appears to be higher than in the pre-GFC boom (see Chart B, panel b). Shares of loans with LTI ratios above 6, meaning with households borrowing over six times their annual disposable income, are currently at roughly the same level as in 2007. However, as a lower borrowing cost implies increased housing affordability, for a given maturity of new loans, their debt service burdens may currently be lower than pre-GFC.

Chart B

Household balance sheet vulnerabilities are at slightly lower levels than pre-GFC, but current lending standards seem to be at similar levels

Sources: Panel a: ECB, Eurostat and ECB calculations. Panel b: European Datawarehouse GmbH (EDW) and ECB calculations.

Notes: Panel a: the average risk rating across household balance sheet indicators covers household debt in relation to disposable income, household financial assets in relation to debt and the aggregate debt-service-ratio of households. The lower and upper hinges correspond to the 25th and 75th percentiles. The upper/lower whisker extends from the hinge to the 90th/10th percentile. 2021 data are from the first quarter. In 2021 all 19 euro area countries are covered; in earlier years some countries are missing due to data unavailability (Cyprus, Estonia, Latvia, Lithuania, Luxembourg, Malta and Slovakia in 2007 and 2014; Cyprus, Estonia, Latvia, Lithuania, Luxembourg, Malta, Slovenia and Slovakia in 2005). The data unavailability inevitably results in an unbalanced sample, which might potentially affect the distribution at different points in time. Panel b: data available for Belgium, Germany, Spain, France, Italy, the Netherlands and Portugal, total weighted by GDP. Chart uses information on securitised mortgage loans only (potentially resulting in selection bias) which may not accurately represent national mortgage markets.

Overall, vulnerabilities in euro area RRE markets appear more benign than during the pre-GFC period, but build-ups of medium-term vulnerabilities warrant close monitoring and potentially policy consideration. On aggregate, mortgage lending is less exuberant and households’ balance sheets seem more resilient currently than in the pre-GFC period. In addition, despite the pandemic, the euro area banking system is more resilient compared with the pre-GFC period, reflecting improved quality of supervision, stronger capital positions and, in some countries, measures that already address real estate risks. Nevertheless, the continued build-up of vulnerabilities in residential real estate markets calls for close monitoring and possible macroprudential measures.

- See Jordà, O., Schularick, M. and Taylor, A., “Leveraged bubbles”, Journal of Monetary Economics, Vol. 76, 2015.

- Falling house prices result in a lower value of available collateral, which in turn means lower credit supply – the “collateral channel of the wealth effect”. The strength of this channel differs across countries due to specificities of residential real estate markets and housing loan contracts.

- Each composite risk indicator is constructed as a simple average of various underlying indicators, which are first transformed into a discrete risk rating ranging from 0 to 3 depending on whether the indicator breaches certain risk thresholds (the rating scale is: 0 = no risk, 1 = low risk, 2 = medium risk, 3 = high risk). These thresholds are guided by evidence from early warning models and the historical distribution of the indicators. See Working Group on Real Estate Methodologies, “Methodologies for the assessment of real estate vulnerabilities and macroprudential policies: residential real estate”, ESRB, 2019.

- This is especially relevant for households borrowing at variable rates, with interest rate fixation periods shorter than the maturity of the loan; or for households that will need to refinance loans at maturity.

- Against the backdrop of the scarcity of data on lending standards this box uses data from residential mortgage loans that have been securitised. See European Datawarehouse GmbH. The analysis in the box assumes that the observed trends in lending standards in securitised mortgages are mirrored in the loans remaining in the bank balance sheets. The literature on the credit quality of securitised loans is not conclusive. Some studies show that securitised loans could be of lower quality than loans retained in banks’ balance sheet (see Keys, B., Mukherjee, T., Seru, A. and Vig, V., “Did Securitization Lead to Lax Screening? Evidence from Subprime Loans”, The Quarterly Journal of Economics, Vol. 125, Issue 1, 2010, pp. 307-362). Other studies find the opposite (see Albertazzi, U., Eramo, G., Gambacorta, L. and Salleo, C., “Asymmetric information in securitization: An empirical assessment”, Journal of Monetary Economics, Vol. 71, 2015, pp. 33-49). An analysis of default frequencies of the loans considered in this study does not reveal substantial differences from historical default frequencies on a larger pool of mortgage loans.

- High LTVs expose banks to higher loss-given-default and entail a higher risk of negative equity which can incentivise strategic defaults by borrowers. A loan is in negative equity when the value of the outstanding amount of the loan is higher than the value of the purchased real estate asset. High LTI loans measure the size of the loan in relation to the income of the borrower and correlate with default risk.