Published as part of the ECB Economic Bulletin, Issue 8/2022.

The euro area bank lending survey (BLS) provides valuable information on bank lending standards and conditions as well as on loan demand in the euro area. By collecting this information, the survey sheds light on the transmission of monetary policy in the euro area via the bank lending channel. It relies on a representative sample of about 150 euro area banks. While the survey information is qualitative, the replies of the banks are closely related to actual loan growth and lending rate developments. The BLS is especially useful for monetary policy purposes as it provides early indications about changes in bank lending criteria, conditions and loan demand before such changes become evident in actual loan developments.[1] This box describes how the BLS can provide early indications on developments in loans to firms and loans to households for house purchase in the euro area.

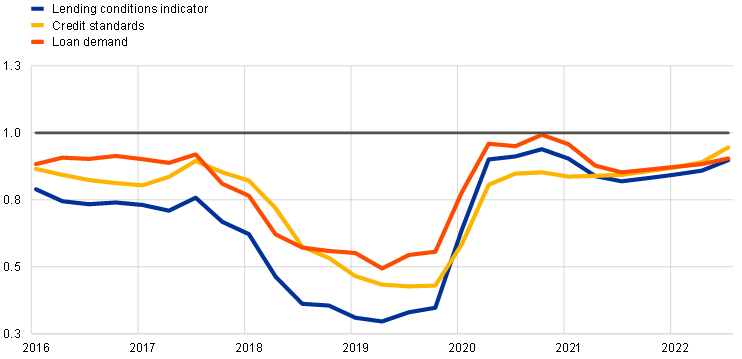

BLS data provide timely information on bank lending conditions and loan demand. Euro area banks reply to the BLS questionnaire around the end of each quarter. Aggregate BLS data are published by the ECB three weeks after receiving the replies from the reporting banks. The short reporting lag compared with other statistical data means that BLS data provide early information on key lending developments in the euro area, which has been especially valuable for identifying turning points in lending conditions and assessing lending developments during exceptional periods. For example, at the start of the coronavirus pandemic in 2020, the BLS signalled early on that there had been a sharp rise in the demand for loans on account of increased short-term financing needs of firms (Chart A), and a substantial fall in household loan demand for house purchase, owing mainly to a drop in consumer confidence.[2] The BLS also provided timely information on the impact of the Russian war in Ukraine and the surge in energy costs on bank lending conditions in 2022, revealing a net tightening of credit standards – driven mainly by an increase in banks’ risk perceptions in the context of high uncertainty about the economic outlook and concerns about borrowers’ creditworthiness. While most of the BLS questions are backward-looking, the survey also includes some forward-looking questions on the expectations of banks for credit standards and loan demand in the coming three months, allowing some assessment of future lending conditions based directly on the expectations of banks.

Chart A

Loan growth and BLS indicators for euro area firms

(left-hand scale: net percentages of banks over the past three months; right-hand scale: quarterly growth rate in percentages)

Source: ECB (BLS and Balance Sheet Items (BSI) statistics).

Notes: “Loans to firms” refers to the quarterly net loan growth to non-financial corporations. For credit standards, net percentages are defined as the difference between the percentage of banks reporting an easing and the percentage of banks reporting a tightening. For loan demand, net percentages are defined as the difference between the percentage of banks reporting an increase and the percentage of banks reporting a decrease.

The BLS also helps to disentangle credit supply from credit demand in lending developments. Analytical work on credit supply and demand and possible credit constraints has been especially important for understanding lending developments during the global financial crisis and the sovereign debt crisis.[3] The BLS has also played an important role in assessing the impact of the ECB’s monetary policy measures, such as its asset purchases and targeted longer-term refinancing operations (TLTROs), on bank loan supply and demand.[4] Overall, the BLS has proved to be a very useful tool for understanding and analysing bank lending conditions in the euro area. Within this broader range of topics, this box focuses on one specific characteristic of the BLS, namely its leading indicator properties for predicting loan growth.

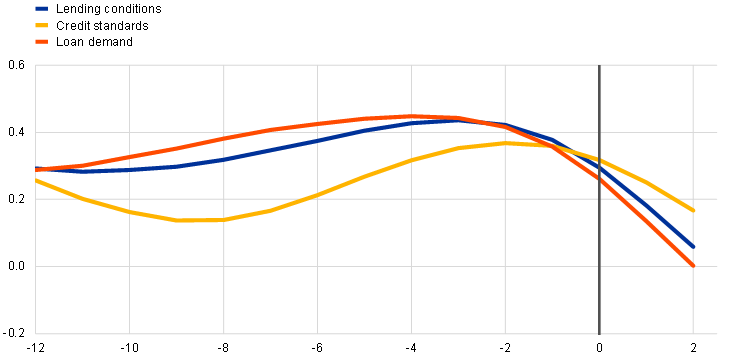

Changes in BLS credit standards and loan demand have leading indicator properties for future growth in loans to firms. A first indication of the information BLS indicators provide for future loan growth is to consider cross-correlations between BLS indicators at different leads relative to data on actual loan growth. For loans to firms, the cross-correlation between credit standards and annual loan growth is highest when the BLS leads actual loan growth by five to six quarters (Chart B, panel a). In other words, a tightening of credit standards tends to lead to weaker loan growth around five to six quarters later. For loan demand, the maximum correlation is higher and observed for a shorter lead of around three quarters. The longer lead between credit standards and actual loan developments is consistent with the fact that credit standards are set ahead of loan negotiations by the banks. By contrast, firms’ financing needs, as indicated by loan demand, are reflected faster in actual loan growth developments.

Chart B

Cross-correlations between loan growth and BLS indicators for euro area firms and households

a) Loans to firms

(y-axis: correlation coefficient; x-axis: lag of BLS indicators relative to loan growth in quarters)

b) Loans to households for house purchase

(y-axis: correlation coefficient; x-axis: lag of BLS indicators relative to loan growth in quarters)

Source: ECB (BLS and BSI statistics).

Notes: The chart shows the correlation between aggregate BLS indicators, based on the BLS sample of about 150 banks, and the annual growth rate of loans (net loan growth) to non-financial corporations (panel a) and to households for house purchase (panel b). BLS indicators either lead loan growth (negative value on the y-axis) or lag loan growth (positive value). “Lending conditions” refers to the net increase in loan demand minus the net tightening of credit standards. “Credit standards” are inverted, i.e. net percentages are defined as the share of banks reporting an easing minus the share of banks reporting a tightening. The annual growth rate of loans is computed as the sum of loan flows over the past 12 months divided by the outstanding amount of loans 12 months ago. BLS indicators are four-quarter moving averages. Loans to firms are adjusted for sales, securitisation and cash pooling.

Beyond the simple correlations mentioned above, the information that the BLS indicators provide on future loan growth can be assessed by analysing their value in forecasting actual loan growth. Compared with an autoregressive model where loan growth is predicted by its own lag, a model which includes BLS indicators improves the loan growth forecast for euro area firms (Chart C, panel a). While credit standards and loan demand each individually improve loan forecasts, combining both in a lending conditions indicator further improves the performance of forecasts over time, i.e. the forecast error is reduced more on average. Broadly corresponding evidence on the information that the BLS provides regarding future loan growth is also found for individual euro area countries.[5]

Chart C

BLS leading properties for future growth in loans to euro area firms

a) Performance of BLS indicators in forecasting aggregate loan growth

(ratio of root mean squared error of out-of-sample forecast of loan growth based on models with and without BLS indicators)

b) Impact of changes in credit standards and loan demand on loan growth at the level of individual banks

(impact on annual loan growth in percentage points)

Source: ECB (BLS and BSI statistics for panel a; individual BLS and individual BSI statistics for panel b) and ECB calculations.

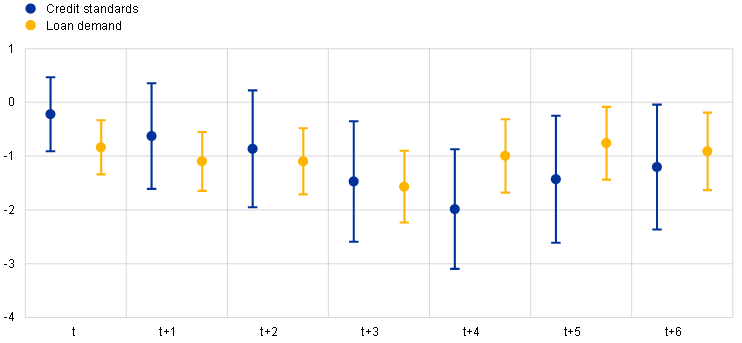

Notes: Panel a shows the performance of BLS indicators in forecasting annual loan growth at a horizon equal to two quarters. Values below 1 indicate that augmenting a pure autoregressive model with the BLS improves the forecast’s accuracy. Annual loan growth is defined as net loan flows over the past 12 months divided by the outstanding amount of loans 12 months ago, adjusted for sales, securitisation and cash pooling. Models are estimated over rolling ten-year windows. Root mean squared errors (RMSEs) are computed over rolling four-year windows. Panel b shows the impact on annual loan growth in periods t+i, with BLS indicators measured in period t. Effects are relative to banks which report eased or unchanged credit standards/increasing or unchanged loan demand. Coefficients result from a regression with the annual growth in net loans to firms as the dependent variable and the respective lags of banks’ reported credit standards and loan demand, three lags of the dependent variable and bank and country time-fixed effects as explanatory variables. The sample includes 149 banks and covers the period from the third quarter of 2009 to the second quarter of 2022.

The BLS contains information on future loan growth not only at the aggregate level, but also for individual banks. Bank-level estimations show that for banks reporting tighter credit standards, actual growth in loans to firms declines significantly three to six quarters after the tightening relative to banks reporting eased or unchanged credit standards (Chart C, panel b). At the same time, for banks which report a decrease in demand for loans in the BLS, actual growth in loans to firms is lower in the same quarter and the following quarters compared with banks reporting unchanged or increased loan demand.[6] This shows that the more contemporaneous relationship of loan demand with actual loan growth in the cross-correlations of the aggregate series is also valid at the level of individual banks.

For housing loans, BLS indicators also provide valuable information about future loan growth, albeit with a shorter lead time and a somewhat weaker correlation than in the case of loans to firms. In particular, the cross-correlation between credit standards and housing loan growth shows that the BLS indicator has only a slight lead over actual housing loan growth (peaking at around two quarters; Chart B, panel b). For housing loan demand, the cross-correlation with housing loan growth is generally higher than for credit standards, and peaks somewhat earlier, with a lead of three to four quarters. In addition, the co-movement of the BLS indicators with net loan growth is weaker overall for housing loans than for loans to firms. However, this difference is likely related to the fact that housing loan repayments were high as of around ten years after the housing market boom experienced before the global financial crisis, which was dragging down net housing loan growth.[7] In fact, the correlation is higher for both credit standards and housing loan demand when considering new business loans for house purchase (peaking at around 0.6 in both cases, with a lead of four quarters), which is also in line with banks being asked to report on gross loans in the BLS.

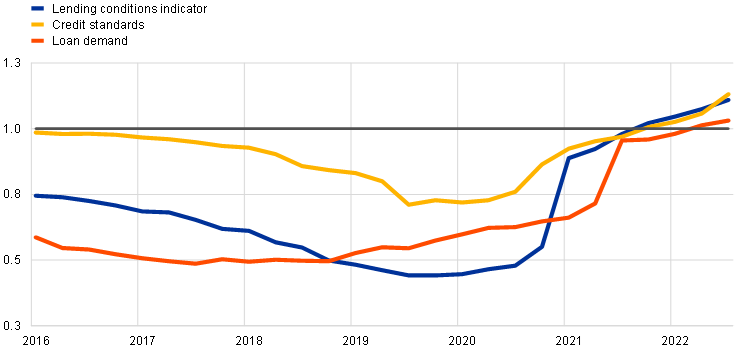

The information reported in the BLS also helps improve housing loan growth forecasts. In contrast with forecasts for loans to firms, housing loan growth forecasts are improved more by including loan demand than by including credit standards (Chart D, panel a). This is in line with the fact that the cross-correlation of net housing loan growth is lower with credit standards than with loan demand, as discussed above. Loan demand also helps predict future housing loan growth at the bank level – banks reporting a decrease in demand experience lower loan growth over the following quarters compared with banks reporting unchanged or increased loan demand (Chart D, panel b). By contrast, credit standards are less relevant for predicting housing loan growth, not only at the aggregate level but also at the level of individual banks.

Chart D

BLS leading properties for future growth in loans to euro area households for house purchase

a) Performance of BLS indicators in forecasting aggregate loan growth

(ratio of root mean squared error of out-of-sample forecast of loan growth based on models with and without BLS indicators)

b) Impact of changes in credit standards and loan demand on loan growth at the level of individual banks

(impact on annual loan growth in percentage points)

Sources: ECB (BLS and BSI statistics for panel a; individual BLS and individual BSI statistics for panel b) and ECB calculations.

Notes: Panel a shows the performance of BLS indicators in forecasting annual loan growth at the horizon yielding the lowest average RMSE (two quarters for credit standards, five quarters for loan demand and three quarters for lending conditions). Values below 1 indicate that augmenting a pure autoregressive model with the BLS improves the forecast’s accuracy. Annual loan growth is defined as net loan flows over the past 12 months divided by the outstanding amount of loans 12 months ago. Models are estimated over rolling ten-year windows. RMSEs are computed over rolling four-year windows. Panel b shows the impact on annual loan growth in periods t+i, with BLS indicators measured in period t. Effects are relative to banks which report eased or unchanged credit standards/increasing or unchanged loan demand. Coefficients result from a regression with the annual growth in net loans to households for house purchase as the dependent variable and the respective lags of banks’ reported credit standards and loan demand, three lags of the dependent variable and bank and country time-fixed effects as explanatory variables. The sample includes 140 banks and covers the period from the third quarter of 2009 to the second quarter of 2022.

In the light of these findings, the BLS currently points to a deceleration of loan growth to euro area firms and households for house purchase over the coming quarters. In the first three quarters of 2022 banks reported a net tightening of their credit standards for loans to firms.[8] In particular, the net tightening in the second and third quarters exceeded that observed during the coronavirus pandemic (which was dampened by public sector intervention in the form of loan guarantee schemes and other fiscal support measures as well as measures by monetary policy and supervisory authorities), while remaining below the net tightening seen during the global financial crisis and sovereign debt crisis.[9] The main drivers of this tightening were banks’ higher risk perceptions and lower risk tolerance owing to concerns regarding the general economic outlook and borrower creditworthiness. Banks’ cost of funds and balance sheet situations also had a tightening impact on credit standards for loans to euro area firms and households for house purchase. This impact became larger over the first three quarters of 2022 with the ongoing monetary policy normalisation. This reflects the survey’s usefulness for assessing the passthrough of the ECB’s monetary policy to euro area firms and households via the bank lending channel. At the same time, banks reported that, on balance, loan demand from firms continued to increase in the first three quarters of 2022, driven mainly by firms’ financing needs for working capital and inventories. In the October 2022 BLS, banks reported that they expect a further strong net tightening in credit standards but a net decline in loan demand from firms in the fourth quarter of 2022. Overall, these results point to slower growth in loans to firms during 2023.[10] For housing loans, banks reported a substantial net decrease in housing loan demand in the third quarter of 2022, following a more moderate decline in the second quarter of 2022. In conjunction with the strong net tightening of credit standards for housing loans in the second and third quarters of 2022, this points to a marked decline in actual housing loan growth in the coming quarters. In fact, signs of a turning point in actual housing loan growth are already visible.

See the article entitled “What does the bank lending survey tell us about credit conditions for euro area firms?”, Economic Bulletin, Issue 8, ECB, 2019. See also De Bondt, G., Maddaloni, A., Peydró, J.-L. and Scopel, S., “The euro area bank lending survey matters – empirical evidence for credit and output growth”, Working Paper Series, No 1160, ECB, February 2010.

See the box entitled “Drivers of firms’ loan demand in the euro area – what has changed during the COVID-19 pandemic?”, Economic Bulletin, Issue 5, ECB, 2020.

See, for instance, Altavilla, C., Darracq Pariès, M. and Nicoletti, G., “Loan supply, credit markets and the euro area financial crisis”, Journal of Banking and Finance, Vol. 109, 2019, in which the authors construct a loan supply indicator based on the BLS and use it to identify the impact of loan supply shocks on euro area real economic activity. Other examples of analytical work on loan supply based on the BLS are, for instance, Hempell, H. and Kok Sorensen, C., “The impact of supply constraints on bank lending in the euro area – crisis induced crunching?”, Working Paper Series, No 1262, ECB, November 2010, and Maddaloni, A., and Peydró, J.-L., “Bank Risk-taking, Securitization, Supervision and Low Interest Rates: Evidence from the Euro-area and the U.S. lending standards”, The Review of Financial Studies, Vol. 24, No 6, 2011, pp. 2121-2165.

See, for instance, Altavilla, C., Boucinha, M., Holton, S. and Ongena, S., “Credit Supply and Demand in Unconventional Times”, Journal of Money, Credit and Banking, Vol. 53, No 8, 2021, and Andreeva, D.C. and García-Posada, M., “The impact of the ECB’s targeted long-term refinancing operations on banks’ lending policies: The role of competition”, Journal of Banking and Finance, Vol. 122, 2021.

See “Negative interest rate policy period and pandemic as reflected in the Bank Lending Survey”, Monthly Report, Deutsche Bundesbank, September 2022, and Levieuge, G., “On the coherence and the predictive content of the French Bank Lending Survey’s indicators”, Working Paper Series, Banque de France, No 567, August 2015.

These results show that banks’ responses on credit standards and loan demand for firms not only help improve loan growth forecasts on aggregate, but also contain valuable information on changes in loan volumes for individual banks. Importantly, this is the case even after accounting for past developments, bank-specific factors and national macroeconomic developments that may influence the lending markets in which banks operate.

See the box entitled “Developments in mortgage loan origination in the euro area”, Economic Bulletin, ECB, Issue 5, 2018.

The BLS evidence provided by banks is consistent with the latest evidence from firms in the Survey on the Access to Finance of Enterprises (SAFE), in which firms reported a widening of their financing gaps for the period from April to September 2022 and expect a reduced availability of bank loans for the period from October 2022 to March 2023. See the box entitled “Firms’ access to finance and the business cycle – evidence from the SAFE” in this issue of the Economic Bulletin.

See the BLS reports on these quarters on the ECB’s website.

Notwithstanding the information provided by BLS indicators on actual growth in loans to firms and to households for house purchase, it needs to be kept in mind that these developments are unconditional forecasts based solely on the BLS and that further changes to the economic environment and outlook may alter these trajectories.