- THE ECB BLOG

Repo markets: Understanding the effects of a declining Eurosystem market footprint

23 July 2024

Repo markets are vital for banks to source liquidity and securities. They also represent an essential link in the monetary policy transmission chain. While the Eurosystem is in the process of reducing its market footprint, repo markets are going through a phase of change. The ECB Blog looks at dynamics in this market.

Monetary policy and repo markets are closely connected. The removal of monetary policy accommodation and the ongoing reduction of the Eurosystem’s footprint in financial markets set in motion some forces with countervailing effects on euro area repo markets. In this blog post, we identify these opposite forces and how they have influenced the dynamics in this market segment. In doing so, we take stock of the recent past to reflect on the growing importance of repo markets as a channel for liquidity redistribution, and outline the challenges for repo markets that lie ahead in this respect.

But first, what is a repo? “Repo” is short for “repurchase agreement”, which is a transaction where one market participant sells a security to another one, with an agreement to repurchase it later. Therefore, repos can offer a secured way to borrow and deposit cash for banks and other financial intermediaries, or a means to obtain a specific security. Moreover, repo markets are of critical importance for the smooth functioning of the government bond market, as they provide the financing for bond investments and help market participants source specific securities. Disruptions in repo markets can propagate to secondary government bond markets, affecting market liquidity and banks’ funding conditions. Thus, dysfunction in repo markets can have an adverse effect on the broader financial system and impede the smooth transmission of monetary policy.

How has the reduction of the Eurosystem’s footprint in government bond markets supported repo market functioning?

As repo markets play such a crucial role, it is worth checking how they have coped with the reduction of the Eurosystem’s footprint in euro area government bond markets.

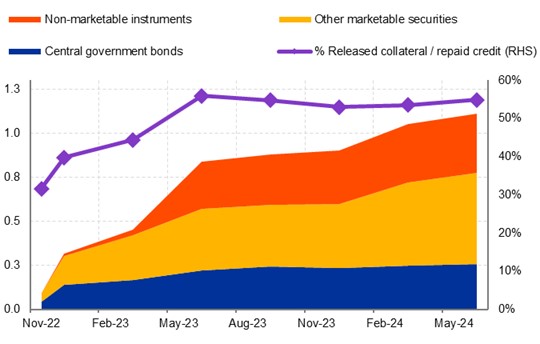

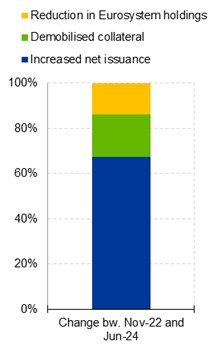

Since 2022, the Eurosystem has made significant headway towards reducing its presence in government bond markets. The early repayments of the Targeted Longer-Term Refinancing Operations (TLTROs) in Q4 2022, after the decision to change their pricing, set this process in motion. With the repayments of more than EUR 2 trillion of outstanding TLTROs, almost 60% of the collateral previously mobilised with the Eurosystem in exchange for these funds has returned to the market. Especially in Q4 2022, significant volumes of government bonds that were previously tied up as collateral have made their way back into repo markets (collateral worth almost EUR 300 bn by now). After this initial phase, the amount of government bonds released has, however, remained stable, and other marketable but also non-marketable securities were demobilised instead (Chart 1, LHS).

This initial step of TLTRO repayments was followed by the decision to start a gradual run-off of the asset purchase portfolio (APP) in March 2023 and to reduce the holdings of the pandemic emergency purchase portfolio (PEPP) as of July 2024. These decisions made a significant contribution to shrinking the Eurosystem’s footprint in euro area government bond markets, which was further supported by an increase in net issuance (Chart 1, RHS).

Chart 1

LHS: Eurosystem collateral released since the TLTRO III repayments in November 2022 (LHS axis: EUR trillion; RHS axis: %) RHS: Contributors to the reduction in Eurosystem footprint in euro area government bond markets, November 2022 – June 2024 (%)

Sources: Eurosystem, CSDB, ECB calculations.

Notes: The purple line in the LHS chart reports the ratio of released collateral to total credit repaid. The RHS chart displays the share of factors contributing to the reduction of the Eurosystem’s footprint in euro area government bond markets. It considers the change of total nominal amount of euro area government bonds outstanding, Eurosystem’s outright holdings and mobilised collateral since November 2022. Outright holdings are euro area government bonds held by the Eurosystem via purchase programmes, adjusted with euro area government bonds lent back via the Securities Lending against cash programme. Mobilised collateral includes euro area government bonds mobilised as collateral for open market operations.

Latest observation: 30 June 2024.

Before the extensive scaling back of the Eurosystem’s market presence, repo markets experienced some difficulties. In 2022, the proper functioning of repo markets was hindered by the scarcity of high-quality assets like highly-rated government bonds.[2] This threatened to delay the transmission of monetary policy in the early stages of the tightening cycle. The improved availability of collateral since then has helped to significantly alleviate such shortages of assets and played a positive role in ensuring a much quicker alignment of repo rates to changes in policy rates.

Dynamics in government deposits and link to repo markets

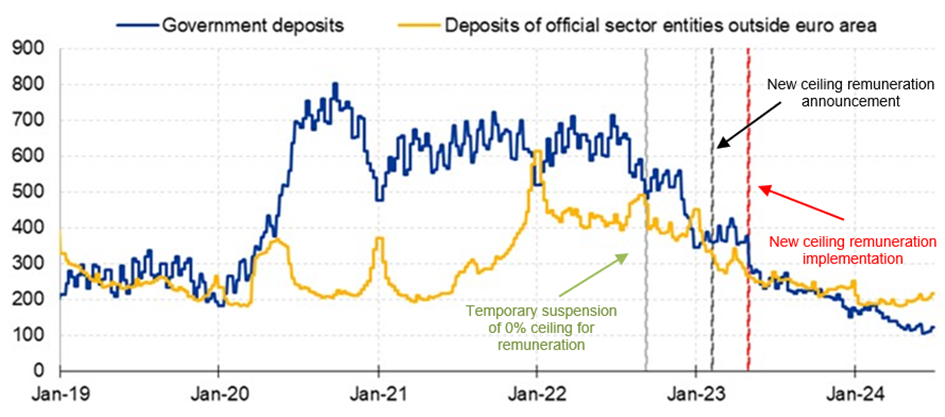

In addition to the reduction of the Eurosystem’s presence in euro area government bond markets, some other balance sheet dynamics have also had a bearing on repo markets. A case in point was non-monetary policy deposits – i.e., deposits placed with the Eurosystem by euro area governments and official-sector entities outside the euro area. The negative interest rate environment had prompted an increase in such deposits since 2014.[3] During the COVID-19 pandemic, many euro area debt management offices also built large cash buffers to mitigate cash flow volatility and funding risk in view of the heightened macroeconomic uncertainty and the large fiscal commitments made. Non-monetary policy deposits reached more than €1,000 billion during the pandemic (Chart 2).

As long as the movements in and out of these deposits were gradual and smooth, their size was less of a concern. However, at the beginning of the Eurosystem’s path to monetary policy normalisation, when the policy rate moved back into positive territory, the zero-percent ceiling on non-monetary policy deposits risked catalysing abrupt and sizeable outflows from the Eurosystem’s accounts into euro area repo markets. Such concerns affected the pass-through of the ECB’s policy rate hikes to repo markets in September 2022.

Chart 2

Non-monetary policy deposits: government deposits and deposits of official-sector entities outside the euro area (EUR billion)

Source: Eurosystem.

Notes: Temporary suspension of 0% ceiling for remuneration was announced on 8 September 2022 (green vertical line). New ceiling remuneration was announced on 7 Feb 2023 (black vertical line). New ceiling remuneration was implemented on 1 May 2023 (red vertical line).

Latest observation: 30 June 2024.

In the face of potential adverse effects on market functioning, the Eurosystem took action to ensure the smooth transmission of monetary policy. First, in September 2022, the Governing Council decided to temporarily remove the interest rate ceiling of zero percent for the remuneration of government deposits held with the Eurosystem, which incentivised governments to keep liquidity on the Eurosystem’s accounts for longer. Later, in February 2023, the Governing Council announced a new ceiling for the remuneration of euro area government deposits, set at the €STR minus 20 basis points. The remuneration of deposits held by foreign central banks was also adjusted accordingly. These changes came into effect on 1 May 2023.[4]

The aim of these adjustments was to encourage a gradual and orderly reduction of non-monetary policy deposits, thus minimising the risk of potential adverse effects on market functioning. As a result, non-monetary policy deposits have been on a declining trend since the end of summer 2022, and there were no significant disruptions in repo markets triggered by these outflows (Chart 2).

Modest effects from changes in the remuneration of minimum reserves

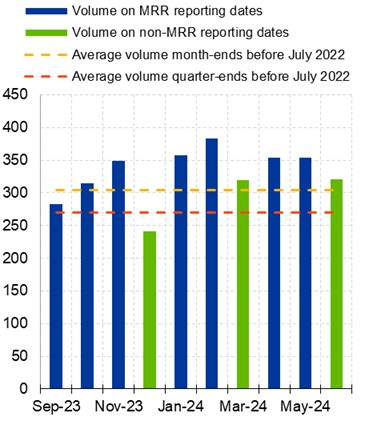

The speed and extent of the rise in policy rates has been the hallmark of the process of departing from the ECB’s previously very accommodative stance. However, this rate increase, coupled with an abundance of remunerated reserves, prompted the need for the Governing Council to assess whether it could achieve the same outcomes in terms of policy stance and transmission at a reduced cost for the Eurosystem. The outcome of this assessment was the decision announced in July 2023 to stop remunerating minimum reserves as of September 2023.[5]

When taking this decision, the Governing Council was cognisant that one of the possible reactions to the change could be that banks would reduce the reserve base for minimum reserve calculations through balance sheet optimisation strategies. Instead of accepting unsecured deposits, they could switch to secured deposits or FX swaps – instruments that are not included in the calculation of the reserve base. Such strategies could exert pressures on money markets including repo markets, especially on the days when minimum reserve requirements (MRR) are calculated.

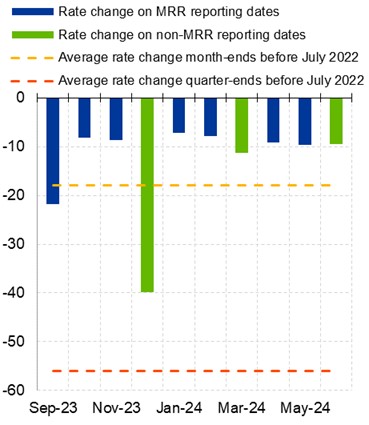

Chart 3

Month-end volumes of overnight transactions (LHS, EUR bn) and rate change (RHS, basis points) in secured money markets

Source: MMSR, ECB calculations.

Notes: Averages refer to month-ends (excluding quarter-ends) and quarter-ends (excluding year-ends) over the period January 2022 to June 2023, i.e., before the remuneration of minimum reserve requirements (MRR) was reduced from deposit facility rate (DFR) to 0%. Repo volumes and rates refer to 1-day transactions of MMSR reporting agents’ cash borrowing volumes against all euro area government bond collateral.

Latest observation: 30 June 2024.

So far, the minimum reserve reporting dates since July 2023 did see slightly higher volumes in repo markets compared to averages seen since 2022 (Chart 3, LHS). However, there was no noticeable price impact, in the context of the overall easing of collateral scarcity. Thus, any additional flows into the repo market were well absorbed (Chart 3, RHS) and the repo market impact of the change in minimum reserve remuneration has been modest.

Are repo markets at the cusp of a transformation?

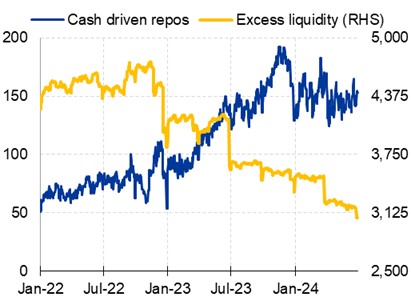

Overall, we have witnessed an easing of asset scarcity and improved repo market functioning in 2023 and 2024. Yet, given the still high excess liquidity in the euro area, the nature of the repo market remains fundamentally unchanged for the time being, as it continues to be dominated by the intention to source collateral. Looking ahead, the challenge will be whether repo markets can successfully transition to a new paradigm in which they are an efficient and effective vehicle for distributing liquidity in the euro area. This is particularly pertinent as the Eurosystem dials down its presence in funding markets and excess liquidity is being reabsorbed.

Chart 4

Outstanding volumes of liquidity-motivated repo transactions (EUR billion)

Sources: ECB, SFTD, BrokerTec, Eurex, MTS, ECB calculations.

Notes: Chart displays liquidity-motivated (general collateral, GC) repo volumes based on BrokerTec/MTS one-day repo transactions and on Eurex GC pooling trades as reported in Securities Financing Transactions Data (SFTD). Calculations are based on a single-counting approach.

Latest observation: 30 June 2024.

Although it is still early days, there are some tentative signs that such a transformation of repo markets may already be underway. This is shown, for instance, by the considerable rise in activity of liquidity-motivated transactions on major European trading platforms (Chart 4), which went hand-in-hand with the reduction of excess liquidity in the system.

Conclusion

As the Eurosystem dials down its footprint, markets need to rise up to the challenge of providing viable and effective alternatives. For banks, this means preparing to tap multiple and alternative sources of liquidity, including some that have not been used for a long time. As a result, going forward, repo markets will have to prove their ability to efficiently redistribute liquidity to all corners of the financial system.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

We are grateful to Benjamin Hartung, Katja Hettler, Annette Kamps, Benoit Nguyen, and Rita Fernandes Vitorino Besugo for their contribution to this blog post.

Several factors contributed to the scarcity of high-quality collateral in repo markets. First, the increase and volatility in yields of government bonds, amid the sharp repricing of interest rate expectations. This lowered government bonds’ value and simultaneously increased demand for these high-quality assets in repo markets. Second, the substantial holdings of government bonds of the Eurosystem reduced the amount of high-quality assets available to market participants.

Until September 2022 the relevant legal framework foresaw a remuneration ceiling for non-monetary policy deposits of zero percent if the deposit facility rate (DFR) was zero percent or higher. In the presence of a negative DFR, however, their remuneration was linked either to DFR or to €STR and, therefore, was more attractive compared to the situation under positive rates.

Following a comprehensive review of the remuneration of the different types of non-monetary policy deposits, the Eurosystem confirmed on 16 April 2024 the remuneration ceiling for euro area government deposits and most other non-monetary policy deposits.

In October 2022 the Governing Council decided to reduce the remuneration of minimum reserves from the rate on the Main Refinancing Operations (MRO) to the Deposit Facility Rate (DFR), while leaving the actual minimum reserves’ ratio unchanged at 1%.