Financial market infrastructures (FMIs) are the backbone of the financial system. They provide the networks through which financial institutions and financial markets connect with each other and through which financial transactions are cleared and settled. Therefore, it is essential to ensure that market infrastructures are safe and efficient, and that they provide for a stable and well-functioning economy. The Eurosystem is closely involved in this work as the conduct of monetary policy depends on the availability of reliable and effective FMIs, such as TARGET2 (the real-time gross settlement system), TARGET2-Securities (the securities settlement platform) and TIPS (the instant payment settlement service).

TARGET2-Securities (T2S), in particular, was conceived as an initiative to address the highly fragmented securities settlement landscape in Europe. It was launched in June 2015 as an integrated platform for processing securities transactions against central bank money. T2S revolutionised securities settlement in Europe by offering a solution to simplify cross-border settlement procedures and to the difficulties caused by different settlement practices among countries.

T2S provides harmonised and commoditised securities settlement to central securities depositories (CSDs), and applies a single set of rules, standards and tariffs to all participant CSDs. This allows the securities settlement platform to lay the foundations for a single market for securities settlement and, as a result, contributes to achieving greater integration of Europe’s financial market. Today, the T2S platform connects 20 CSDs and processes on average over 700,000 securities transactions per day against both euro and Danish kroner.

The report and its structure

This is the 11th edition of the TARGET2-Securities Annual Report, which now covers the fourth full year after the end of the T2S migration period. The first edition was published in 2011, a pivotal year for the finalisation of the legal and technical documentation of T2S and for the CSDs to prepare their T2S adaptation plans.

This year the report presents the evolution of T2S settlement data, while confirming the continuity of operational stability and efficiency. It describes the developments which took place in T2S in 2021 as well as some of the main incidents that had an impact on the platform throughout the previous year. The report is mainly addressed to decision-makers, practitioners, lawyers, and academics wishing to acquire an in-depth understanding of T2S and how it works. In addition, it will serve the public with an interest in market infrastructure matters and T2S in particular.

In addition to the core content, three boxes are included in this year’s publication. They provide in-depth information on the Market Settlement Efficiency Workshop V, the survey on on-hold functionality and late matching transactions, and the CSD Regulation (CSDR) and the settlement discipline regime that entered into force on 1 February 2022.

1 Evolution of T2S traffic in 2021

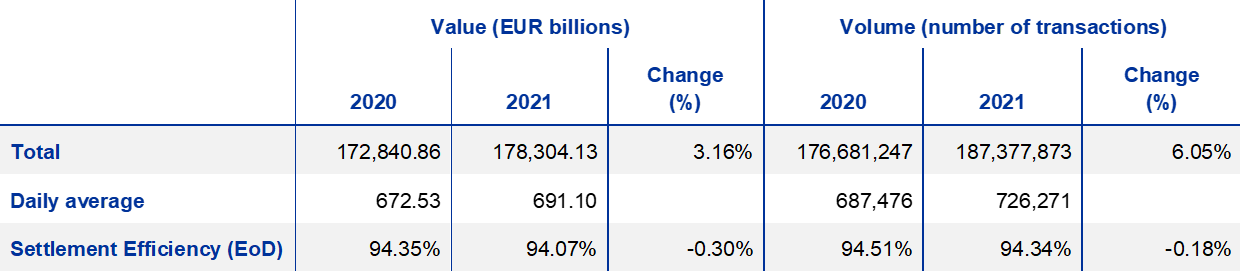

Table 1 provides an overview of traffic developments in T2S in 2021 compared with 2020. In 2021 T2S settled 187,377,873 transactions, with a total value of €178.30 trillion. This corresponded to a daily average volume of 726,271 transactions, with a daily average value of €691.10 billion. Compared with the previous year, there was an increase of 3.16% in the value settled, and of 6.05% in the volume settled. Settlement efficiency in 2021 was 94.07% in terms of value and 94.34% in terms of volume. This represented a minor decrease of 0.30% in terms of value and 0.18% in terms of volume compared with 2020.

Table 1

Evolution of T2S settlement data and settlement efficiency

Source: T2S.

Notes: There were 257 operating days in 2020 and 258 operating days in 2021. EoD: end of day.

1.1 Volume of settlements in T2S

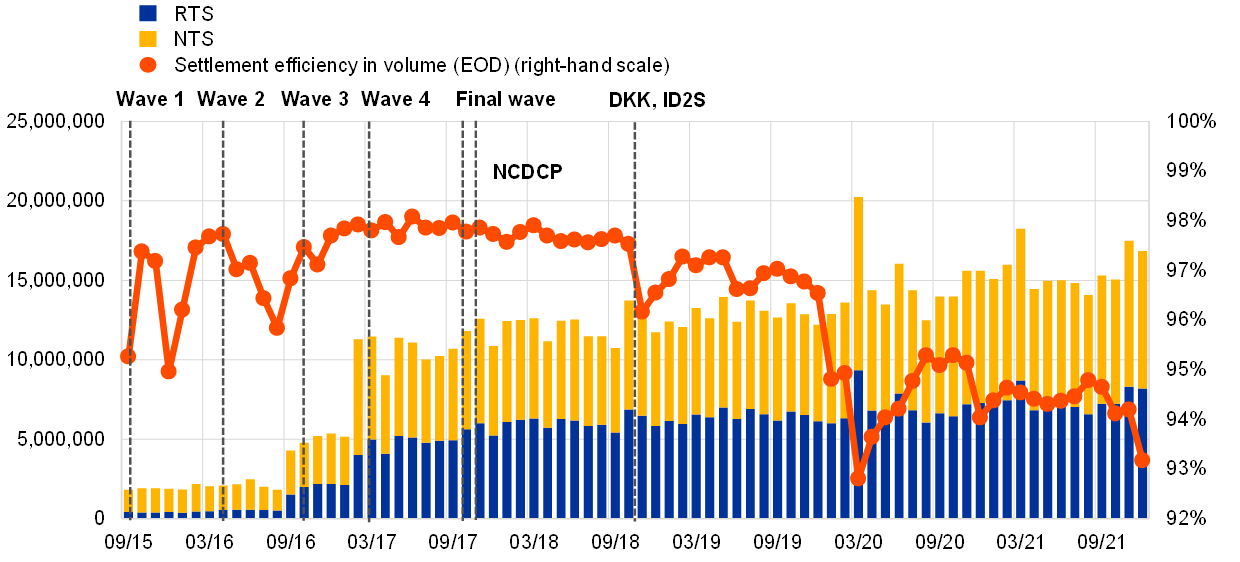

Chart 1 shows the evolution of the volumes settled in T2S and settlement efficiency at the end of the day since the first migration wave was completed in 2015. As a result of the migration waves, the monthly total T2S settlement volumes increased from 1,815,790 transactions in September 2015 to 11,804,649 transactions in October 2017. Between November 2018 and December 2019, total T2S settlement volumes averaged 12,819,952 transactions per month. In March 2020, following the outbreak of the coronavirus (COVID-19) pandemic, total monthly traffic peaked at 20,232,528 transactions. In 2021 T2S settled on average 15,614,823 transactions per month. Compared with 2020, the average monthly volumes were 6.05% higher in 2021. Monthly volumes peaked at over 18 million transactions in March 2021, although this was lower than the peak in March 2020. As traffic in T2S stabilised in its first few years of operation, settlement efficiency in volume terms became less volatile and averaged 96.85% between November 2018 and December 2019. Following the introduction of the new T2S statistical framework,[1] settlement efficiency in volume terms decreased to 94.81% in January 2020. The particularly high volumes settled in T2S in March 2020 affected settlement efficiency, which declined to 92.81%. Between that date and the end of 2021, settlement efficiency in volume terms averaged 94.50%.

Chart 1

Evolution of volumes settled in T2S and settlement efficiency at end of day

(left-hand scale: number of transactions, monthly totals; right-hand scale: settlement efficiency, percentages)

Source: T2S.

Notes: Migration wave 1 refers to 22 June‑31 August 2015; wave 2 refers to 29 March 2016; wave 3 refers to 12 September 2016; wave 4 refers to 6 February 2017; and final wave refers to 18 September 2017. NCDCP (Slovakian CSD) joined on 27 October 2017; settlement in Danish kroner (DKK) available, and ID2S (French CSD) joined on 29 October 2018.

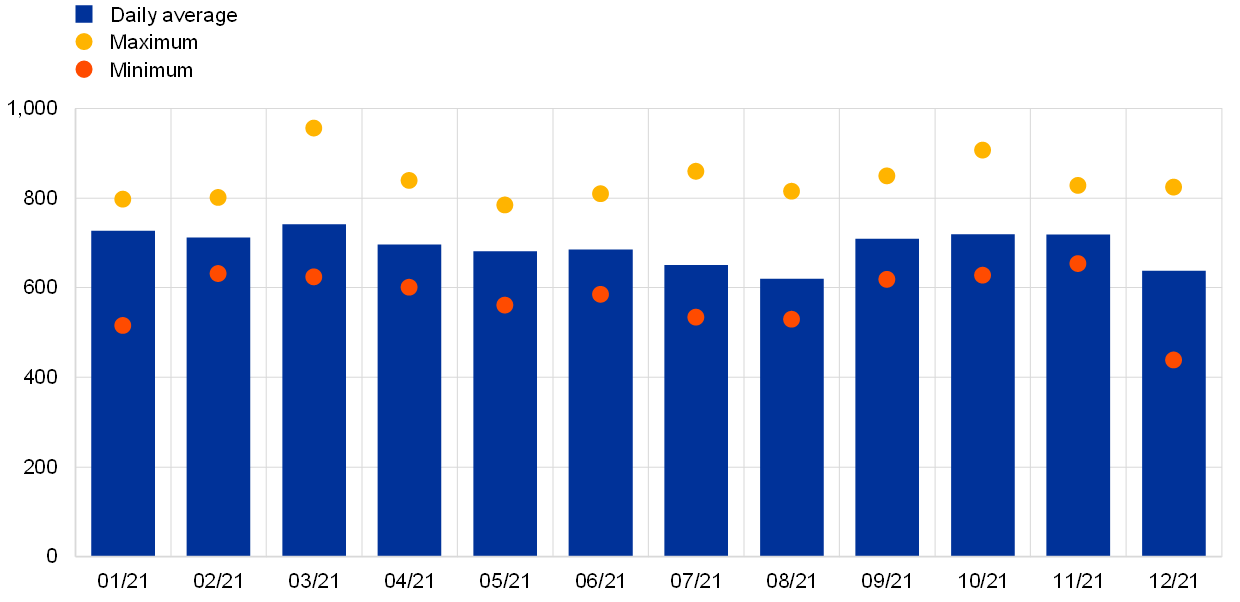

In 2021 T2S settled on average 726,271 transactions per day. Chart 2 shows the evolution of the daily average T2S traffic in volume terms. The daily average volume per month ranged from 639,876 (in August) to 798,571 (in February). The highest daily volume settled was on 30 November (1,061,928 transactions) and the lowest was on 28 December (245,181 transactions).The minimum occurred in a period of lower traffic owing to seasonality, with the closing of the German stock market on 24 December as a key driver for the volumes settled two business days later. The maximum was likely influenced by the market conditions at the time. Overall, the number of transactions settled in T2S on a daily average basis in 2021 was higher than in 2020 (687,476 transactions), despite the market volatility caused by the outbreak of the COVID-19 pandemic in March 2020.

Chart 2

Volumes of T2S transactions settled in 2021

(number of transactions (thousands), daily averages)

Source: T2S.

1.1.1 Real-time settlement and night-time settlement

In T2S, the new business day starts at 18:45 CET with the preparation for night-time settlement (NTS). NTS processing starts at 20:00 CET and is completed before 22:00 CET. It consists of two cycles. The first cycle is subdivided into five sequences and the second cycle into four sequences. Within the different sequences, a pre-defined set of transaction or instruction types is settled. At the end of the second cycle T2S submits, for partial settlement, all eligible transactions for which settlement failed in an earlier attempt in the same evening.

After the end of NTS there is a short preparation period for real-time settlement (RTS), followed by the RTS process. RTS is concluded by the end of the RTS process at 18:00 CET, but may be interrupted by the maintenance window. T2S Release 5.0 in June 2021 made the daily maintenance window optional. Additionally, the time of the weekly maintenance window has changed from Saturday at 03:00 CET to Monday at 05:00 CET. Since June the mandatory weekly maintenance window has been activated every weekend from Saturday 02:30 CET on Saturday to 02:30 CET on Monday. During the week the maintenance window is activated on an optional basis. When activated, it starts at 03:00 CET and ends at 05:00 CET. During the maintenance window T2S is closed for all settlement activities.

RTS includes five partial settlement windows, at 08:00 CET, 10:00 CET, 12:00 CET, 14:00 CET and 15:45 CET. In each partial settlement window, T2S partially settles new settlement instructions arriving in T2S that are eligible for partial settlement, as well as previously unprocessed or partially processed settlement instructions eligible for partial settlement. The first and the last partial settlement windows have a duration of 30 minutes each, while the others each have a duration of 15 minutes. The real-time settlement closure period starts with the DVP cut-off, which is harmonised at 16:00 CET for all currencies.

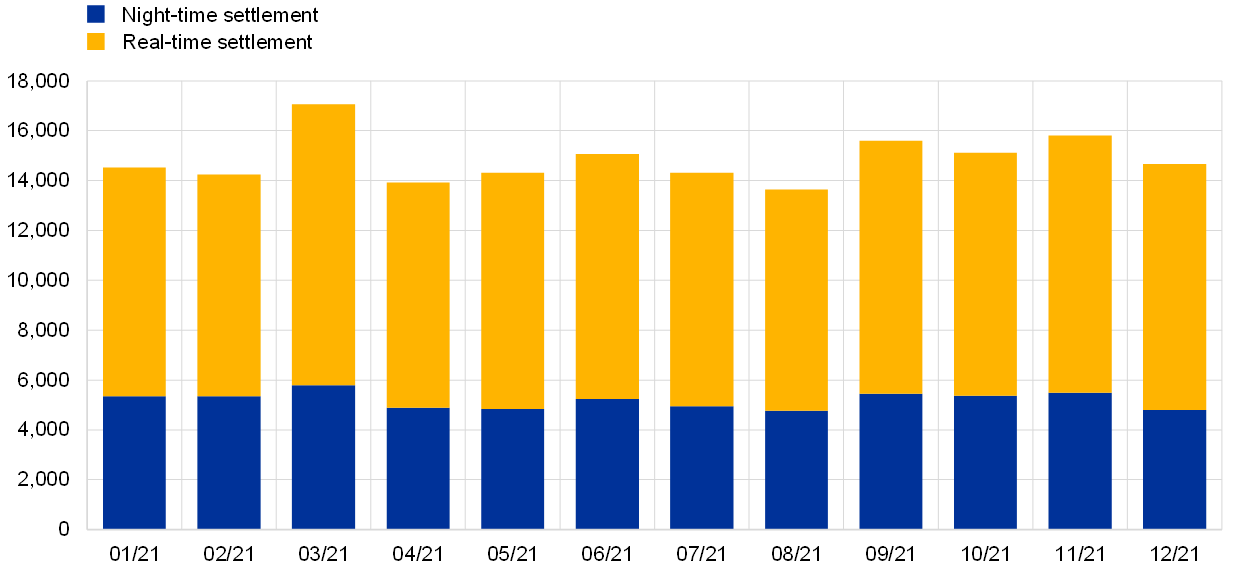

In 2021 15,614,823 transactions were settled on average each month, compared with 14,723,437 in 2020. Chart 3 shows the total monthly volumes of traffic, broken down by NTS and RTS. The total monthly traffic ranged between a low of 14,077,269 transactions in August and a high of 18,249,070 transactions in March. This is in line with 2020, as total monthly traffic reached its minimum (12,487,334 transactions) and maximum (20,232,528 transactions) levels in the same months.

Chart 3

NTS and RTS volumes in 2021

(number of transactions (millions), monthly totals)

Source: T2S.

As depicted in the chart, there is little variation in the share of the total volume settled in NTS and RTS each month in 2021. NTS accounted for 52.63% of the overall volume, while RTS accounted for 47.37%, which is in line with the 2020 statistics (52.98% and 47.02%, respectively). In absolute terms, the monthly volumes settled in NTS and RTS both peaked in March, at 9,543,443 and 8,705,627 transactions respectively. Conversely, in percentage terms, the peak volume settled in NTS was seen in February (53.32%), while the peak volume settled in RTS was seen in December (48.70%). In volume terms, delivery versus payment (DVP) transactions, which account for the majority of the T2S traffic, were largely settled during the NTS cycles (62.44%).

1.1.2 Settlement volume by transaction type

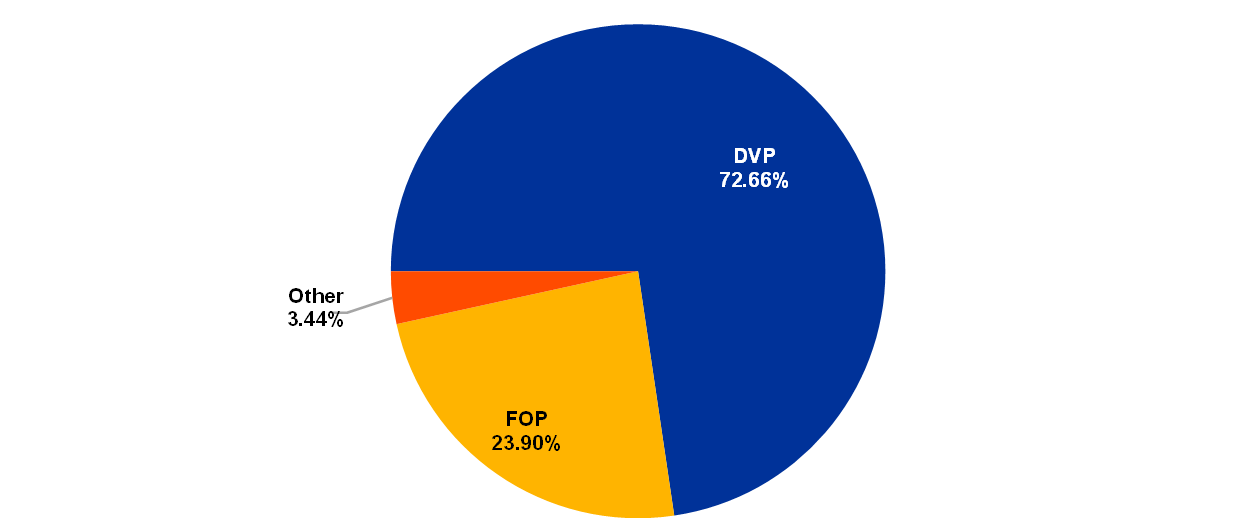

Five transaction categories make up T2S volumes: DVP, free-of-payment (FOP), payment-free-of-delivery (PFOD), settlement restrictions on securities (SRSE) and delivery-with-payment (DWP).[2] Chart 4 displays total T2S traffic broken down by transaction type.

Chart 4

Settlement volume by transaction type in 2021

(percentages, yearly totals)

Source: T2S.

Note: The category “Other” includes PFOD, SRSE and DWP.

In 2021 DVP and FOP transactions were the largest contributors to T2S traffic, together representing around 96.56% of the total settled volume, compared with 97.24% in 2020. DVP transactions accounted for most of the total T2S volumes, with 72.66% (corresponding to a daily average of 527,732 transactions). FOP transactions represented 23.90% of the total T2S volumes (corresponding to a daily average of 173,590 transactions). PFOD transactions, SRSE transactions and DWP transactions together accounted for 3.44% of the total volumes (corresponding to a daily average of 24,949 transactions). The percentage contribution of each transaction type relative to the overall volume is consistent with the pattern observed in previous years.

1.1.3 Settlement volume by transaction categories

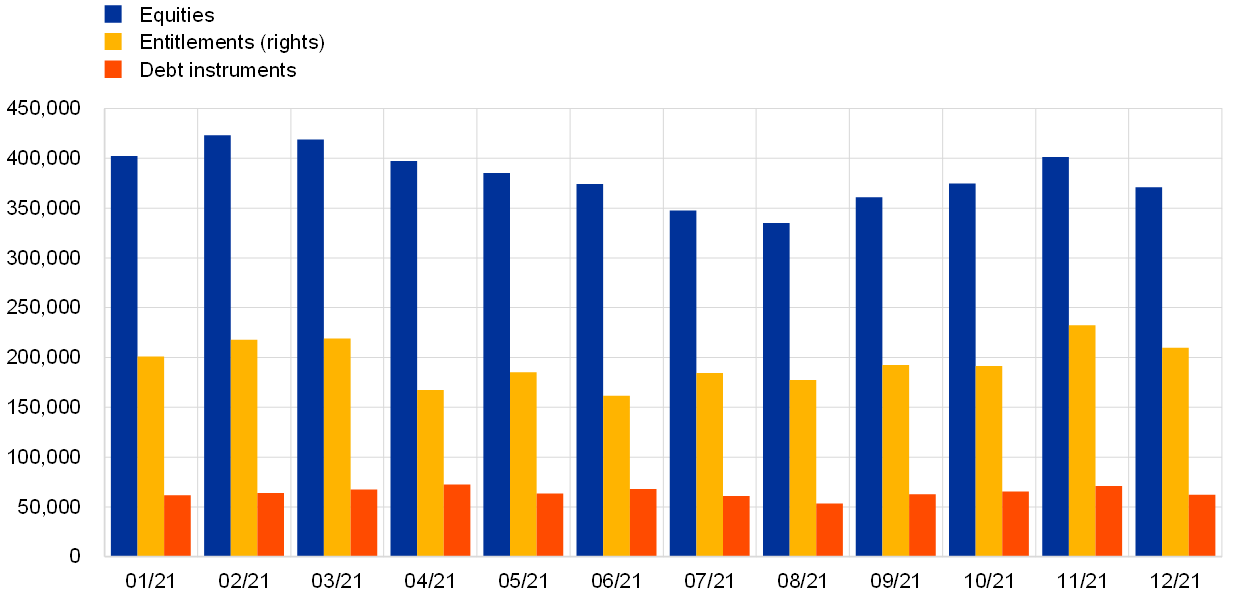

The three largest securities categories contributing to T2S traffic in terms of volume are equities, entitlements (rights) and debt instruments. Chart 5 shows the daily average volume settled for each of these three categories. In line with previous years, in 2021 equities represented the largest share of overall T2S traffic with a daily average volume of 382,204 transactions (52.63%), followed by entitlements (rights) with 195,235 transactions (26.88%) and debt instruments with 64,432 transactions (8.87%). The remaining share (11.62%) is attributable to other types of security. In 2020 the weight of equities and debt instruments was higher (58.52% and 9.57%, respectively), whereas the weight of entitlements (rights) was slightly lower (26.26%).

Chart 5

Volume by securities category in 2021

(number of transactions, daily averages)

Source: T2S.

The daily average volume of equity transactions in 2021 ranged between a low of 335,271 (in August) and a high of 423,261 transactions (in February). The daily average volume of entitlements (rights) ranged between 161,328 transactions (in June) and 232,520 (in November). The daily average volume of debt instruments ranged between 53,547 transactions (in August) and 72,778 (in April). Throughout the year equities consistently accounted for by far the largest volume, followed by entitlements and then debt instruments.

1.2 Value of settlements in T2S

Chart 6 shows the evolution of the value settled in T2S and of settlement efficiency at the end of the day since the first migration wave was completed in 2015. Following the migration waves, monthly total T2S settled values increased from €10.14 trillion in September 2015 to €19.14 trillion in October 2017. Between November 2018 and December 2019, total T2S settled values averaged €22.98 trillion per month. The introduction of the new T2S statistical framework considerably affected settled values, which dropped to €14.76 trillion in January 2020 (i.e. a decrease of 32.38% compared with December 2019). Similar to the trend in volumes, values also saw a notable increase in March 2020, reaching €16.74 trillion. Compared with 2020, average monthly volumes were 3.16% higher in 2021. Unlike volumes, in March 2021 values were higher than at the outbreak of the COVID-19 pandemic, standing at €17.06 trillion. Settlement efficiency in value terms averaged 97.52% between November 2018 and December 2019, largely in line with the average of 97.95% observed between September 2015 and October 2018. Following the methodological changes, the decrease in settlement efficiency between December 2019 and January 2020 was slightly larger in value terms than in volume terms (-2.33 percentage points compared with -1.73 percentage points). In line with volumes, settlement efficiency in value terms also dropped, falling to 88.95% in March 2020. From that date to the end of 2021, settlement efficiency in value terms averaged 94.40%.

Chart 6

Evolution of value settled in T2S and settlement efficiency at end of day

(left-hand scale: EUR billions, monthly totals; right-hand scale: settlement efficiency, percentages)

Source: T2S.

Notes: Migration wave 1: 22 June-31 August 2015; wave 2: 29 March 2016; wave 3: 12 September 2016; wave 4: 6 February 2017; final wave: 18 September 2017; NCDCP: 27 October 2017; DKK, ID2S: 29 October 2018.

In 2021 T2S settled an average of €691.10 billion per day. Chart 7 shows the evolution of daily average T2S traffic in value terms.[3] The daily average value ranged from €620.04 billion (in August) to €741.88 billion (in March). The highest daily value was recorded on 10 March (€955.75 billion) and the lowest on 29 December (€438.34 billion). In line with volumes, the minimum was reached in a period of lower traffic owing to seasonality. Overall, the daily average value settled in T2S in 2021 was higher than in 2020 (€672.53 billion). The range of the daily average volume per month was narrower than in 2020, when it fluctuated between €567.31 billion in August and €931.42 billion in March.

Chart 7

Values of settled T2S transactions in 2021

(EUR billions, daily averages)

Source: T2S.

Comparing Chart 7 with Chart 2, the highest daily traffic is seen in different months for volume (November) and value (March). This is not the case for the lowest daily traffic (which was recorded in December for both volume and value).

1.2.1 Real-time settlement and night-time settlement

In 2021 T2S settled transactions with an average monthly value of €14.86 trillion, compared with €14.40 trillion in 2020. Chart 8 depicts total monthly traffic in terms of value, broken down by NTS and RTS. Total monthly traffic ranged from a low of €13.64 trillion in August and a high of €17.06 trillion in March. This is in line with 2020, when minimum (€11.91 trillion) and maximum (€16.78 trillion) levels were reached in the same months.

Chart 8

NTS and RTS values in 2021

(EUR billions, monthly totals)

Source: T2S.

On average, RTS accounted for 65.09% of overall traffic in value terms in 2021 (61.67% in 2020), compared with 34.91% settled in NTS (38.33% in 2020). As shown in Chart 4, settlement was more evenly balanced between RTS and NTS in volume terms (47.37% and 52.63% respectively). This indicates that the RTS phases were more value-intensive than volume-intensive and featured transactions with a higher average value than in the NTS cycles. In contrast, the NTS cycles were more volume-intensive than value-intensive.

In absolute terms, the monthly values settled in both NTS and RTS in 2021 peaked in March, at €5,787.09 billion and €11,276.20 billion respectively. As a percentage of the total monthly value, the peak value settled in NTS was in February (37.52%), while the peak value settled in RTS was in December (67.31%). 65.20% of the total value of DVP transactions, which represented the majority of overall T2S traffic, was settled in RTS.

1.2.2 Settlement value by transaction type

Three transaction categories make up settlement values in T2S, namely DVP, DWP and PFOD, compared with five categories for volumes.[4] Chart 9 illustrates the total value settled in T2S by transaction type in 2021.

Chart 9

Settlement value by transaction type in 2021

(percentages, yearly totals)

Source: T2S.

Note: The category “Other” includes PFOD and DWP.

As for volumes (see Chart 5), DVP represented the largest transaction type in value terms in 2021. DVP transactions were on average the largest contributor to T2S traffic, accounting for 95.52% (corresponding to a daily average of €660.15 billion), compared with 96.38% in 2020. PFOD and DWP transactions together accounted for only 4.48% (corresponding to a daily average of €30.95 billion) of the total value settled, compared with 3.62% in 2020.

1.2.3 Settlement value by transaction categories

As in the case of volumes, the three largest securities categories contributing to T2S traffic in terms of value are equities, entitlements (rights) and debt instruments. Chart 10 shows the daily average value settled for these three types of security in 2021. Debt instruments were by far the largest securities category in overall T2S traffic in value terms, with a daily average of €587.28 billion (84.98%), followed by equities with €67.18 billion (9.72%) and entitlements (rights) with €1.14 billion (0.16%). The remaining share (5.14%) is attributable to other types of security. In 2020 the weight of debt instruments and equities was higher (85.55% and 10.02% respectively), whereas the weight of entitlements (rights) was largely unchanged (0.15%).

Chart 10

Value by securities category in 2021

(EUR billions, daily averages)

Source: T2S.

Note: Owing to the much lower values of entitlements (rights) settlements compared with the other two categories, the amounts are barely visible on the chart.

Unlike in Chart 6, where equities are the largest securities category in volume terms, they are the second largest in value terms, whereas debt instruments are by far the largest category in value terms but are the third largest in volume terms. This suggests that equity transactions have a much lower average value than debt instrument transactions. Like equities, entitlements (rights) contribute far more to settlement volumes than to values.

1.3 Settlement efficiency

Settlement efficiency measures the efficiency of the settlement engine of the T2S platform. It compares the volume (or value) of transactions that are settled on a given day with the total volume (or value) of transactions eligible for settlement on that day.[5]

Charts 11 and 12 show the evolution of settlement efficiency in T2S in 2021, at end of day (EOD) and after NTS respectively.

Chart 11

Settlement efficiency at end of day in 2021

(percentages, at end of day)

Source: T2S.

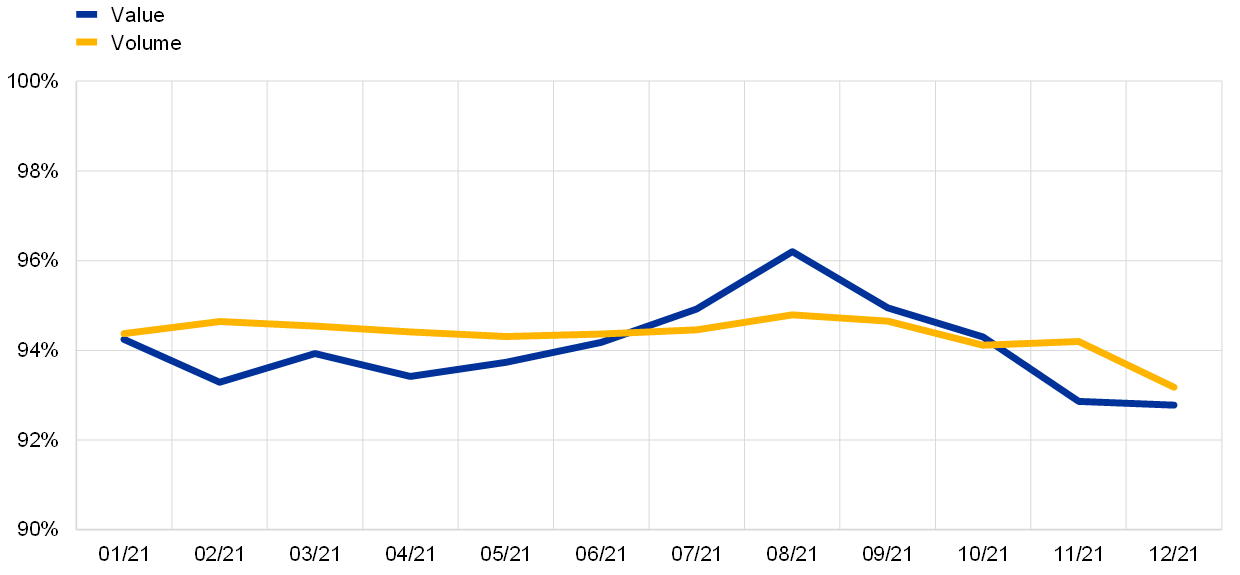

In 2021 settlement efficiency at end of day reached on average 94.34% in volume terms and 94.07% in value terms. This is in line with the 2020 calculations, when settlement efficiency at end of day averaged 94.51% in volume terms and 94.35% in value terms. In 2021 settlement efficiency in volume terms ranged between 93.18% and 94.79%, as illustrated in Chart 11. In value terms, it displayed more volatility, ranging between 92.78% and 96.20%. The minimum level was reached in December and the maximum level was reached in August, in both volume and value terms. During the fourth quarter of 2021 T2S recorded a significant increase in both the volume and the value of on-hold transactions, mainly owing to external reasons, such as volatility on financial markets. This, combined with the lower traffic typically seen in the month of December, negatively affected settlement efficiency. In this period the average settlement efficiency at end of day stood at 93.83% in volume terms and 93.31% in value terms.

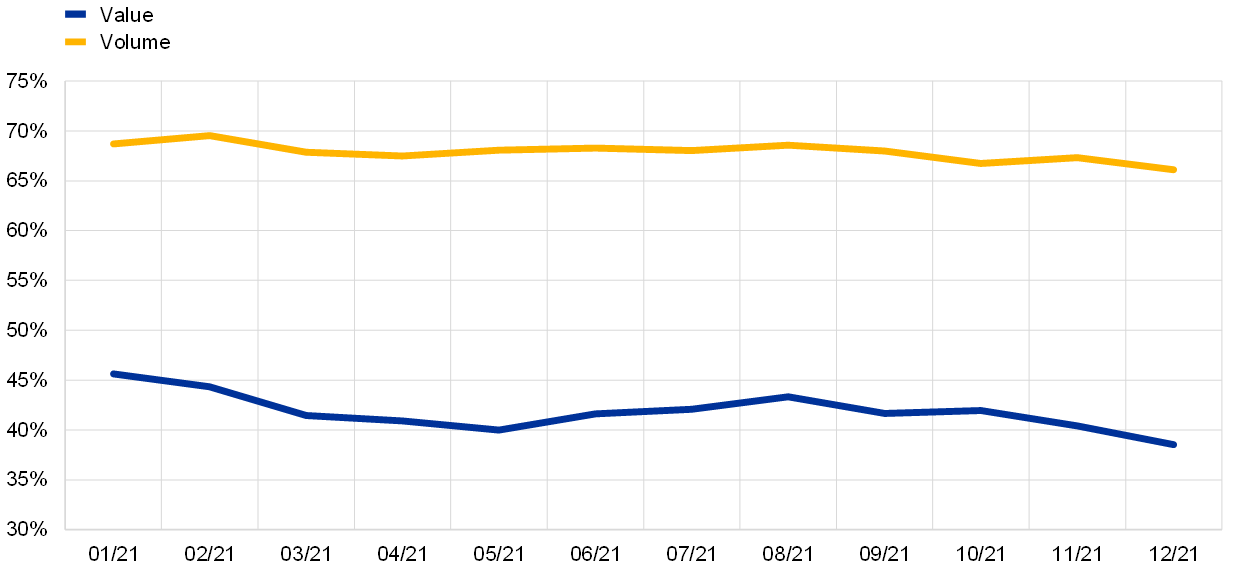

In 2021 average settlement efficiency after NTS reached 67.89% in volume terms and 41.82% in value terms (see Chart 12). This compares with a level of 67.85% in volume terms and 46.75% in value terms in 2020. In line with the end of day, settlement efficiency after NTS displayed more volatility in value than in volume terms. The minimum level was reached in December in both volume and value terms (66.09% and 38.53% respectively), whereas the maximum level was reached in February in volume terms (69.54%) and in January in value terms (46.51%).

Chart 12

Settlement efficiency after NTS in 2021

(percentages, after NTS)

Source: T2S.

It is important to emphasize that the settlement efficiency is in line with market expectations and its evolution is discussed with the key stakeholders via dedicated Market Settlement Efficiency (MSE) workshops. See also Box 1.

Box 1

Settlement efficiency according to CSDR guidelines

The analysis of settlement efficiency topics continued in 2021. A fifth dedicated Market Settlement Efficiency (MSE) workshop was organised in June. The main purpose was to improve on the calculation of the settlement efficiency indicator computed in accordance with the CSDR guidelines prepared for the fourth workshop, to support the CSDs in their preparation for the new regulatory framework. The enhancements encompassed aligning the treatment of partially settled transactions[6] with CSDR requirements and including late matching transactions (LMT)[7] in additional breakdowns compared with the fourth workshop. The indicators were provided at the global level, as well as by time of day, type of settlement instruction and type of asset. Moreover, a set of intraday settlement efficiency indicators was developed following contacts with the market.

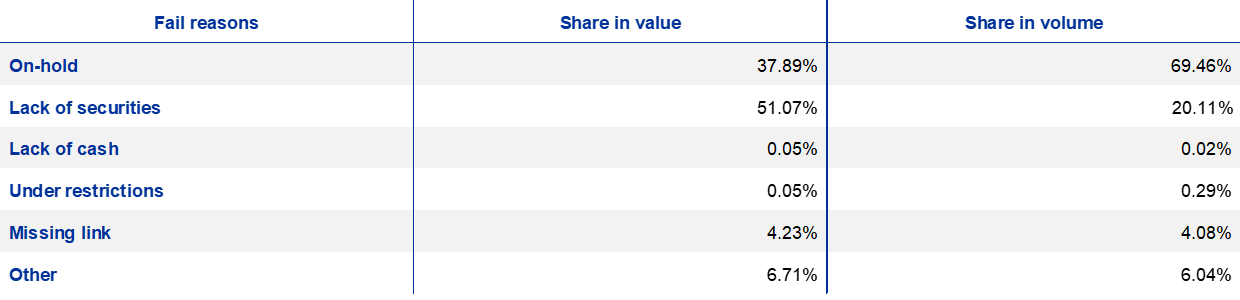

The CSRD settlement efficiency indicator (CSDR SEI) is based on the principle that transactions eligible for settlement that are not settled at end of day, irrespective of the reason, have to be considered as failures, thus having a negative impact on the settlement efficiency. In line with past results, the analysis showed that on-hold transactions were the main fail reason in volume terms in the reference month of February 2021, whereas in value terms lack of securities and on-hold transactions were the main fail reasons (see Table A). The asymmetric impact of the on-hold fail reason in the CSDR SEI for volume and value is mainly because the on-hold transactions are usually FOP transactions, which do not imply cash movements.

Table A

Main fail reasons in T2S

Source: T2S.

Notes: Calculations are for February 2021. Fail reasons are computed as a percentage of total failed transactions in value and volume terms.

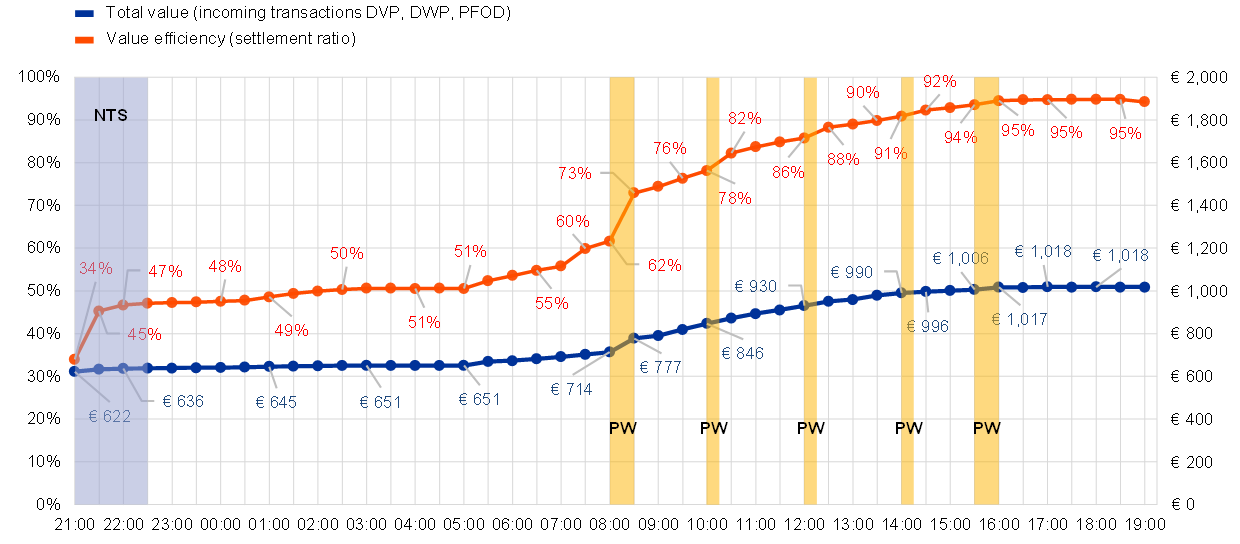

Particular attention has been paid to the intraday evolution of the CSDR settlement efficiency indicator, both in volume and value terms, with the aim of investigating liquidity usage and identifying settlement best practices to optimise settlement efficiency. The analysis looked at different points in time of the T2S business day, including the end of the two NTS cycles, the start of day-time at 07:00 CET, the end of all partial settlement windows (at 08:30 CET, 10:15 CET, 12:15 CET, 14:15 CET and 16:00 CET) and the end of RTS at 18:00 CET.

The intraday evolution of the CSDR settlement efficiency indicator in value terms showed two main increases throughout the business day: the first during the two cycles of the NTS phase and the second during the first partial settlement window scheduled for 08:00 CET. The CSDR SEI reached 33.97% in value terms at the end of NTS Cycle 1 and then jumped by 12.70 percentage points to 46.67% in a short time during NTS Cycle 2 (see Chart A). The increase was less pronounced afterwards (+3.90 percentage points to 50.57% in seven hours, from the end of NTS to 03:00 CET). The plateau observed between 03:00 CET and 05:00 CET was due to the maintenance window.[8] The CSDR SEI marked significant increases at each partial settlement window and reached 94.21% at the end of RTS, including the impact of LMTs. It is worth noting that the inclusion of LMTs has a negative effect on the CSDR SEI at the end of RTS, because it increases the number of transactions that are considered to be unsettled. Excluding the impact of LMTs, the CSDR SEI would increase to 94.78%.

Chart A

Evolution of the intraday settlement efficiency indicator in T2S in value terms

(left-hand scale: settlement efficiency in percentages; right-hand scale: total value in EUR billions)

Source: T2S.

Note: Calculations relative to February 2021. The blue shaded area represents the NTS phase and the yellow shaded areas represent the partial settlement windows throughout the T2S business day.

The intraday evolution of the CSDR settlement efficiency indicator in volume terms showed that the indicator reached 58.12% at the end of NTS Cycle 1 and grew by 3.04 percentage points to 61.16% during NTS Cycle 2 (see Chart B). The CSDR SEI showed a further slight increase of 6.72% in seven hours (to 67.88%) from the end of NTS to 03:00 CET. It then rose consistently throughout the day, mainly from 05:00 CET to 09:00 CET, when the settlement ratio increased by 14.03 percentage points, from 67.88% to 81.91%. The CSDR SEI reached 89.57% at end of RTS, including LMTs. Excluding the impact of LMTs, the CSDR SEI would increase to 91.25%.

Chart B

Evolution of the intraday settlement efficiency indicator in T2S in volume terms

(left-hand scale: settlement efficiency in percentages; right-hand scale: number of transactions in thousands)

Source: T2S.

Note: Calculations relative to February 2021. The blue shaded area represents the NTS phase and the yellow shaded areas represent the partial settlement windows throughout the T2S business day.

In conclusion, the analysis showed that the settlement efficiency indicator based on CSDR guidelines reached an average of 94.78% in value terms and 89.57% in volume terms, including the impact of LMT, at the end of the day, thus leaving room for further improvement. No critical points in time during the T2S operational day emerged, as the main causes of settlement fails are related to certain market-oriented practices, such as on-hold transactions,[9] and to a lack of securities. In addition, the analysis confirmed that the possibility of using multiple partial settlement windows during the day helps to increase settlement efficiency in T2S.

1.4 Unsettled transactions

Not all transactions submitted for processing in T2S are settled on the intended settlement day. This may be because the resources (cash and/or securities) needed for settlement are not available, one of the two instructions underlying the transaction is set to on-hold or the instruction is submitted late. Unsettled transactions negatively impact settlement efficiency (see Section 1.3).

Chart 13 illustrates the daily average volume of unsettled transactions in T2S at the end of the day in 2021. The calculations comprise of DVP, DWP, PFOD, FOP and SRSE transactions.

Chart 13

Volume of unsettled transactions in 2021

(number of transactions, daily averages)

Source: T2S.

In 2021 the daily average number of unsettled transactions was 14,170, which is slightly lower than the 14,418 transactions reported in 2020. This means that, on a daily average basis, of the total number of transactions processed by T2S, 5.66% were unsettled at the end of the day. Unsettled transactions reached a high of 16,449 in November and a low of 11,486 in August, thus mirroring the volume trends illustrated in Chart 3. In line with the results observed for settled transactions, DVP and FOP represented around 98.64% of all unsettled transactions in volume terms.

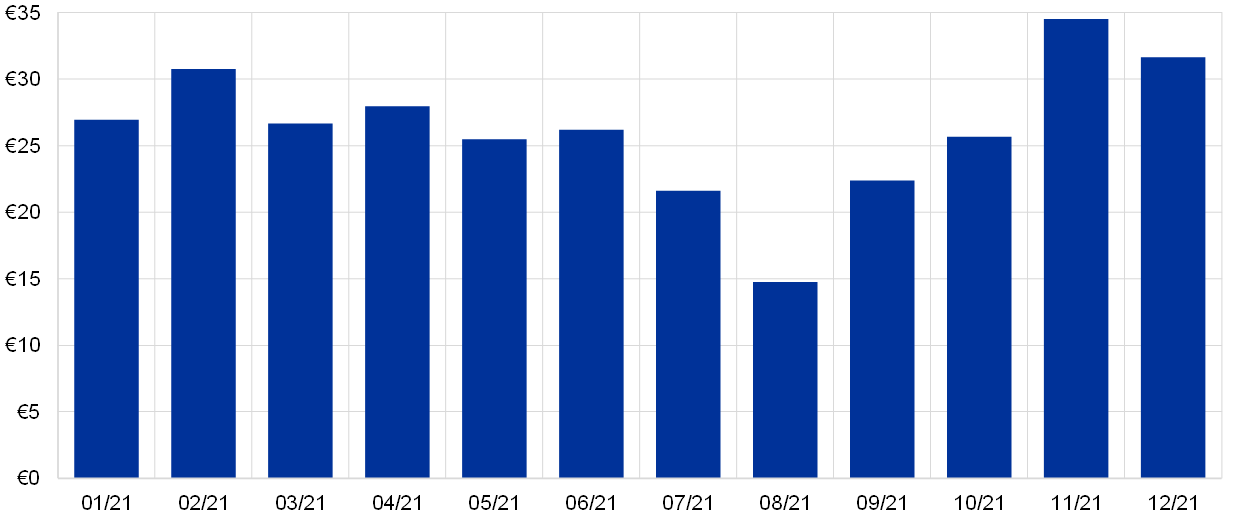

Chart 14 shows the daily average value of unsettled transactions in T2S in 2021. The transaction types contributing to the value are DVP, DWP and PFOD.

Chart 14

Value of unsettled transactions in 2021

(EUR billions, daily averages)

Source: T2S.

The daily average value of unsettled transactions in T2S in 2021 ranged between €14.75 billion in August and €34.52 billion in November. These figures are significantly lower than in 2020, when they ranged between €22.49 billion in October and €63.92 billion in March. In 2021 DVP represented 99.36% of all unsettled transactions in value terms, followed by PFOD with 0.64%. Once again, these results reflect the composition of settled traffic in value terms.

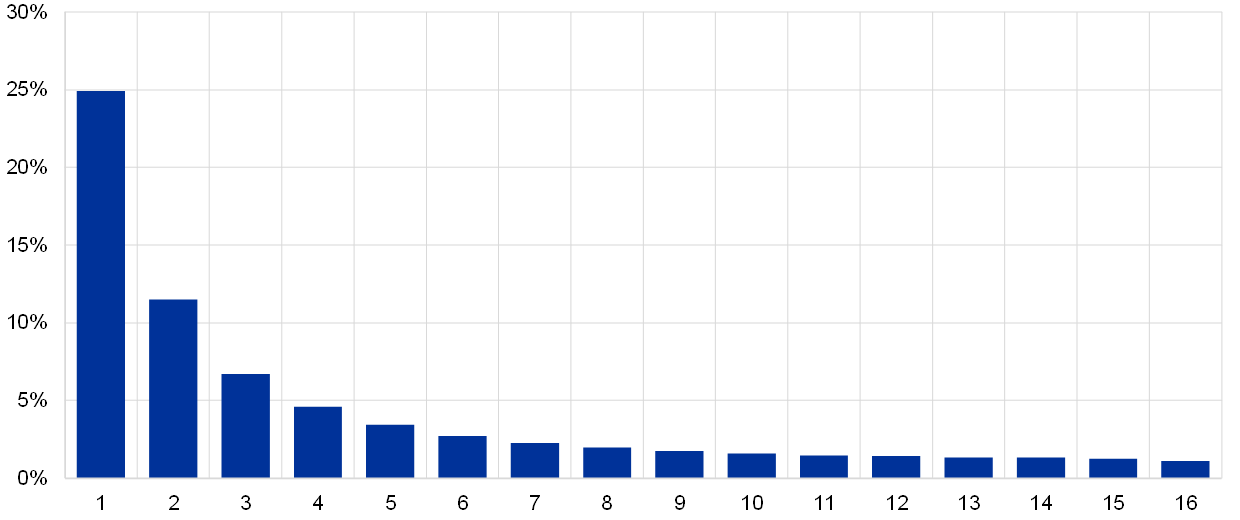

At the end of each day, the unsettled transactions are not deleted but automatically postponed by T2S (“recycled” in technical terms) to the following business day(s). T2S attempts to recycle them for a period of time referred to as the “recycling period” before they are automatically cancelled. In other words, the recycling period can be defined as the number of days during which a transaction remains unsettled. Chart 15 shows the share of unsettled transactions and the recycling days required before settling.

Chart 15

Average unsettled transactions per number of recycling days in 2021

(percentages, number of recycling days)

Source: T2S.

Chart 15 shows that on average 24.93% of unsettled transactions sent for recycling were settled on the following business day in 2021 (first column) and less than half of those (11.50% in total) were pending for two days before settlement. Only 1.11% were pending for 16 days (last bar). In 2020 these averages were slightly higher at 26.28%, 12.51% and 1.16%, respectively.

Box 2

Survey on on-hold and late matching transactions

Following the fourth workshop on settlement efficiency topics held in October 2020, a survey was carried out among the CSDs in T2S to investigate the reasons behind on-hold and late matching transactions in their markets. A total of 17 responses, covering 19 markets, were received. The results were grouped by the size of the reporting CSD and presented at the fifth workshop held in June 2021 (see Box 1). This box provides some key takeaways.

On-hold transactions

The on-hold functionality is a risk management tool aimed at ensuring the availability of the necessary resources before settlement is attempted in T2S. It comprises four types: party-on-hold, CSD-on-hold, CSD-validation-on-hold and CoSD (conditional securities delivery)-on-hold. Most CSDs, irrespective of their size, indicated that “party-on-hold” is the most widely used functionality, followed by 40% or more that use CSD-on-hold (see Chart A). Conversely, a minority of CSDs indicated that they use the CSD-validation-on-hold option, and only less than half of the medium and large CSDs reported usage of CoSD-on-hold. These results are in line with expectations, as T2S actors can set out the first two types of on-hold functionality, while the last two are automatically set by T2S in line with specific rules and conditions drawn up by the CSDs.

Chart A

Usage of the on-hold functionality in T2S by type

(percentages, share of respondents)

Source: ECB calculations.

Note: The size of the reporting CSD is determined by its volumes in T2S.

The results showed that the on-hold functionality is used for several reasons. First, it provides support for managing and optimising the settlement of specific instruction types and client resources. For instance, it can help prevent settlement fails that are due to a lack of securities when segregated accounts are involved and it supports ownership and position checks in the case of omnibus accounts. Second, the functionality supports the timely matching of transactions and helps prevent the settlement of cancelled transactions that are still awaiting the counterparty’s cancellation. Third, it helps manage settlement involving communities or markets outside T2S, where the partial release implementation may not be completed.

At the same time, the survey highlighted that inefficiencies in the usage of the on-hold functionality can arise owing to the lack of straight-through processing (STP) and the presence of interdependencies, also with markets outside T2S. These may cause the unavailability of resources by actors along the settlement chain. Moreover, it was noted that the system design means that transactions are not prioritised by their recycling period in T2S. Owing to regulatory requirements, T2S actors may thus set transactions with an intended settlement date (ISD) less than 4 days on-hold.

Late matching transactions

As discussed in Box 1, LMTs are matched either after their cut-off on the ISD has been reached or after their ISD, and thus count as unsettled at the end of the day.

The survey results indicated different potential reasons for LMTs in T2S. First, the need for information from own clients or counterparties and the submission of incomplete, invalid or incorrect instructions on either side can cause the late submission of instructions to T2S. Second, transactions in T2S can be matched late because the client submits the instruction to the CSD late. Third, business process dependencies, such as internal dependencies before submission to T2S, linkages between transaction flows or long intermediary chains also play a role.

Overall, the survey offered interesting insights into on-hold and LMTs from a market perspective. This can help the T2S operator better understand the way T2S actors make use of the available functionalities and consider implementing changes to address potential issues. It can also be considered a stock-taking exercise for the market, which may result in guiding and encouraging clients in the use of specific functionalities, promoting information sharing between counterparties or developing market practices.

1.5 Use of auto-collateralisation

Auto-collateralisation in T2S is an intraday credit operation granted by a central bank which is triggered when a T2S dedicated cash account (DCA) holder does not have enough funds to settle securities transactions. Its ultimate purpose is to improve the buyer’s cash position and secure the funds necessary to settle the transaction. Auto-collateralisation is an automatic process which is aimed at facilitating smooth real-time DVP settlement in central bank money.

Two types of auto-collateralisation are available in T2S:

- auto-collateralisation on-flow refers to the use of the securities which are about to be purchased as collateral to secure the necessary credit to complete the transaction;

- auto-collateralisation on-stock is the use of other securities already held by the buyer as collateral to complete the transaction.

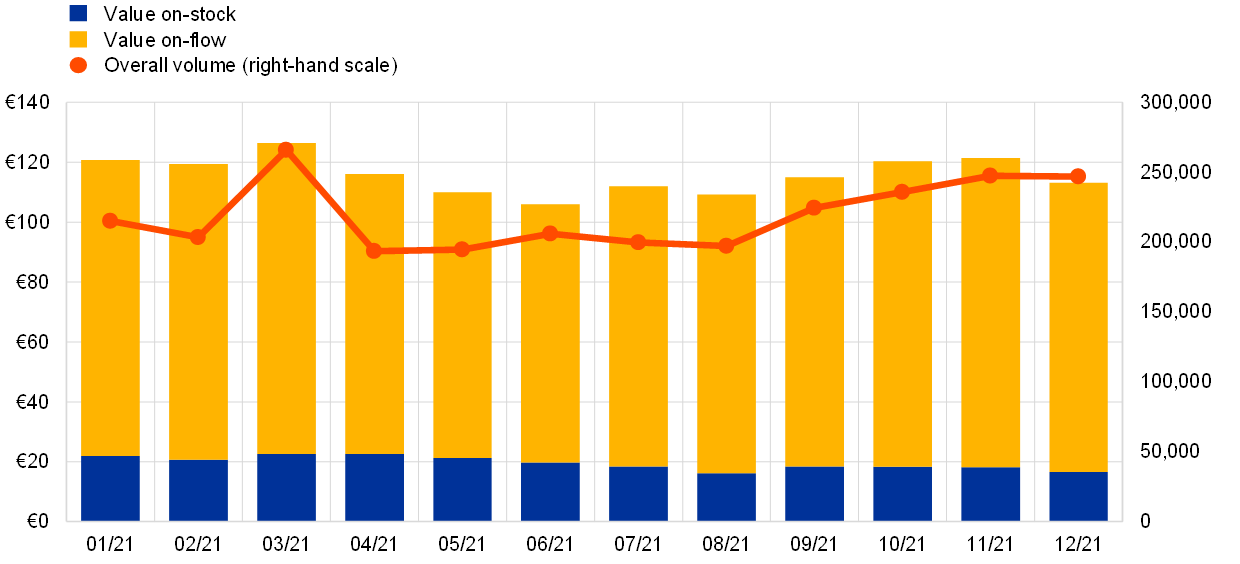

In 2021 the overall use of auto-collateralisation reached a daily average value of €115.79 billion, compared with €103.45 billion in 2020. Chart 16 shows the daily average value of auto-collateralisation per month, broken down by type. The daily average use of auto-collateralisation ranged between €106.00 billion in June and €126.41 billion in March.

Chart 16

Auto-collateralisation use by type in 2021

(left-hand scale: EUR billions, daily averages; right-hand scale: number of transactions, daily averages)

Source: T2S.

Note: The chart shows use of auto-collateralisation by national central banks.

The use of auto-collateralisation largely follows a similar pattern to that observed for daily DVP transactions settled throughout the year.

On average, 83.15% of the total value of auto-collateralisation was represented by auto-collateralisation on-flow (corresponding to €96.27 billion) and 16.85% by auto-collateralisation on-stock (corresponding to €19.51 billion). As in 2020, the use of auto-collateralisation on-stock remained relatively stable in 2021. In contrast, the use of auto-collateralisation on-flow displayed a more volatile pattern reaching a peak of €103.89 billion in March. The total monthly number of auto-collateralisation transactions ranged between 193,565 (in April) and 265,977 (in March).

In 2021 the overall use of auto-collateralisation on a monthly basis ranged between €2,310.47 billion in May and €2,907.20 billion in March. Chart 17 shows the monthly total value of auto-collateralisation, broken down by RTS and NTS, and the value of auto-collateralisation as a share of DVP transactions.

Chart 17

Real-time and night-time use of auto-collateralisation in 2021

(left-hand scale: EUR billions; right-hand scale: percentages, monthly totals)

Source: T2S.

Note: The chart shows use of auto-collateralisation by national central banks.

On average, 83.08% of auto-collateralisation transactions took place during RTS (corresponding to €2,068.28 billion) and 16.92% took place during NTS (€421.10 billion) in 2021. This compares to 78.61% and 21.39% respectively in 2020. The use of auto-collateralisation in RTS and NTS follows a similar pattern to that of the daily average value of transactions settled in T2S (see Chart 8). Auto-collateralisation use during RTS peaked in March (at €2,452.80 billion), while its use during NTS peaked in January (at €515.79 billion).

In 2021 the use of auto-collateralisation represented on average 17.54% of the total monthly value of DVP transactions settled and remained broadly stable over the year. This represents an increase compared with 2020 when this figure was 15.96%. As the chart shows, auto-collateralisation use as a share of DVP transactions reached its highest point in December (18.44%).

1.6 Other aspects related to settlement in T2S

1.6.1 Internally and externally matched settlement instructions

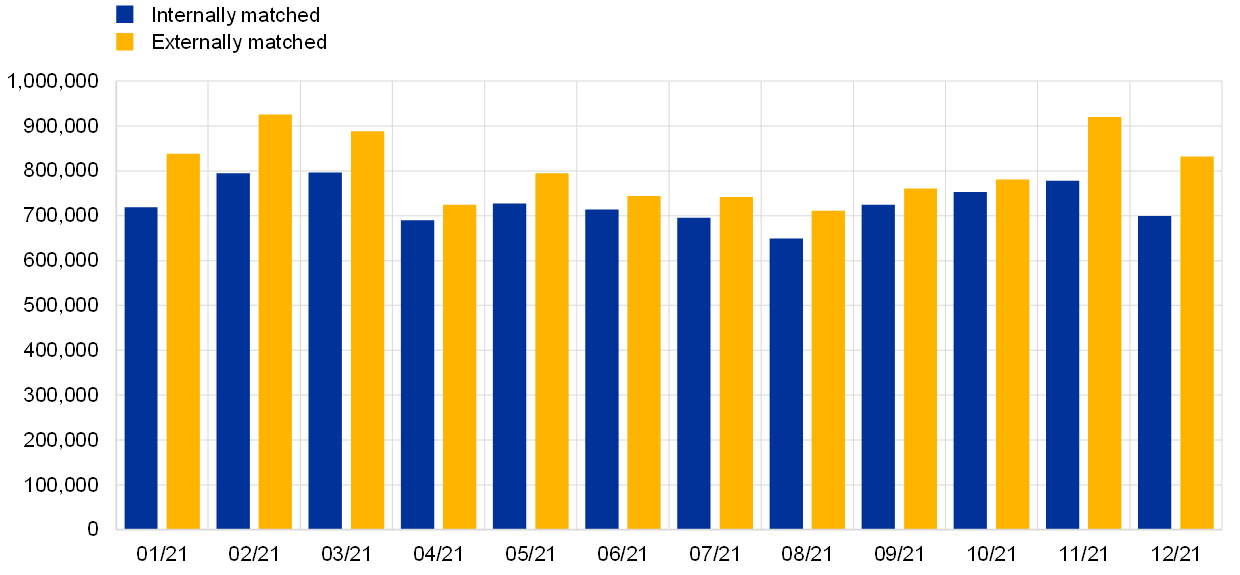

In order to settle a securities transaction, the delivering and receiving parties provide the necessary details in the form of settlement instructions. The two settlement instructions have to be compared to ensure that both parties agree on the terms of the transaction. If the comparison is successful, the two settlement instructions are matched, generating a new settlement transaction in T2S. This process can take place either inside T2S in the module performing the validation and matching of individual settlement instructions (life cycle management and matching – LCMM) or outside T2S. In the first case, the settlement instructions are defined as internally matched. In the second case, they are referred to as externally matched.

In 2021 728,354 settlement instructions were matched daily in T2S on average, compared with an average of 805,148 daily settlement instructions that were matched outside T2S. This represents an increase of 5.25% and 3.89% respectively compared with 2020. Chart 18 compares the daily average number of instructions that were internally and externally matched each month.

Chart 18

Internally and externally matched settlement instructions in 2021

(number of instructions, daily averages)

Source: T2S.

Overall, 47.50% of settlement instructions were internally matched, suggesting that slightly more than half (52.50%) reached T2S as already matched.

1.6.2 Intra-, cross- and external-CSD settlement

Investors can access different markets linked to T2S through multiple technical channels. Depending on the number of CSDs involved, it is possible to distinguish between intra-CSD, cross-CSD and external-CSD traffic.

- Intra-CSD traffic refers to securities transfers where the delivering and receiving parties belong to the same CSD

- Cross-CSD traffic takes place when the delivering and receiving parties belong to different CSDs

- External-CSD traffic occurs when the delivering and receiving parties belong to different CSDs, one of which is not in T2S

In T2S, intra-CSD transactions represent the majority of all settled transactions in terms of both volume and value.

As illustrated in Chart 19, in 2021 the daily average volume of intra-CSD transactions represented 98.42% (compared with 98.63% in 2020) of the total T2S settlement volume, while the daily average value of intra-CSD settlement represented 96.90% (97.26% in 2020) of the total T2S settlement value.

Chart 19

Intra-CSD settlement in 2021

(percentages, daily averages)

Source: T2S.

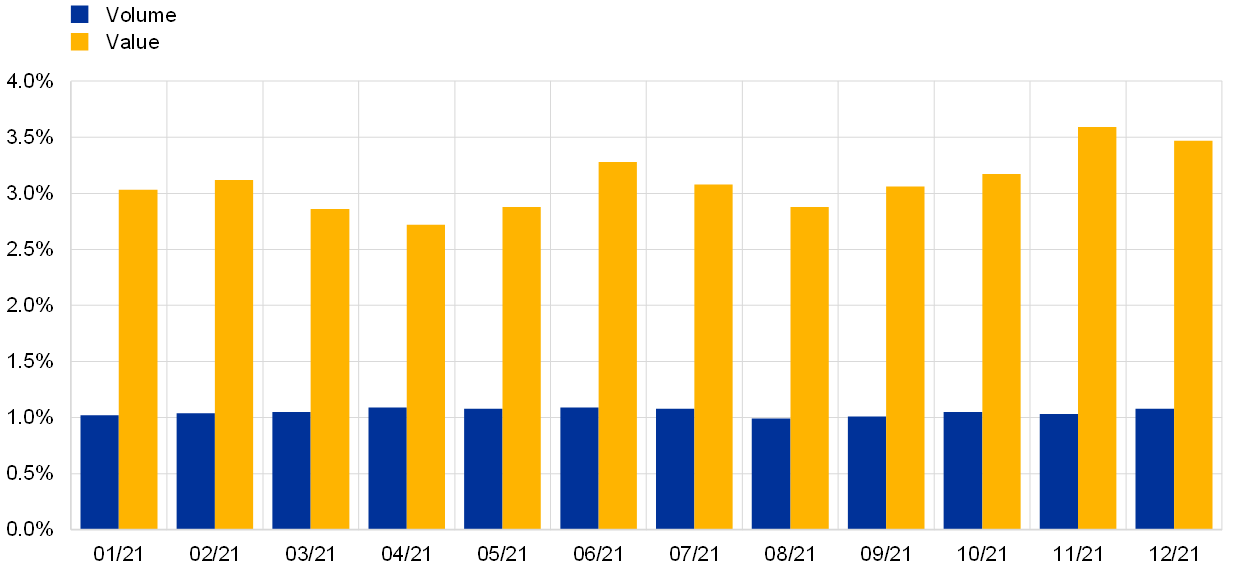

Only a very small percentage is attributable to cross-CSD traffic. Chart 20 shows the share of cross-CSD transactions compared with total value and volume of all transactions settled, in terms of daily average volume and value, in 2021.

Chart 20

Cross-CSD settlement in 2021

(percentages, daily averages)

Source: T2S.

In 2021 the daily average volume of cross-CSD settlement transactions represented 1.05% of the total T2S settlement volume (compared with 0.99% in 2020), while the daily average value of cross-CSD settlement transactions represented 3.10% of the total T2S settlement value (2.74% in 2020).

Considering that intra-CSD and cross-CSD transactions together accounted for 99.47% of the total volume and 100.00% of the total value, the share of external-CSD settlement was negligible in 2021.

1.7 Interaction between T2S and connected RTGS systems

At the start of each day liquidity is sent from the RTGS accounts in TARGET2 and Kronos2 (see Section 1.7.2) to the DCAs in T2S, while towards the end of RTS, at the latest, any remaining liquidity in DCAs is returned from T2S to the corresponding RTGS accounts. During the day, liquidity can be freely transferred from the RTGS systems to T2S and vice versa.

1.7.1 Interaction between T2S and TARGET2

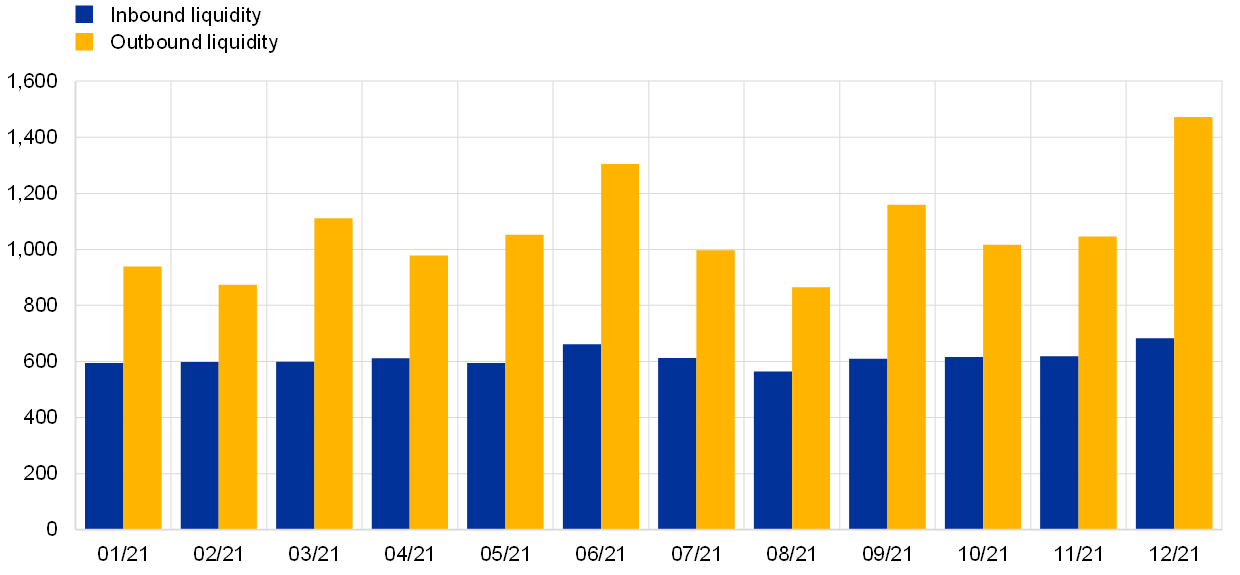

Inbound liquidity transfers are transfers from the TARGET2 RTGS accounts to the T2S DCAs, while outbound liquidity transfers are transfers from the T2S DCAs to the TARGET2 RTGS accounts.

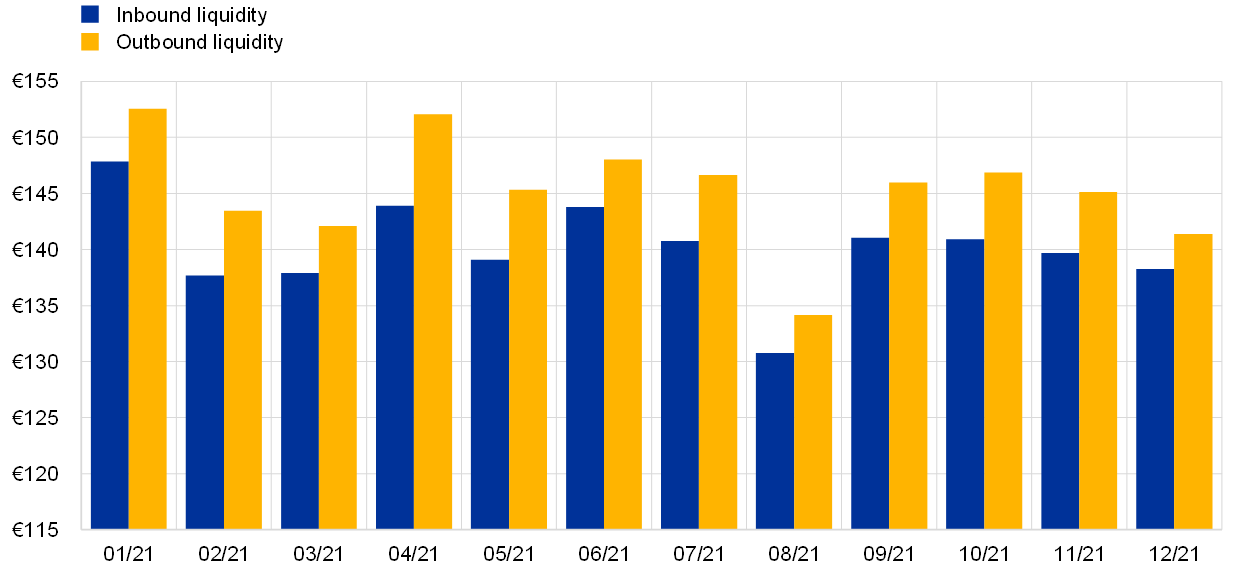

Chart 21 shows the daily average volumes of liquidity transfers between TARGET2 RTGS accounts and T2S DCAs in 2021. The daily average volume of inbound liquidity transfers from TARGET2 was 614, while the daily average volume of outbound liquidity transfers to TARGET2 was 1,073.

Chart 21

Volume of liquidity transfers between TARGET2 RTGS accounts and T2S DCAs in 2021

(number of transactions, daily averages)

Source: T2S.

Chart 22 shows the daily average value of liquidity transfers between TARGET2 RTGS accounts and T2S DCAs in 2021. The daily average value of inbound liquidity transfers from TARGET2 was €140.05 billion, while the daily average value of outbound liquidity transfers to TARGET2 was €145.18 billion. Any remaining balance on T2S DCAs stemming from the discrepancy between inbound and outbound liquidity transfers is automatically transferred back to TARGET2 as part of the RTS closure activities.

Chart 22

Value of liquidity transfers between TARGET2 RTGS accounts and T2S DCAs in 2021

(EUR billions, daily averages)

Source: T2S.

1.7.2 Interaction between T2S and Kronos2

Inbound liquidity transfers are transfers from the Kronos2 RTGS accounts to the T2S DCAs, while outbound liquidity transfers are transfers from the T2S DCAs to the Kronos2 RTGS accounts.[10]

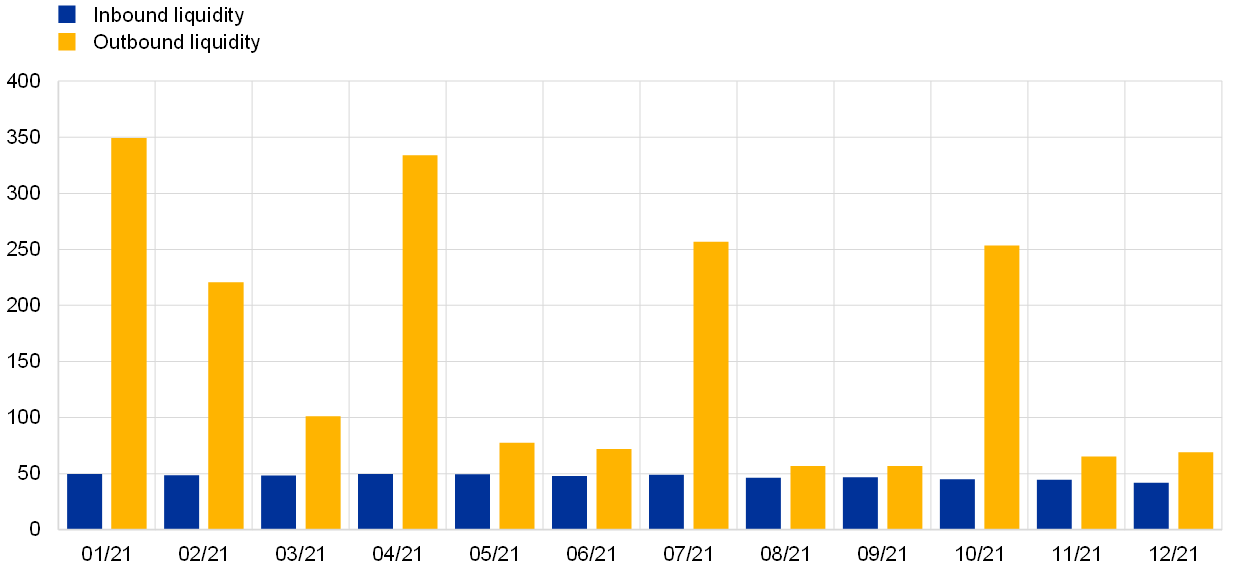

Chart 23 shows the daily average volumes of liquidity transfers between Kronos2 RTGS accounts and T2S DCAs in 2021. The daily average volume of inbound liquidity transfers from Kronos2 was 47 transfers, while the daily average volume of outbound liquidity transfers to Kronos2 was 156 transfers.

Chart 23

Volume of liquidity transfers between Kronos2 accounts and T2S DCAs in 2021

(number of transactions, daily averages)

Source: T2S.

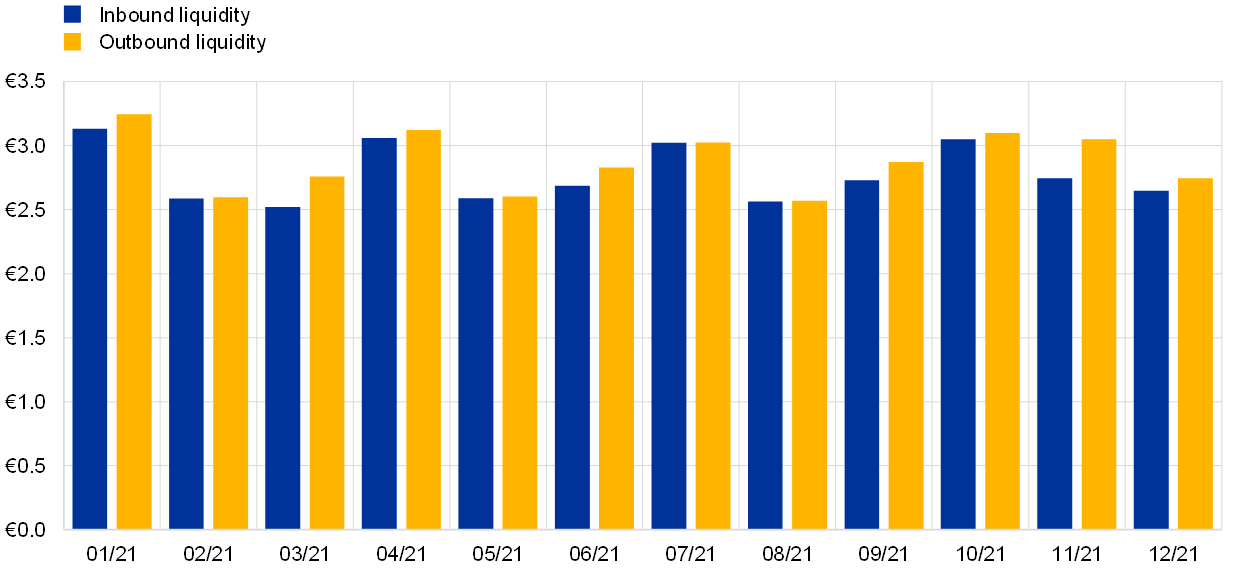

Chart 24 shows the daily average value of liquidity transfers between Kronos2 RTGS accounts and T2S DCAs in 2021. The daily average value of inbound liquidity transfers from Kronos2 was €2.77 billion (corresponding to DKK 21.31 billion), while the daily average value of outbound liquidity transfers to Kronos2 was €2.87 billion (corresponding to DKK 22.08 billion). Any remaining balance on T2S DCAs stemming from the discrepancy between inbound and outbound liquidity transfers is automatically transferred back to Kronos2 as part of the RTS closure activities.

Chart 24

Value of liquidity transfers between Kronos2 accounts and T2S DCAs in 2021

(EUR billions, daily averages)

Source: T2S.

2 T2S Service level and availability data

2.1 Technical availability

The Eurosystem pays particular attention to the proper functioning and operation of the T2S platform. The availability of the services is measured continuously and objectively at pre-defined components of T2S, throughout each Settlement Day, excluding the Maintenance Window.

The use of key performance indicators (KPIs) is one of the measures applied to demonstrate how effectively T2S is achieving its punctuality objectives. The punctuality of T2S is measured by calculating the real duration of the following three phases of the Business Day and comparing these against the expected target durations.

- Start of Day (SOD) – measures the elapsed time between the Start of Day phase (event BDCD) and the End of Start of Day (event ESOD)

- Night-Time Settlement including reporting (NTS + reporting) – measures the elapsed time between the start of the Night-Time Settlement (event C1P0) and the end of the NTS reporting (event ENTS)

- End of Day (EOD) – measures the elapsed time between the Start of the End of Day phase (event SEOD) and the End of Day Reports (event EEOR)

Table 2 summarises the average duration on a monthly basis of the different phases in a business day in comparison with the respective target durations. The figures show that the platform operated within the target expectations.

Table 2

Punctuality

2.2 Incidents in T2S

The Eurosystem is dedicated to ensuring the smooth operation of the T2S system during normal operations and to steering activities aimed at restoring the proper functioning of the T2S Services by mitigating the effects of incidents.

In 2021 the T2S platform experienced three major incidents, described as unplanned interruptions or reductions in the quality of an agreed service for which a Crisis Managers' conference call[11] was required. Each of the incidents was followed up with a detailed report, which serves as input for continuously improving the service and for increasing capabilities for preventing or mitigating them in the future. Paragraphs 1.2.1-1.2.3 provide more details about the three major incidents that occurred in 2021.

In comparison, in 2020 the T2S platform experienced 21 major incidents.

As illustrated in Chart 25, throughout the year 2021 the service level indicator, computed as the weighted average of the platform services, was below the committed KPI value of 99.7% on two occasions (June and November). Nonetheless, the overall results demonstrate a consistently high performance by the platform in the remaining months.

Chart 25

T2S Service level indicator in 2021

Source: T2S.

2.2.1 25 January incident

A major incident occurred in NTS on 25 January 2021, causing event C1S4 to be delayed.

The root cause of the issue related to a change in one of the database tables and was an unexpected consequence of the deployment of a minor change effected on 16 January 2021.This change proved to be inefficient with higher volumes.

An optimisation at database level allowed event C1S4 to run at its usual pace and it was finally completed at 01:28 CET.

As a follow-up to the incident, an alert was put in place to identify the possible reoccurrence of the issue with the access path, thus shortening the reaction time.

2.2.2 14 June incident

On 14 June 2021, following the deployment of T2S Release 5.0, the EOD reporting phase did not complete in its usual time frame. Instead, events closed and the BD change took place at 22:50 CET. The start of NTS (event C1P0) was scheduled 75 minutes afterwards, at 00:05 CET. Both the SOD and the NTS phases ran smoothly. Similar delays were also experienced on 15 June, after which a rollback of two changes stemming from Release 5.0 enabled a return to close to expected event durations.

2.2.3 22 November incident

On 22 November 2021, following the deployment of T2S Release 5.2, T2S dealt with an incident that prevented the proper closure of the Weekly Maintenance Window at a planned time of 02:30 CET on Monday, affecting outbound A2A traffic.

The incident was discovered by the operator through the technical monitoring tool at 05:10 CET. The operator was able to identify a missing job run that had caused the restart of the message brokers as the root cause. Once the jobs had been executed at around 07:45 CET, the outbound flow was resumed. In the meantime, a considerable queue of messages had accrued, which was fully processed by around 10:30 CET.

The late appearance of the alarm was caused by a wrong setting in the technical monitoring tool, which was subsequently fine-tuned to react to the changed weekly maintenance schedule introduced in Release 6.0.

3 T2S financial performance

3.1 Cost recovery objective

The financial position of T2S is determined by cost and revenue trends. The platform operates on a full cost recovery basis, meaning that all costs incurred should be covered by the revenues generated. The T2S pricing structure is defined in Schedule 7 of the T2S Framework Agreement and is also available in the TARGET Services Pricing Guide. T2S cost recovery is driven by three factors:

- the transaction volumes that are settled in T2S;

- the fees that are charged to T2S actors for using its services;

- the pre-defined T2S cost recovery period.

3.2 Financial performance of T2S

The overall financial position of T2S is detailed in the annual T2S financial statements, which are prepared in accordance with specific accounting policies established by the Market Infrastructure Board (MIB). In the interests of clarity, the financial information is presented in a similar manner to a profit and loss report (T2S operating statement) and a balance sheet report (T2S financial situation report).

The T2S operating statement shows yearly accumulated revenues (collected on a monthly basis) and yearly operational costs (paid on a quarterly basis). The T2S financial situation report provides a snapshot of relevant items in the asset and liability accounts.

For more information on the T2S financial position, see the latest T2S financial statement for 2020.[12]

3.3 Analysis of revenues collected in 2021

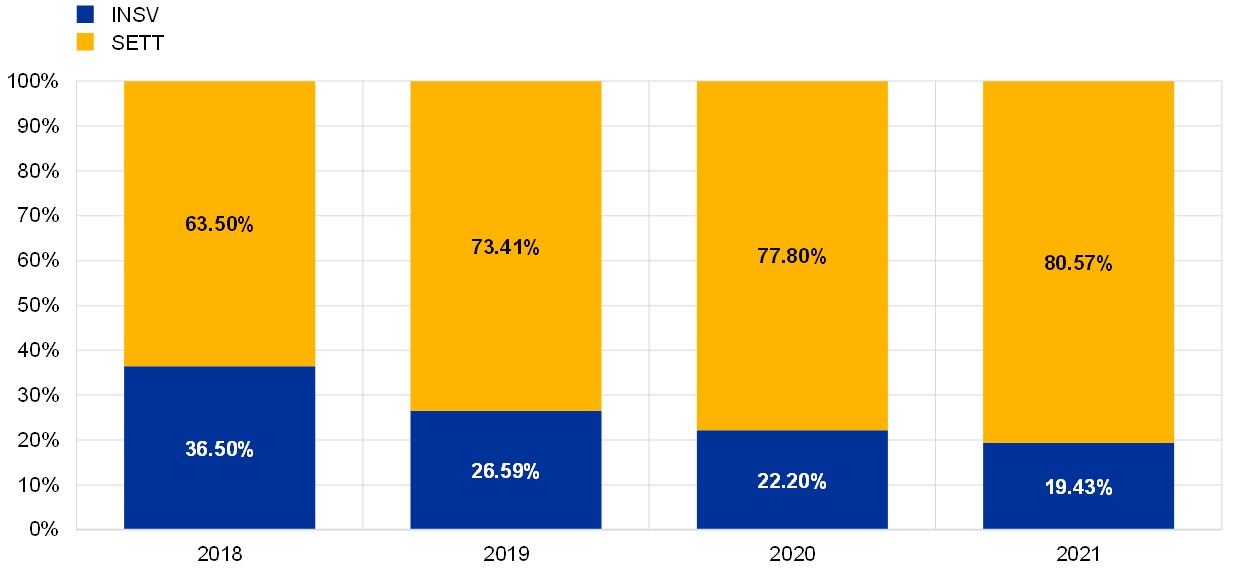

Chart 26 displays the relative split (in percentage terms) in T2S revenues between settlement services (SETT) and information services (INSV). The SETT revenue derives from the core settlement services that are available continuously during the night-time and real-time settlement periods, except for a short period during the maintenance window. Information services include services related to T2S information items, such as queries and reports. As part of this service, a CSD or an NCB may query any of its assigned accounts.

As shown in the Chart 26 below, in 2021 approximately four-fifths (80.6%) of T2S revenues stemmed from settlement services, while approximately one-fifth (19.4%) of T2S revenues stemmed from information services. The settlement services portion of T2S revenues has been increasing over the years (with a concomitant reduction in the information services portion), mainly owing to the gradual migration of some of the largest T2S markets in the platform’s first years of operation, and to the increase in T2S prices, which became effective in January 2019.

Chart 26

Share of T2S revenue split between settlement and information services

Source: T2S.

Table 3 displays the share (in percentage terms) of T2S revenues split between settlement services (SETT) and information services (INSV) detailed per tariff item. In 2021 the tariff items that contributed the most to the settlement services portion of T2S revenues were DVP (51.9%) and FOP (9.8%), while the tariff items that contributed the most to the information services portion of T2S revenues were charges related to Transmissions (10.1%) and Messages bundled into file (6.0%).

Table 3

Share of T2S revenue split between settlement and information services tariff items

4 T2S risk management and compliance

4.1 Risk management

Managing operational and information security risk is a key element of the governance structure of T2S.

The T2S governance is based on the ECB Guideline on T2S,[13] which lays down the responsibilities of the Governing Council and of the MIB in relation to T2S, including their risk management-related responsibilities. Thus, the Governing Council decides on the general operational aspects of T2S, including the TARGET services risk management framework. The MIB’s responsibilities[14] include (in full respect of the mandates of the European System of Central Bank (ESCB) committees) the preparation of a T2S risk management framework for Governing Council approval, its implementation and maintenance.

The T2S risk status and assessment, including risk analysis and mitigation measures (where relevant), is shared on a regular basis with the CSDs and the NCBs via the relevant fora: the Operations Managers Group (OMG), the Project Managers Group (PMG), the CSD Steering Group (CSG), the Securities Managers Group (SMG) and the Eurosystem Risk Management Forum (ERMF). As part of their own risk management activities, and complying with their own national regulatory requirements, CSDs and NCBs actively contribute to risk discussions by providing their views on existing risks and sharing information about any risks their participants and/or they themselves may pose to T2S.

Following a recommendation from the TARGET2 overseer, a common TARGET Services Risks Management Framework was adopted in 2021 for all TARGET services. The framework is based on a three-line model:[15] the TARGET services first line manages risks on a day-to-day basis and is made up of operational experts and managers whose main role is to ensure the efficient and smooth operation of TARGET services, while the TARGET services second line hosts the risk management function, and is composed of operational risk managers and experts, that are independent from operations and have a direct reporting line to the Steering Level. Both manage TARGET services operational risks and report regularly to the MIB, for their area of competence. Lastly, the third line is represented by the Eurosystem Internal Auditors’ Committee (IAC).

4.2 Oversight

The Eurosystem conducts the oversight of T2S as laid down in the Eurosystem oversight policy framework. The ECB has primary oversight responsibility for T2S and leads and coordinates all oversight activities. The oversight of T2S is conducted against a subset of the Principles for financial market infrastructures (PFMIs) established by the Committee on Payments and Market Infrastructures (CPMI) and the International Organization of Securities Commissions (IOSCO) as considered relevant for T2S by the Eurosystem. The PFMIs are the international standards for FMIs, i.e. payment systems, CSDs, securities settlement systems, central counterparties and trade repositories. Although T2S does not fall within the definition of an FMI provided in the PFMI report, the Eurosystem decided to apply the PFMIs to T2S as these principles relate to functions performed by T2S, i.e. the settlement and recording of securities transactions.

In the course of 2021, the operation function engaged in an active dialogue with the oversight function in order to follow up on outstanding oversight recommendations stemming from the various previous assessments. The oversight function acknowledged the progress made overall in 2021, as most of the actions planned for this year to address the oversight recommendations were completed (in particular those related to risk management, following the finalisation of the TARGET Services Risk Management Framework). The progress made in the implementation of the action plan to address the outstanding recommendations is constantly monitored by the ECB’s oversight function through regular exchanges between the two areas.

In 2021 the operation function shared the information requested by the ECB’s oversight function to support the continuous conduct of the oversight assessments of operational incidents and changes to the system implemented with T2S Releases 5.0 in June 2021 and 5.2 in November 2021. Following the implementation of the T2S Penalty Mechanism with T2S Release 4.2 in November 2020, the operation function regularly informed the oversight function about the status of the dry run activities being conducted in the production environment before the entry into force of the settlement discipline regime in February 2022. Furthermore, the operation function provided the oversight function with aggregated settlement statistics and information on operational and financial performance, as well as on risk management, testing and migration activities, with a view to supporting the oversight function’s monitoring of T2S activities that are relevant from an oversight perspective. With regard to cyber resilience, in 2021 the oversight function progressed in the assessment of T2S against the Eurosystem cyber resilience oversight expectations (CROE), and the operation function provided the necessary support to share the relevant documentation for the assessment and clarify specific aspects as required during regular exchanges. The oversight assessment report is scheduled to be finalised in March 2022 and the findings will then be shared with the operation function.

4.3 External examination

T2S services are performed on a single technical platform integrated with central banks’ RTGS systems for all participating currencies. Under the T2S Framework Agreement, the Eurosystem and the CSDs have agreed that the performance of T2S services must be subject to technical and operational examinations performed by an external examiner. These examinations provide an independent, third-party assessment to all participating CSDs based on the established industry norm (ISAE 3402). The external examiner must be a reputable, internationally active accounting firm.

The objective of these examinations is to provide the CSDs with reasonable assurance that (a) the organisation set up by the Eurosystem meets the obligations established in the Framework Agreement, and (b) the controls implemented by the Eurosystem are suitably designed, effective, and allow for efficient risk assessments to meet the security objectives.

As required by its statute, the Eurosystem conducted a public tender in 2018 and appointed an external examiner for T2S. The third external examination of T2S services took place in 2021, which looked into T2S services in 2020. For the first time, the agreed additional checks for the control and management of cyber-related risks were included in the 2020 examination. Apart from some exceptions, the external examiner confirmed that the T2S controls examined were both suitably designed and implemented and had operated effectively throughout the examination period from 1 January 2020 to 31 December 2020. The findings and recommendations from the 2020 examination report will be addressed in a comprehensive action plan, together with the open actions from the 2019 action plan.

The external examination for 2021 will be performed in 2022. These external examinations are a regular yearly exercise.

4.4 Special review

In December 2020 the ECB appointed Deloitte GmbH to conduct an independent review of five major information technology-related incidents (not cyber incidents) which occurred in 2020, affecting payment transactions and securities processing of TARGET services. The review aimed to identify the root causes of the incidents, draw more general lessons and propose recommendations in the following six key areas: (i) change and release management, (ii) business continuity management, (iii) fail-over and recovery tests, (iv) communication protocols, (v) governance, and (vi) data centre and IT operations.

On 28 July 2021 the ECB published Deloitte’s independent review. The report included a detailed description of the relevant incidents, the impact each had on TARGET services participants and the respective root causes. Deloitte also performed a thorough review of the procedures followed during the incidents, highlighting the weaknesses identified and issuing recommendations to address them.

In its response, the Eurosystem accepted Deloitte’s general conclusions and recommendations, and committed to decisively address them.

In the second half of 2021 the Eurosystem prepared an action plan to address the issues and recommendations raised by Deloitte in a timely manner. The action plan was further broadened to include recommendations issued by the Eurosystem oversight function and the Internal Audit Committee in relation to the TARGET services incidents that took place in 2020. In addition, for the recommendations on a specific TARGET service, the Eurosystem sought to design response actions that would apply holistically across the different TARGET services and the T2-T2S consolidated system due to go live in November 2022.

Measures addressing several recommendations were agreed or implemented in 2021, while most of the remaining measures will be implemented in 2022. For some recommendations, market participants were also involved to ensure that their views were taken into account. For that purpose, dedicated sessions with the Advisory Group on Market Infrastructures for Payments (AMI-Pay), the Advisory Group on Market Infrastructures for Securities and Collateral (AMI-SeCo) and the T2S CSG were organised. These groups will also be regularly updated on the implementation of the action plan until completion.

5 System evolution

5.1 Regular software updates

T2S evolution reflects changes in business needs, regulatory factors and applicable market standards, along with some changes considered to aspects of system maintenance. The typical T2S annual release schedule includes one major release and one minor release, including change requests and production problems, as well as two production problem releases, which only include fixes for production problems.

5.1.1 T2S releases in 2021 (R4.3, R5.0, R5.1 and R5.2)

On 20 February 2021 T2S Release 4.3 was deployed to fix 12 known production problems.

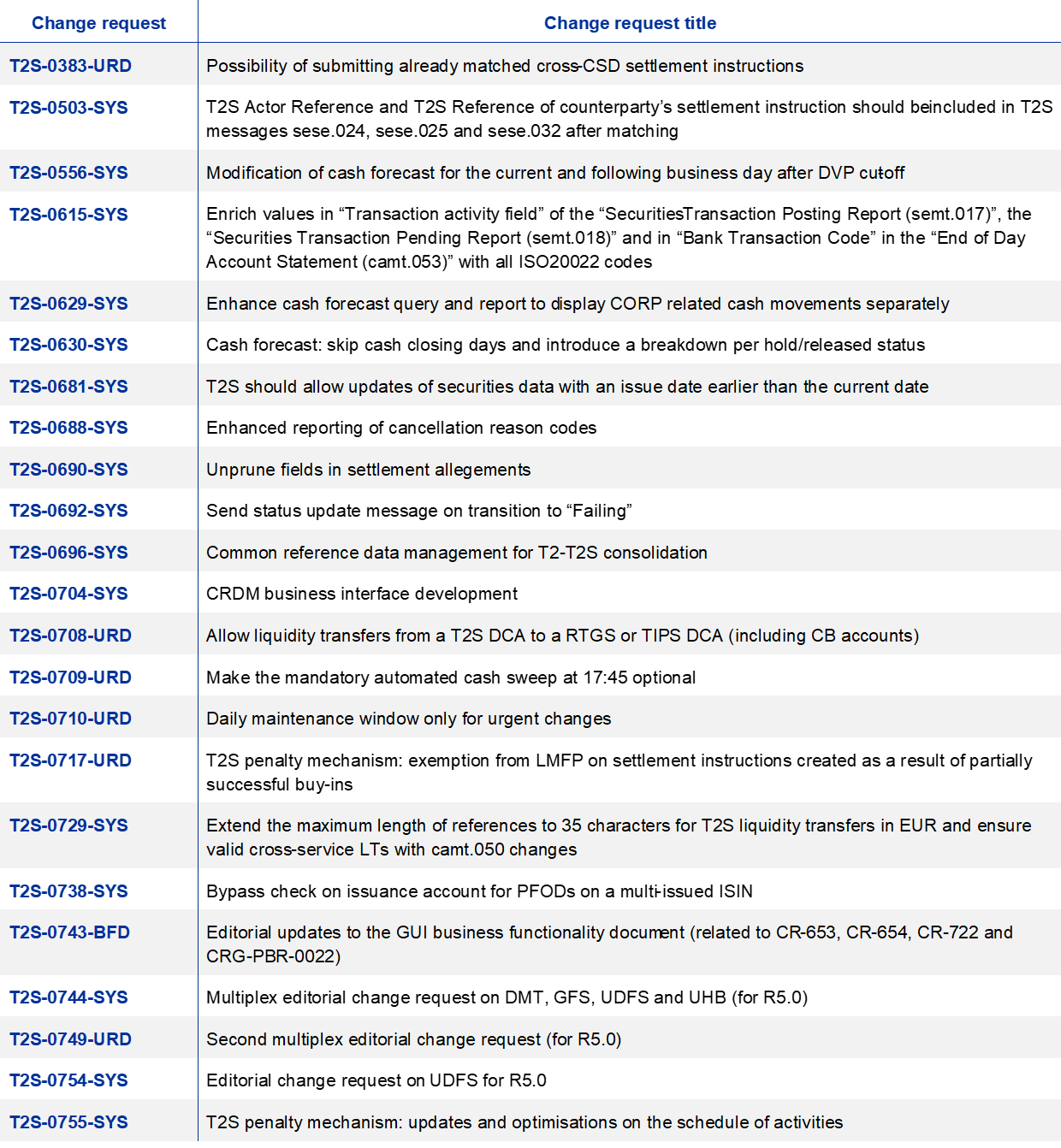

On 12 June 2021 the major T2S release, Release 5.0, went live with the implementation of 19 change requests (listed in Table 4 below), four editorial change requests and 27 fixes for known production problems. These changes covered a wide range of functional areas, including enhancements to the penalty mechanism, the cash forecast, and the deployment of several change requests related to the T2-T2S consolidation project, including making the maintenance window optional on weekdays.

A second release solely for production problems (Release 5.1) was deployed on 18 September 2021 to fix 16 production problems.

The minor release, T2S Release 5.2, deployed on 20 November 2021, included 13 change requests (listed in Table 5 below), one editorial change request and four fixes for production problems. The changes included enhancements to the T2S penalty mechanism (see Box 3) and to the T2S auto-collateralisation functionality, as well as additional tools for handling contingency situations.

The numbers of change requests deployed and production problems resolved in 2021 are shown in Table 6.

Table 4

T2S releases in 2021

Table 5

Change requests implemented in T2S Release 5.0

Table 6

Change requests implemented in T2S Release 5.2

5.1.2 Future system evolution

In 2022 changes to T2S will be delivered in two releases – Release 6.0 in July 2022 and Release 6.2 in November 2022. The changes planned for July 2022 will include the introduction of the new interface ESMIG and other common components developed for the T2-T2S consolidation project (see Section 5.4), as well as a new technology for the digital signature of manual actions in T2S (the non-repudiation of origin). In November 2022 the T2S release will coincide with the go-live of centralised liquidity management (CLM) and RTGS settlement services, and will also include enhancements to the management of reference data as well as changes in preparation of the future onboarding of end-investor markets on the platform.

In addition to the major and minor releases in 2022, two releases solely for production problems will be deployed, on 18 February 2022 (release 5.3) and 17 September 2022 (Release 6.1) respectively.

Although it is acknowledged that changes to the scope of the planned releases might be proposed in the future, the number of change requests planned for implementation in 2022 are shown in Table 7.

Table 7

T2S releases in 2022*

* Changes to the scope might be still possible.

For further information, a full list of T2S change requests and the detailed contents of each release can be found on the ECB’s website:

List of change requests

Project Managers Group – scope of T2S releases

Box 3

CSDR and Penalty Mechanism

In line with the CSD Regulation (CSDR), settlement discipline regime, which intends to apply harmonised measures at the EU level to address settlement fails, the penalty mechanism was included in T2S. The T2S penalty mechanism offers the identification, calculation and reporting of cash penalties to T2S CSDs based on the analysis of failed transactions in T2S, as well as a set of operational tools deemed necessary in this context. The T2S Penalty Mechanism Dry Run, which took place between 13 September 2021 and 31 January 2022, was a core activity in the readiness preparation for the CSDR settlement discipline regime. It gave the T2S community the possibility to test the T2S Penalty Mechanism in production conditions and detected a number of issues that could be fixed ahead of the regulatory deadline for entry into force on 1 February 2022. Furthermore, the exercise was suspended between 30 November and 3 December in order to concentrate resources in finalising the work on already identified fixes (testing and deployment) to improve the overall performance and stability of the penalty mechanism process. The main issues detected were performance issues that had an impact on the duration of the respective events. Owing to minor changes and technical optimisations the overall performance was improved, and the process became more stable.

5.2 Onboarding of new CSDs

T2S has also been constantly evolving in terms of participants. The following CSDs are currently working towards joining the T2S platform.

- Euroclear Finland. The migration of Euroclear Finland to T2S is scheduled for 11 September 2023 as the migration planning was endorsed by the MIB in July 2021. As an end-investor market, Euroclear Finland is expected to bring more than 2 million securities accounts to T2S, a significant increase compared with today’s operations.

- Euroclear Bank. Euroclear Bank signed[16] the T2S Framework Agreement on 21 December 2021 and is set to join T2S governance in the first quarter of 2022. The migration will take place in stages to ensure a smooth transition that enables Euroclear Bank to start offering its clients settlement services in central bank money. The exact date of migration has yet to be officially announced by Euroclear Bank.

- Središnje klirinško depozitarno društvo (SKDD). Under Croatia’s national plan for the changeover from the Croatian kuna to the euro (planned for 1 January 2023), the ECB team has been supporting Hrvatska narodna banka (the Croatian central bank) and SKDD with their preparations to join T2S. On 17 December 2021 SKDD delivered to the MIB its self-assessment for migrating to the T2S platform and the Eurosystem is expected to take a decision in the first half of 2022 and offer the T2S Framework Agreement to SKDD for signing.

- Bulgarian market. The ECB team has engaged in preliminary discussions with the private (Central Depository AD) and public (BNBGSSS) CSDs with regard to a possible T2S migration, in the context of Bulgaria potentially joining the euro in 2024. The self-assessment exercise and subsequent Eurosystem decision to offer the T2S Framework Agreement is expected to take place in 2022.

5.3 Exit activities of current CSDs

Complementary to the onboarding activities reported in the last chapter, in 2021 two CSDs initiated activities to exit from T2S.

- NCDCP. After NCDCP’s decision to stop operating as a CSD in December 2020 and submission of the termination notice to the ECB in June 2021, NCDPD successfully completed its exit activities on 12 November 2021.

- ID2S. Following the decision taken by the shareholders of ID2S on the 30 September 2021 to liquidate the company, ID2S requested the Eurosystem to initiate the exit process from T2S. In 2021 the process was initiated and the exit from the test environments was successfully conducted. The exit from the PROD environment is planned for February 2022.

5.4 Consolidation of TARGET2 and T2S

The T2-T2S consolidation project will replace the current TARGET2 with a new RTGS system and apply a CLM tool across all TARGET services (T2, T2S, TIPS and ECMS).

The functional specification phase of the project ended in 2020 following the publication of stable User Detailed Functional Specifications (UDFS) and User Handbooks (UHBs).

In 2021 the focus was on the update of these user specifications and preparing them for testing by incorporating change requests approved after the publication of the UDFS and UHB books. UDFS v2.2 was published in April and the different books of UHB v2.0 were published between May and December 2021.

The T2-T2S consolidation project has also published explainers and examples to help market participants better understand certain concepts by gathering information spread across different chapters or specifications books into single documents.

The next versions of the user specifications are expected to be published throughout 2022 before the go-live.

Migration, testing and readiness

The T2‑T2S consolidation project will go live in November 2022 following a “Big Bang” migration approach. This means that the current TARGET2 SSP will be discontinued at the time of the launch of the new T2 service. Transition in stages is not possible because the current SWIFT FIN Y-copy message flow used in TARGET2 cannot co-exist with the V-shape message flow that will be employed by the new T2 service. The V-shape set-up provides for network-agnostic connectivity and enhanced information security.

Following the Eurosystem Acceptance Testing (EAT) conducted up until early 2021, for the rest of the year the focus was on user testing. Central Bank Testing started in June 2021 and User Testing (UT) began in December 2021.

In 2022 testing will be stepped up and the migration process will be intensively practised in a set of go-live rehearsal tests, some of which will include the whole TARGET community. T2 participants will be invited to take part in dedicated testing campaigns, e.g. billing, ancillary system procedures. T2 participants will need to successfully perform the mandatory test cases in order to access the new platform.

The Community Readiness Reporting process follows the Community Readiness Framework which is outlined in the Migration, Testing and Readiness Strategy document. The readiness of the community to migrate in November 2022 will continue to be assessed against these milestones throughout the year in quarterly cycles.

Further details are available on the T2-T2S consolidation project page on the ECB’s website.

5.5 Eurosystem Collateral Management System

The Eurosystem Collateral Management System (ECMS) will be a single collateral management system used to manage eligible assets mobilised as collateral in Eurosystem monetary policy operations, replacing the current local collateral management systems.

The ECMS will interact with the CLM module in T2 to ensure the settlement of payments stemming from monetary policy operations, corporate actions and fees, and to update the relevant credit line.

In addition, the ECMS will interact with T2S for the settlement of securities and the management of the auto-collateralisation process. The resulting synergies are expected to benefit NCBs and all other ECMS players in their communities – counterparties, CSDs and tri-party agents (TPAs) – by contributing to the efficient exchange of securities, collateral and liquidity within the Eurosystem. It will be accessible via a single common interface across jurisdictions and facilitate the mobilisation of cross-border collateral.

In 2021 the software development phase was concluded and EAT and preparations for UT started. Ensuring that ECMS stakeholders have the necessary documentation for their internal adaptations was a priority in 2021. The catalogue of ECMS messages and credit claim schemas have been published on the ECB website, as well as detailed information on the future interaction between counterparties and the ECMS (authentication of instructions, potential business configurations, the U2A and A2A roles that counterparties may hold, the business rules and status codes that will apply to them in the ECMS). Key information on readiness milestones was provided to external stakeholders, and work commenced on preparing the testing and migration activities. The series of workshops with CSDs and TPAs launched in 2020 was continued in 2021, to facilitate the understanding and effective preparation of these significant stakeholders for the upcoming changes that the ECMS will make to the way in which collateral is managed by the Eurosystem. The ECMS is scheduled to go live on 20 November 2023.

Further details on the functions and features of the ECMS are available on the ECMS – professional use page on the ECB’s website.

© European Central Bank, 2022

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

For specific terminology please refer to the ECB glossary (available in English only).

PDF ISBN 978-92-899-5135-7, ISSN 2599-9257, doi:10.2866/835501, QB-CH-22-001-EN-N

HTML ISBN 978-92-899-5134-0, ISSN 2599-9257, doi:10.2866/702698, QB-CH-22-001-EN-Q

See Box 1, “Changes in the T2S statistical framework” in the T2S Annual Report 2019.

Liquidity transfers are excluded from the reported statistics, following the changes to the T2S statistical framework. See Box 1 of the T2S Annual Report 2019 for further details.

From 29 October 2018 all the charts related to settled value include transactions settled in Danish kroner. The traffic in Danish kroner is converted into euro at an exchange rate of DKK 1 to EUR 0.13.

As SRSE and FOP transactions do not imply a cash movement on a dedicated cash account, these two transaction types do not contribute to the calculation of value-based statistics. Moreover, liquidity transfers are excluded from the reported statistics, following the changes to the T2S statistical framework. See Box 1 of the T2S Annual Report 2019 for further details.

Until December 2019 settlement efficiency was computed in terms of platform settlement efficiency. The platform settlement efficiency indicator (PSEI) focused on the ability of the T2S platform to process transactions and helped determine whether T2S was performing as expected in terms of system configuration and performance of the optimisation algorithms. It thus comprised all settlement activities, including those automatically generated by T2S. From January 2020 settlement efficiency has been computed in terms of market settlement efficiency. The market settlement efficiency indicator (MSEI) aims at capturing the behaviour of T2S participants. Consequently, it mainly excludes transactions that are internally generated by T2S, transactions related to corporate actions and liquidity transfers from the calculation. However, it does include party-on-hold transactions.

A transaction is partially settled when only a part of the original quantity or amount is settled. Partial settlement is a functionality that can be used when the full quantity or amount needed for the transaction is not available. The remainder will be subject to recycling, with the aim of completing the settlement.

Late matching transactions are transactions that are matched either after their cut-off on the intended settlement day (ISD) has been reached or after their ISD. The delay is measured in terms of the number of business days between the matching timestamp and the ISD. In consequence, LMTs have been included in the CSDR settlement efficiency indicator only at the end of the day.

The analysis presented in this box focused on February 2021. Following the deployment of Release 5.0 in June 2021, the maintenance window has become optional on weekdays (see Section 5.1.1).

See Box 2 for details on the usage of the on-hold functionality by T2S actors.

Kronos2 is the RTGS system of Danmarks Nationalbank. The traffic in Danish kroner is converted into euro at an exchange rate of DKK 1 to EUR 0.13.