- RESEARCH BULLETIN NO. 67

- 28 February 2020

Public spending at the effective lower bound: how significant are the sustainability risks?

With monetary policy constrained by the effective lower bound (ELB), the debt sustainability implications of a fiscal expansion are a pressing concern. In a general equilibrium model of fiscal limits, we find that the adverse impact of a fiscal expansion on sustainability is muted at the ELB compared with normal times. Getting the timing of public spending increases right, however, is essential for containing sustainability risks.

Monetary-fiscal interactions at the effective lower bound

Risk-free interest rates are the main instruments used by central banks in normal times to achieve their inflation objectives and pursue economic stabilisation. By steering risk-free rates, however, central banks also affect the government’s capacity to service its debt both directly – through interest payments – and indirectly – through growth, inflation and, thus, tax revenues.

In the wake of the Great Recession, a binding effective lower bound (ELB) on interest rates constrained the regular conduct of monetary policy, thus enhancing the stabilisation role of fiscal policy. However, large stocks of debt, accumulated by governments during the prolonged recession, dramatically reduced their room for manoeuvre. As a result, in the current low rate environment, assessing the trade-off between the active use of a fiscal expansion – with the potential to boost economic activity and raise inflation – and the risk of triggering unsustainable public debt dynamics is of key importance (Blanchard, 2019).

In our working paper, we analyse the key ingredients for capturing the trade-off currently faced by fiscal and monetary authorities. Specifically, our model considers a fiscal authority’s limited ability to collect revenues (as higher distortionary taxes reduce output) and limited commitment to repay (as the government can restructure its debt). At the same time, we also take into account the ability of monetary policy to affect real economic activity (due to price rigidities), although this ability is limited at sufficiently low rates (by an endogenously binding ELB constraint).

The debt sustainability cost of the ELB

In our model, a government honours its obligations if it is able to do so. In other words, public debt is sustainable whenever it is below the government’s maximum ability to repay. This is what we call its fiscal limit.[2] Technically, the fiscal limit is computed as the present discounted value of all current and future maximum primary surpluses. As the economy is hit by unexpected shocks, there is no such thing as one fiscal limit: stochastic sequences of future shocks instead originate a distribution of fiscal limits. This distribution gauges the probability of a debt restructuring associated with a specific debt-to-output (or GDP) ratio. Moreover, the distribution of fiscal limits is state-contingent because new shocks arrive every period and, therefore, the distribution shifts every period (Bi, 2012, and Leeper and Leith, 2016).

To evaluate the increase in the probability of a debt restructuring due to the ELB –what we call the debt sustainability cost of the ELB – and how central banks can reduce it, we conduct two exercises. First, we explore the debt sustainability implications of a binding ELB constraint on monetary policy. To this end, we assume that a negative demand shock lowers the level of consumption desired by households, increases their savings and depresses economic activity. Depending on whether monetary policy is constrained or not, the nominal risk-free rate is then either pushed to its ELB (set to zero for practicality) or allowed to freely plunge below the ELB to stabilise the economy, respectively.

Chart 1

Fiscal limit distributions in normal times and at the ELB

Note: Reproduced from Battistini, Callegari and Zavalloni (2019), Figure 1. The chart illustrates how the fiscal limit distribution – i.e. the probability of a debt restructuring for a given debt-to-output ratio in the following quarter – varies in response to different initial unexpected shocks and under different assumptions for monetary policy. In particular, the chart shows the impact of the negative demand shock on the steady-state fiscal limit distribution (solid line), both when monetary policy is constrained (dashed line) and when it is not constrained by the ELB (dashed dotted line). The difference between the latter two cases can be interpreted as the debt sustainability cost of the ELB.

As shown in Chart 1, in the absence of constraints on monetary policy, the negative demand shock improves debt sustainability. The reason is that monetary policy responds by reducing the risk-free rate. The effect of a lower risk-free rate (implying a higher discounted value of future primary surpluses) more than offsets the lower economic activity (implying lower tax revenues), thus shifting the fiscal limit distribution to the right (from the solid line to the dashed dotted line). Introducing the ELB constraint, however, clearly worsens debt sustainability as the binding ELB impedes the beneficial effect of lower interest rates and amplifies the detrimental impact of lower taxes, shifting the fiscal limit distribution to the left (from the dashed dotted line to the dashed line). Ultimately, this shift constitutes the debt sustainability cost of the ELB.

There are ways, however, for monetary policy to tame the adverse consequences of the ELB for debt sustainability. In our second exercise, we look at the debt sustainability implications of a higher degree of activeness of monetary policy, defined as the responsiveness of the risk-free rate to deviations of inflation from its target. As in our first exercise, we concentrate on a situation in which monetary policy is constrained and a negative demand shock pushes the economy to the ELB.

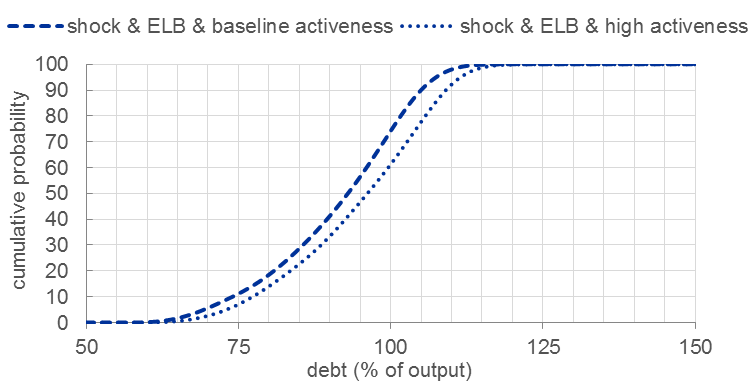

Chart 2

Fiscal limit distributions at the ELB with degrees of monetary policy activeness

Note: Reproduced from Battistini, Callegari and Zavalloni (2019), Figure 3. The chart on the right shows the implications of different degrees of monetary policy activeness on the fiscal limit distribution, given the baseline calibration (dashed line) and low value (dotted line) for the inflation-targeting coefficient in the Taylor rule.

Chart 2 shows that the degree of activeness of monetary policy – despite affecting the behaviour of the central bank only away from the ELB – also matters during periods of constrained monetary policy. In fact, a more active central bank reduces the economic distortions generated by future inflation fluctuations. Its effect is also visible when the economy is initially at the ELB, as a higher degree of monetary policy activeness shifts the fiscal limit distribution to the right (from the dashed line to the dotted line).

What is the trade-off for public spending at the ELB?

Our analysis above shows that, all else equal, debt is harder to sustain at the ELB. This is particularly consequential for high-debt countries, which should take advantage of low rates to rein in excessive deficits and reduce debt. Nevertheless, our model indicates that, taking into account all the general equilibrium effects, the low rate environment of the ELB both enhances the macroeconomic impact of a public spending shock and, at the same time, largely mutes debt sustainability concerns – yet without removing them entirely, especially for high-debt countries.

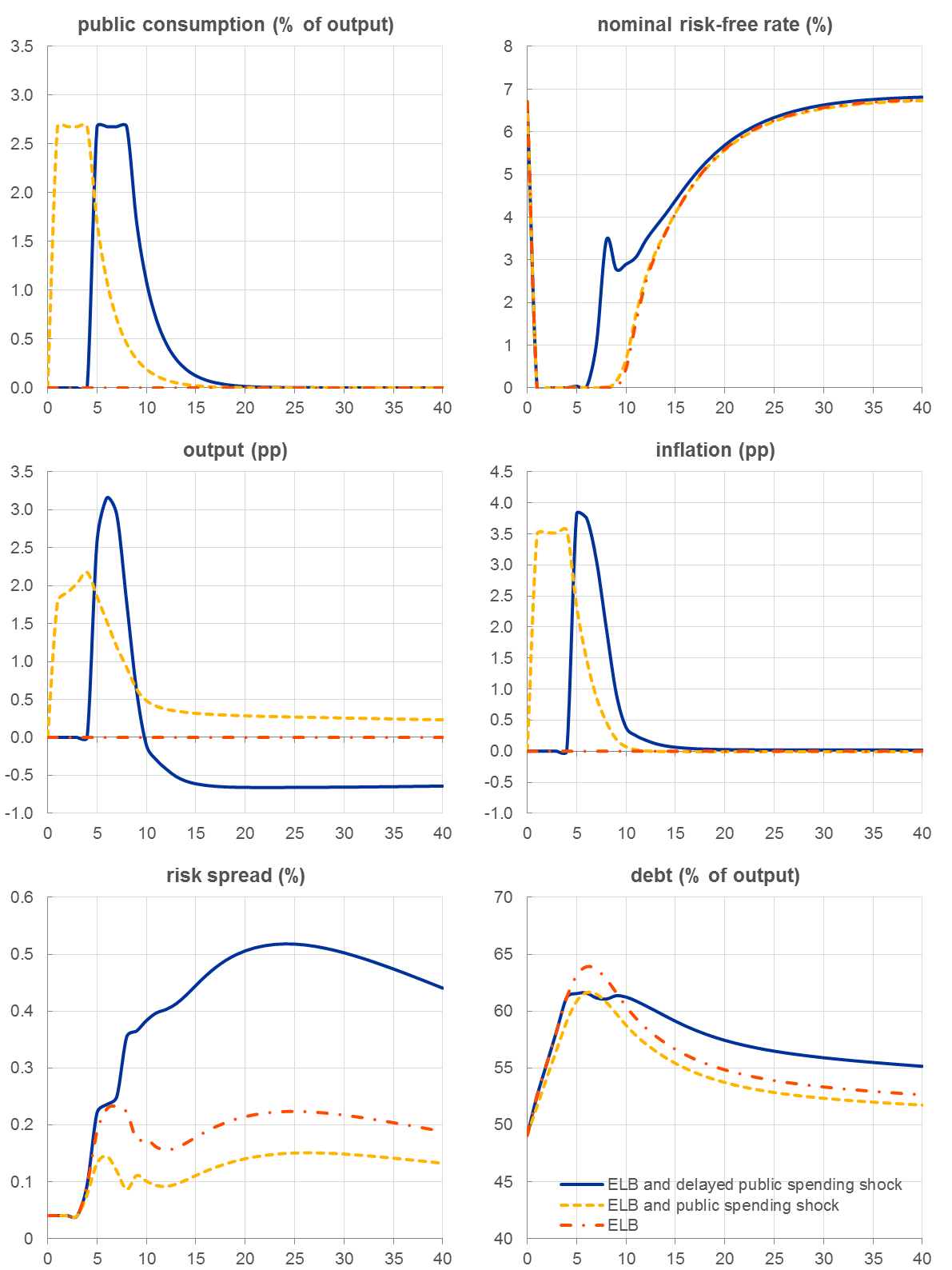

Chart 3

Impact of government spending shocks with different timing at the ELB

Note: Reproduced from Battistini, Callegari and Zavalloni (2019), Figure 8. In all the charts, the x-axis refers to time expressed in quarters. Output (as a percentage deviation from its steady-state level) and inflation are reported in (percentage point) differences from their values at the ELB (their dashed dotted red lines are at zero). Moreover, all variables are expressed in annualised terms.

Looking at Chart 3, in our calibration targeting an average EU-14 country, we let a series of unexpected negative demand shocks hit the economy and push the risk-free rate down to its ELB for four quarters (dashed dotted line). The ensuing recession and deflation (not directly observable in the Chart) force the government to increase public debt, thus raising the risk spread for a long time. However, a series of deficit-financed public spending shocks during the prolonged period at the ELB (dashed yellow line) would support both inflation and output and, at the same time, reduce the risk spread compared to a situation without fiscal expansion. Importantly, our model shows that this concurrent improvement in macroeconomic stabilisation and debt sustainability through an unanticipated fiscal expansion occurs because of the large long-run fiscal multiplier of public spending in times of binding ELB (as highlighted by Christiano, Eichenbaum and Rebelo, 2011) and despite the debt sustainability cost of the ELB.

Getting the timing of the spending increase right is, however, essential. An excessively delayed series of public spending shocks (solid blue line) – starting when the risk-free rate is still low, but continuing well into a period when monetary policy can react to inflationary pressures – would not benefit from the large fiscal multipliers of the ELB. In contrast, a delayed fiscal expansion could lead to soaring sovereign spreads and debt levels and, eventually, long-run output losses. As these dynamics would be further amplified in the presence of higher initial debt levels, the right timing for a fiscal expansion is crucial, especially for highly indebted countries.

Concluding remarks

The active use of fiscal policy for stabilisation purposes should always follow a careful assessment of the impact on public debt sustainability. This assessment, however, changes during periods of binding ELB and depends on the degree of activeness of the central bank. A muted trade-off in times of binding ELB may imply the possibility for a government to obtain gains in terms of both sustainability and stabilisation after a fiscal expansion, but getting the timing right – that is, avoiding excessive delays in its implementation – is essential. Our results are specific to a closed economy model and do not necessarily apply to a currency union setting, where the stabilisation/sustainability trade-off is also influenced by the strategic behaviour of the member countries, including, inter alia, their possible incentives to “free ride” on the safety premium of countries with better fundamentals.

References

Battistini, N., Callegari, G. and Zavalloni, L. (2019), “Dynamic fiscal limits and monetary-fiscal policy interactions”, ECB Working Paper Series, No. 2268, April.

Bi, H. (2012), “Sovereign default risk premia, fiscal limits, and fiscal policy”, European Economic Review, Vol. 56, pp. 389-410.

Blanchard, O.J. (2019), “Public debt and low interest rates”, American Economic Review, Vol. 109(4), pp. 1197-1229.

Christiano, L., Eichenbaum, M. and Rebelo, S. (2011), “When is the government spending multiplier large?”, Journal of Political Economy, Vol. 119(1), pp. 78-121.

Leeper, E.M. and Leith, C. (2016), “Understanding inflation as a joint monetary-fiscal phenomenon”, Handbook of Macroeconomics, Vol. 2, Chapter 30, pp. 2305-2415.

- This article was written by Niccolò Battistini (Economist, Directorate General Economics, Business Cycle Analysis Division) and Giovanni Callegari (Economist at Autonomy Capital Research LLP). It is based on ECB Working Paper 2268 “Dynamic fiscal limits and monetary-fiscal policy interactions”. The authors gratefully acknowledge the comments of Bartosz Maćkowiak, Alberto Martin, Leo von Thadden and Zoë Sprokel. The views expressed here are those of the authors and do not necessarily represent the views of the European Central Bank, the Eurosystem, or Autonomy Capital Research LLP (or its affiliates).

- In our model, the government does not assess the welfare implications of repaying (or not repaying) its debt. Thus, the government reneges on its obligations only if it is unable to repay due to insufficient resources, rather than unwilling to do so due to welfare (or strategic) considerations.