- STATISTICAL RELEASE

Euro area quarterly balance of payments and international investment position:

fourth quarter of 2022

5 April 2023

- Current account deficit at €137 billion (1.0% of euro area GDP) in 2022, down from €285 billion surplus (2.3% of GDP) a year earlier

- Geographical counterparts: largest bilateral current account deficits vis-à-vis China (€170 billion) and Russia (€79 billion) and largest surpluses vis-à-vis United Kingdom (€137 billion) and Switzerland (€72 billion)

- International investment position showed net assets of €265 billion (2.0% of euro area GDP) at end of 2022

- Euro area financial assets vis-à-vis Russia amounted to €308 billion (0.9% of euro area external assets) at end of the fourth quarter of 2022, down by 21% since end of previous quarter

Current account

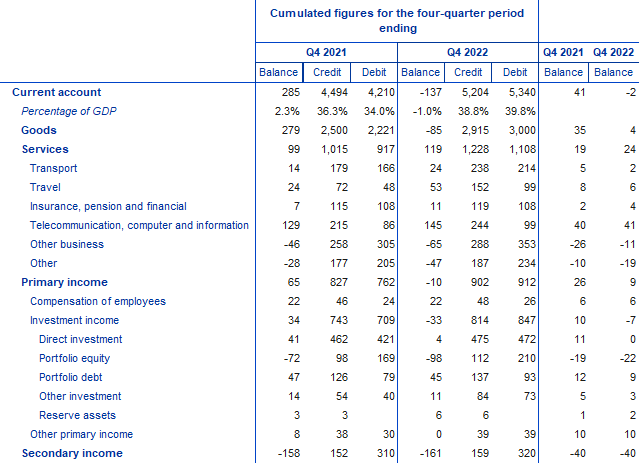

The current account of the euro area recorded a deficit of €137 billion (1.0% of euro area GDP) in 2022, after recording a surplus of €285 billion (2.3% of GDP) in 2021 (Table 1). This change was mainly driven by switches in the goods balance – from a surplus of €279 billion to a deficit of €85 billion – and, to a lesser extent, in the primary income balance – from a surplus of €65 billion to a deficit of €10 billion. Moreover, the deficit in secondary income edged up from €158 billion to €161 billion. These developments were slightly offset by a larger surplus for services (up from €99 billion to €119 billion).

The larger surplus for services in 2022 was mainly due to widening surpluses for travel services (from €24 billion to €53 billion), telecommunication, computer and information services (from €129 billion to €145 billion) and transport services (from €14 billion to €24 billion), while larger deficits were recorded for other business services (from €46 billion to €65 billion) and other services (from €28 billion to €47 billion).

The switch in the primary income balance from a surplus to a deficit was mainly due to a lower surplus in direct investment income (from €41 billion to €4 billion), a larger deficit in portfolio equity income (from €72 billion to €98 billion) and a decline in the surplus for other primary income (from €8 billion to €0.1 billion), the latter mostly related to an increase in payments to the EU institutions.

Table 1

Current account of the euro area

(EUR billions, unless otherwise indicated; transactions during the period; non-working day and non-seasonally adjusted)

Source: ECB.

Notes: “Equity” comprises equity and investment fund shares. Discrepancies between totals and their components may arise from rounding.

Data on the geographical counterparts of the euro area current account (Chart 1) show that in 2022 the euro area recorded its largest bilateral deficits vis-à-vis China (€170 billion, up from €83 billion in 2021), Russia (€79 billion, up from €22 billion) and the residual group of other countries (€76 billion, after a surplus of €124 billion). The largest bilateral surpluses were recorded vis-à-vis the United Kingdom (€137 billion, down from €158 billion) and Switzerland (€72 billion, up from €68 billion). Furthermore, in 2022 the euro area recorded an annual bilateral current account deficit of €37 billion vis-à-vis the United States, following a surplus of €57 billion in 2021.

The most significant changes in the geographical components of the current account in 2022 relative to 2021 were as follows. The goods balance vis-à-vis the residual group of other countries turned from a surplus of €38 billion to a deficit of €188 billion. This was partly due to a larger goods deficit with Norway (up from €14 billion to €75 billion) and increased imports from countries within the Organization of the Petroleum Exporting Countries, in both cases driven by larger imports of energy products. The deficit vis-à-vis China increased from €112 billion to €191 billion and the deficit vis-à-vis Russia rose from €40 billion to €92 billion, mainly on account of higher prices for imported energy products.

In services, the surplus vis-à-vis the United Kingdom widened (from €29 billion to €52 billion), mostly owing to exports of travel services, while the deficit vis-à-vis the United States increased (from €81 billion to €126 billion) mainly on account of larger imports of research and development services. In primary income, a larger deficit was recorded vis-à-vis the United States (up from €41 billion to €89 billion), while the primary income balance vis-à-vis the United Kingdom switched from a surplus of €22 billion to a deficit of €11 billion. In secondary income, the deficit vis-à-vis the EU Member States and EU institutions outside the euro area decreased from €90 billion to €86 billion.

Chart 1

Geographical breakdown of the euro area current account balance

(four-quarter moving sums in EUR billions; non-seasonally adjusted)

Source: ECB.

Note: “EU non-EA” comprises the non-euro area EU Member States and those EU institutions and bodies that are considered for statistical purposes as being outside the euro area, such as the European Commission and the European Investment Bank. “Other countries” includes all countries and country groups not shown in the chart, as well as unallocated transactions.

International investment position

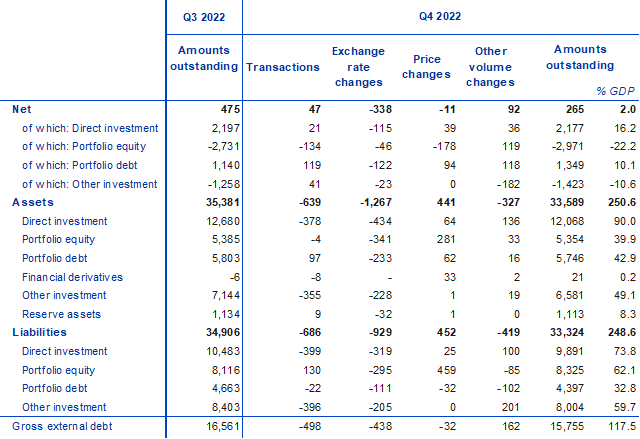

At the end of the fourth quarter of 2022, the international investment position of the euro area recorded net assets of €265 billion vis-à-vis the rest of the world (2.0% of euro area GDP), down from €475 billion in the previous quarter (Chart 2 and Table 2).

Chart 2

Net international investment position of the euro area

(net amounts outstanding at the end of the period as a percentage of four-quarter moving sums of GDP)

Source: ECB.

The €210 billion decrease in net assets reflected changes in the various investment components. Larger net liabilities were recorded in portfolio equity (up from €2.73 trillion to €2.97 trillion) and in other investment (up from €1.26 trillion to €1.42 trillion), while lower net assets were recorded in direct investment (down from €2.20 trillion to €2.18 trillion). These were partly offset by an increase in net assets in portfolio debt (up from €1.14 trillion to €1.35 trillion).

Table 2

International investment position of the euro area

(EUR billions, unless otherwise indicated; amounts outstanding at the end of the period, flows during the period; non-working day and non-seasonally adjusted)

Source: ECB.

Notes: “Equity” comprises equity and investment fund shares. Net financial derivatives are reported under assets. “Other volume changes” mainly reflect reclassifications and data enhancements. Discrepancies between totals and their components may arise from rounding.

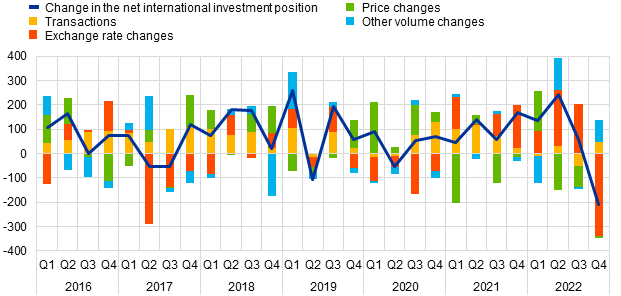

The developments in the euro area’s net international investment position in the fourth quarter of 2022 were driven mainly by large negative net flows from exchange rate changes – reflecting the appreciation of the euro in nominal effective terms – and, to a lesser extent, price changes. These were partly offset by other volume changes and transactions (Table 2 and Chart 3).

The increase in net liabilities for portfolio equity was mostly driven by negative net flows for price changes (as the price increase was larger in liabilities than in assets), transactions and, to a lesser extent, exchange rate changes, which were partially offset by positive net other volume changes (Table 2). The increase in net assets for portfolio debt resulted from positive net transactions, other volume changes and price changes, which were partially offset by negative net exchange rate changes. In direct investment, negative net flows owing to exchange rate changes were almost offset by positive net price changes, other volume changes and transactions, while in other investment net liabilities increased, mainly as a result of negative other volume changes.

At the end of the fourth quarter of 2022 the gross external debt of the euro area amounted to €15.8 trillion (approximately 118% of euro area GDP), down by €806 billion compared with the previous quarter.

Chart 3

Changes in the net international investment position of the euro area

(EUR billions; flows during the period)

Source: ECB.

Note: “Other volume changes” mainly reflect reclassifications and data enhancements.

This release provides an overview of the euro area’s international investment position vis-à-vis residents of Russia at the end of the fourth quarter of 2022 and reports the main changes compared with the previous quarter (Table 3).[1] Euro area financial assets vis-à-vis Russia amounted to €308 billion (0.9% of euro area external assets) at the end of the fourth quarter of 2022, a 21% decrease since the end of the previous quarter. This decrease was broad-based across functional categories, with the largest contributions due to euro area direct investment, other investment and portfolio investment assets in Russia. At the same time, the euro area recorded liabilities of €469 billion vis-à-vis Russia (1.4% of total external liabilities), a decline of 7% compared with the previous quarter, driven mainly by lower liabilities in other investment.

Table 3

International investment position of the euro area – geographical breakdown vis-à-vis Russia

(EUR billions, unless otherwise indicated; at the end of the period; non-working day and non-seasonally adjusted)

Source: ECB.

Notes: “Equity” comprises equity and investment fund shares. “Total assets/liabilities” refer to the sum of direct investment, portfolio investment, other investment and financial derivatives. Reserve assets are not included in the total and financial derivatives are reported separately in gross terms under assets and liabilities. Discrepancies between totals and their components may arise from rounding. Percentage changes refer to changes between the end of the previous quarter and the end of the current quarter.

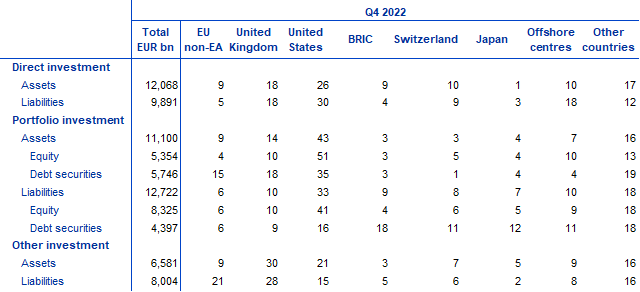

At the end of 2022 euro area direct investment assets were €12.1 trillion, 26% of which was invested in the United States and 18% in the United Kingdom (see Table 4). Euro area direct investment liabilities were €9.9 trillion, with 30% being investments from the United States, 18% from the United Kingdom and 18% from offshore centres.

In portfolio investment, euro area holdings of foreign securities amounted to €5.4 trillion in equity and €5.7 trillion in debt at the end of 2022. The largest holdings of equity securities were in securities issued by residents of the United States (accounting for 51%), followed by those issued by residents of the United Kingdom and offshore centres (each accounting for 10%). In debt securities, the largest euro area holdings were in securities issued by residents of the United States (accounting for 35%), the United Kingdom (18%) and the EU Member States and EU institutions outside the euro area (15%).

On the portfolio investment liabilities side, non-residents’ holdings of securities issued by euro area residents stood at €8.3 trillion in equity and at €4.4 trillion in debt at the end of 2022. The largest holder countries of euro area equity securities were the United States (41%) and the United Kingdom (10%), while in euro area debt securities the largest holders were the BRIC group of countries (18%), the United States (16%) and Japan (12%).

In other investment, euro area residents’ claims on non-residents amounted to €6.6 trillion, 30% of which was vis-à-vis the United Kingdom and 21% vis-à-vis the United States. Euro area other investment liabilities amounted to €8.0 trillion, with the United Kingdom accounting for 28%, while the shares of the EU Member States and EU institutions outside the euro area and the United States were 21% and 15% respectively.

Table 4

International investment position of the euro area – geographical breakdown

(as a percentage of the total, unless otherwise indicated; at the end of the period; non-working day and non-seasonally adjusted)

Source: ECB.

Notes: “Equity” comprises equity and investment fund shares. “EU non-EA” comprises the non-euro area EU Member States and those EU institutions and bodies that are considered for statistical purposes as being outside the euro area, such as the European Commission and the European Investment Bank. The “BRIC” countries are Brazil, Russia, India and China. “Other countries” includes all countries and country groups not listed in the table as well as unallocated positions.

First dissemination of additional details

With this statistical release, additional details as included in the amended ECB External Statistics Guideline ECB/2018/19 are disseminated for the first time. These new series include additional sector breakdowns by providing separate data for investment funds; insurance corporations and pension funds; other financial institutions; non-financial corporations; and combined households and non-profit institutions serving households. Moreover, in direct investment, additional details for debt instruments are now available for debt securities; loans; and trade credits and advances. In addition, euro area bilateral data are now available vis-à-vis Argentina, Australia, Indonesia, Mexico, Norway, Saudi Arabia, South Africa, South Korea and Türkiye.

Data revisions

This statistical release incorporates revisions to the data since the first quarter of 2013, reflecting the inclusion of Croatia in the euro area aggregates, which now cover all 20 members of the euro area. These revisions did not significantly alter the figures previously published, which referred to the first 19 members of the euro area only.

Next releases

- Monthly balance of payments: 19 April 2023 (reference data up to February 2023)

- Quarterly balance of payments and international investment position: 4 July 2023 (reference data up to the first quarter of 2023)

For queries, please use the Statistical information request form.

Notes

- Data are neither seasonally nor working day-adjusted. Ratios to GDP (including in the charts) refer to four-quarter sums of non-seasonally and non-working day-adjusted GDP figures.

- Hyperlinks in this press release lead to data that may change with subsequent releases as a result of revisions.

- Balance of payments statistics are now released using the "BPS" dataset which includes an additional 17th dimension in its data structure definition to specify the type of resident entity.

Table 3 does not include reserve assets in the total euro area external asset positions and financial derivatives are reported in gross terms instead of net terms.