Potential output in the post-crisis period

Published as part of the ECB Economic Bulletin, Issue 7/2018.

Potential output is typically seen by economic analysts as the highest level of economic activity that can be sustained over the long term. Changes in potential output can be driven by factors such as labour supply, capital investment and technological innovation. Recent estimates by international institutions suggest that the euro area economy is currently operating close to its potential. The ongoing economic expansion appears to have largely absorbed the spare capacity created by the global financial crisis and the sovereign debt crisis. At the same time, the estimated rate of potential output growth also appears to have recovered most of its pre-crisis momentum, underpinned mainly by an expansion of the labour force, a decline in trend unemployment and stronger productivity gains. Looking ahead, projections by international institutions suggest that actual euro area GDP growth will continue to outpace potential growth in the near term. Hence, supply constraints are likely to become increasingly binding going forward, which would be conducive to a gradual strengthening of euro area inflation.

1 Introduction

Potential output is a key economic concept as its evolution determines how fast an economy can grow in a sustainable way. It is typically thought of as the highest level of economic activity that can be sustained by means of the available technology and factors of production, in particular labour and capital, without creating inflationary pressure. Institutions that facilitate and encourage innovation, factor accumulation and an efficient allocation of resources are particularly conducive to faster growth in potential output. Therefore, sound structural policies play a key role in promoting sustainable growth.

For central banks, potential output estimates can support the analysis of the state of the business cycle and the implications for the dynamics of wages and prices. If economic activity exceeds the level of potential output, the increased factor utilisation will typically put upward pressure on factor costs and ultimately on consumer prices. Similarly, such price pressures tend to recede if economic activity falls below the level of potential output. The output gap, defined as the percentage deviation of the actual level of output (i.e. real GDP) from the potential level, is therefore often regarded as an indicator of the state of the business cycle and possible inflationary pressures. Potential output estimates also provide a basis for adjusting government budget balances for the effects of the business cycle and are included in analyses of the long-term sustainability of public debt. Moreover, they are also used to gauge the impact of structural reforms.

As potential output is unobservable, it can only be estimated with uncertainty. There are various methods for estimating potential output on the basis of observed data. However, regardless of the method used, such estimates are subject to considerable uncertainty and often revised heavily over time. Therefore, they need to be treated with caution.

Against this backdrop, this article sheds some light on developments in euro area potential output in the post-crisis period. Section 2 discusses the concept of potential output and its measurement. Section 3 examines recent developments in potential output, while Sections 4 and 5 take a closer look at the main driving factors. Section 6 presents the main policy conclusions.

2 The concept of potential output and its measurement

2.1 Definition and determinants

Potential output is typically defined as the highest level of economic activity that can be sustained by means of the available technology and factors of production without creating inflationary pressure.[1] Attempts to exceed this level of production will lead to rising levels of factor utilisation, thereby putting upward pressure on factor costs and ultimately on consumer price inflation. Starting from a neutral position in the economic cycle, a sustainable, non-inflationary increase in output needs to be underpinned by an expansion of potential output.

It is important to distinguish between the level and the rate of growth of potential output. If the level of potential output exceeds actual output, a negative output gap emerges. In such circumstances, the closing of a negative output gap would require actual growth to exceed potential growth for a period of time.

Potential output is usually thought to be determined by supply-side factors, highlighting the importance of sound structural policies for sustainable long-term growth. The supply-side determinants include the state of technology and the available factors of production, most notably labour and capital. At a more fundamental level, the long-term capacity of an economy to produce is shaped by its institutional framework, including the structure of property rights, regulations and the judicial and educational systems. Economies with institutions that facilitate and encourage innovation, factor accumulation and an efficient allocation of resources can be expected to record faster growth in the long run.[2] Indeed, according to Eurosystem estimates, the implementation of best institutional practices in euro area countries could significantly boost their potential growth rates.[3]

The global financial crisis has led to suggestions that demand-side factors might also have very persistent or even permanent impacts on output.[4] According to the “hysteresis” hypothesis, demand shortfalls can perpetuate themselves by adversely affecting the supply potential of the economy and thereby lowering the level of potential output or even its longer-term growth rate. For instance, a demand-led recession may discourage workers from searching for jobs or lead to the erosion of their skills. Firms may refrain from undertaking investment decisions or cut their innovation budgets, which would lower the level of production that can be sustained without stoking (dis-)inflationary pressure. According to this view, countercyclical policies could reduce the risks of hysteresis in times of crisis or reverse its effects ex post, with lasting positive impacts on output.[5] Whether the hysteresis hypothesis is valid is ultimately an empirical question and may also vary across economies and over time.

2.2 Measurement

Since potential output cannot be observed directly, it has to be estimated. Simple statistical methodologies (“univariate filters”) – such as the Hodrick-Prescott (HP) filter – derive potential output by smoothing out fluctuations in actual output. They mechanically split the observed output series into a trend component and a cyclical component. More sophisticated statistical approaches (“multivariate filters”) also use information from other economic indicators, such as inflation, to disentangle the trend from the cycle. Another common approach, which is employed by the European Commission and the Organisation for Economic Co-operation and Development (OECD), is based on a macroeconomic production function, i.e. a simple model of the supply side of the economy relating potential output to the trend components of productivity and the available factor inputs (usually labour and capital).[6] Hybrid methods combine useful elements from both the statistical approach and the production function approach (see Box 1). Other approaches are based on more complex structural economic models.[7] Importantly, all these methods for measuring potential output have their limitations. Therefore, the analysis below will draw on a broad range of estimates based on alternative methodologies.

Regardless of the method used, estimates of potential output are subject to considerable uncertainty. The choice of a specific statistical or economic model always implies judgement and introduces uncertainty. Since models are simplifications of reality, not all information that is possibly relevant for estimating potential output can be processed. In addition, owing to the typically stochastic nature of these models, a degree of uncertainty inherently stems from the characteristics of their shocks. The uncertainty also relates to the parameters of such models which can only be estimated with imprecision. Moreover, the data – both historical and projected – which are used to estimate the models are subject to revisions. Such modifications can result in significant revisions to the estimated path of potential output. Overall, owing to these different types of uncertainty, any point estimate of the output gap has to be treated with a significant degree of caution.

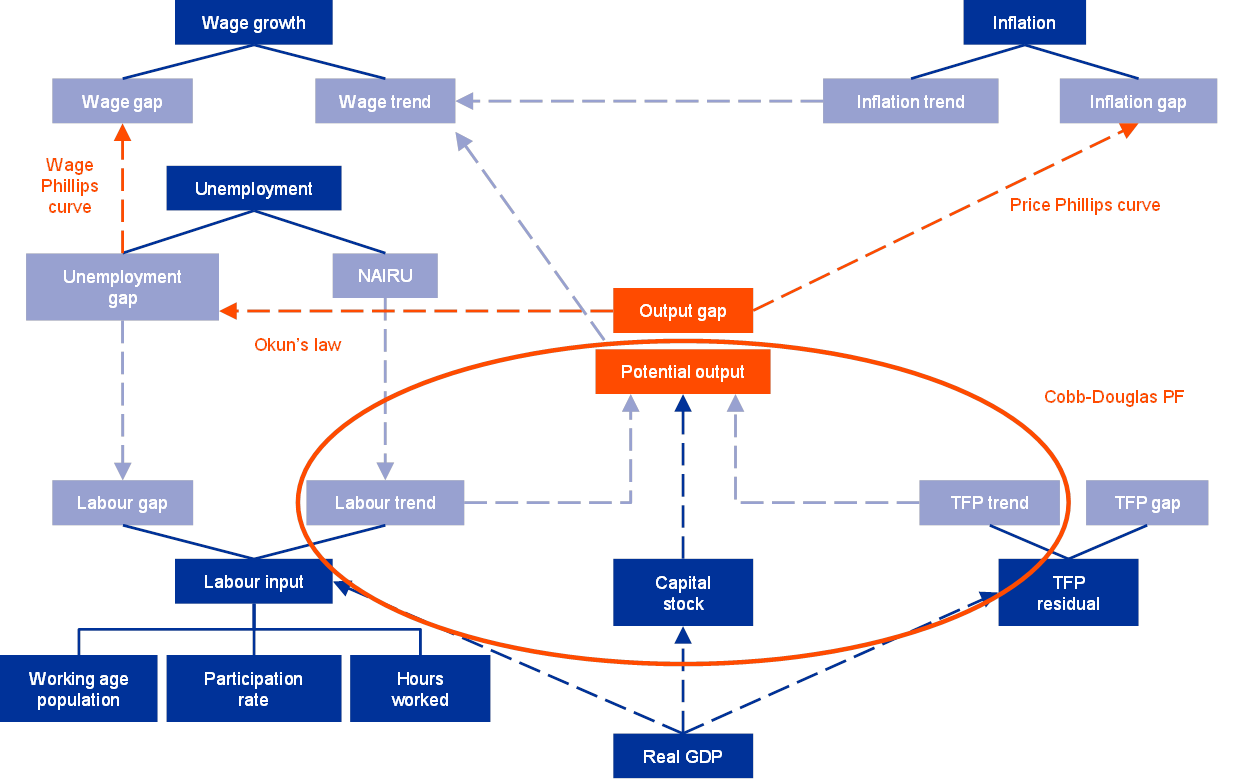

Box 1 An unobserved components model for euro area potential output

The unobserved components model (UCM‑PF) introduced in this box combines a multivariate filter approach with a Cobb-Douglas production function (PF) relating potential output to labour, capital and total factor productivity (TFP). This combination incorporates more economic structure than the traditional production function approach, in which production inputs are typically filtered individually with the help of univariate filters. A possible shortcoming of the latter approach is that the resulting potential output path may closely resemble a potential output path extracted with a univariate filter applied to the output series itself, thus providing little added value. The UCM‑PF approach addresses this issue by estimating the trends of the relevant production inputs jointly in a system of equations in which the trend-cycle decomposition is subject to certain key, albeit reduced-form, economic relationships (see Figure A).

Figure A

Stylised representation of the UCM‑PF

Source: ECB staff.

The underlying model is a backward-looking state-space model that employs the Kalman filter to decompose four key observable variables (real GDP, the unemployment rate, a measure of core inflation and wage inflation) into trend and cyclical components. For this purpose, it relies on several economic relationships, including a Cobb-Douglas production function, a wage and a price Phillips curve and an Okun’s law relationship. A number of additional variables enter the model as exogenously determined observables (e.g. the capital stock and the working age population), while others (such as the labour force participation rate and average hours worked) are endogenously decomposed into cyclical and trend components, with the latter serving as input into the embedded production function. In the model, a closed output gap is consistent with the absence of excessive price or wage pressures, namely inflation being on its long-run trend and wage inflation being consistent with trend inflation and trend productivity growth. In the following sections, model-based uncertainty bands generated by the UCM‑PF will be used to highlight the uncertainty surrounding point estimates of the output gap, potential growth and the trend unemployment rate (or non-accelerating inflation rate of unemployment – NAIRU).

3 Recent developments in potential output

This section analyses recent developments in potential output in the euro area. It focuses on the post-crisis period (2014‑18), but also briefly revisits the crisis years (2008‑13) and the pre-crisis period (1999‑2007).[8] The analysis is based on a broad range of estimates by the European Commission, the International Monetary Fund (IMF) and the OECD, along with estimates based on the model presented in Box 1.

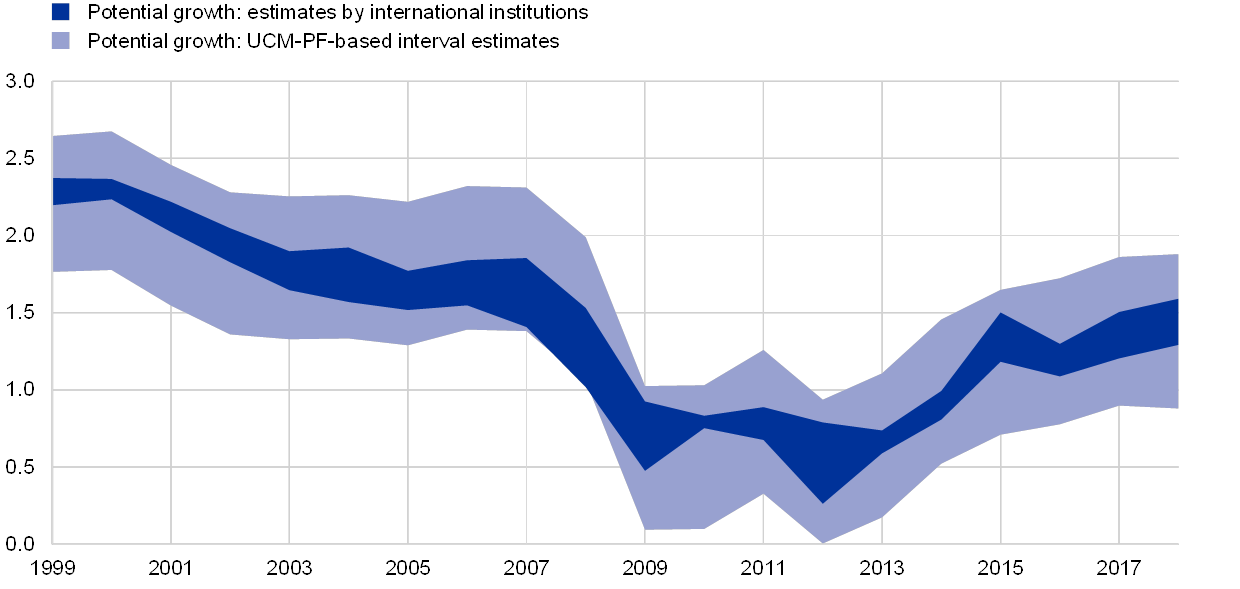

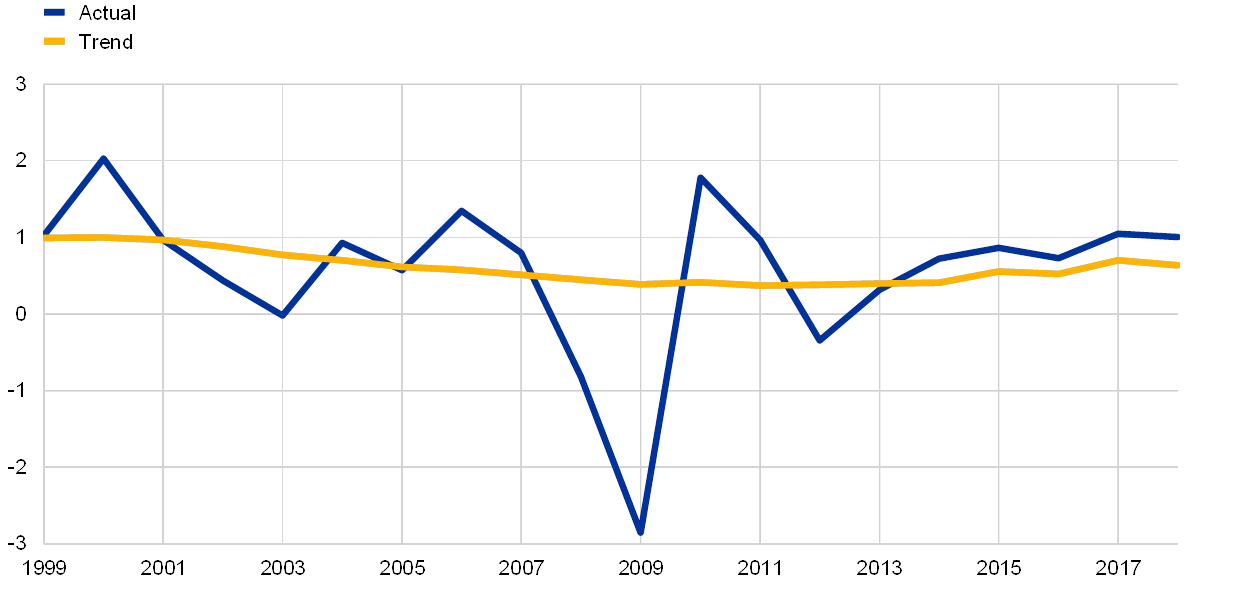

Potential growth in the euro area is estimated to have increased over recent years, although it is still weaker than before the global financial crisis. Prior to the crisis, potential growth was judged to be on a secular downward trend (see Chart 1). Between 1999 and 2007, the estimated rate of potential growth gradually declined from around 2.3% to around 1.7%. The outbreak of the global financial crisis seems to have led to a further decline in potential growth to below 1.0%. However, available estimates indicate that potential output recovered in the post-crisis period, reaching growth rates close to 1.5%. Hence, the latest estimates for euro area potential growth are well above those for the crisis years, albeit still below those for the pre-crisis period. All these estimates are subject to considerable uncertainty, as indicated by the shaded bands in Chart 1. At the same time, they all point to an inverted J-shaped path for euro area potential growth in the period between 1999 and 2017. Moreover, estimates of the euro area aggregate mask significant heterogeneity across individual euro area countries.

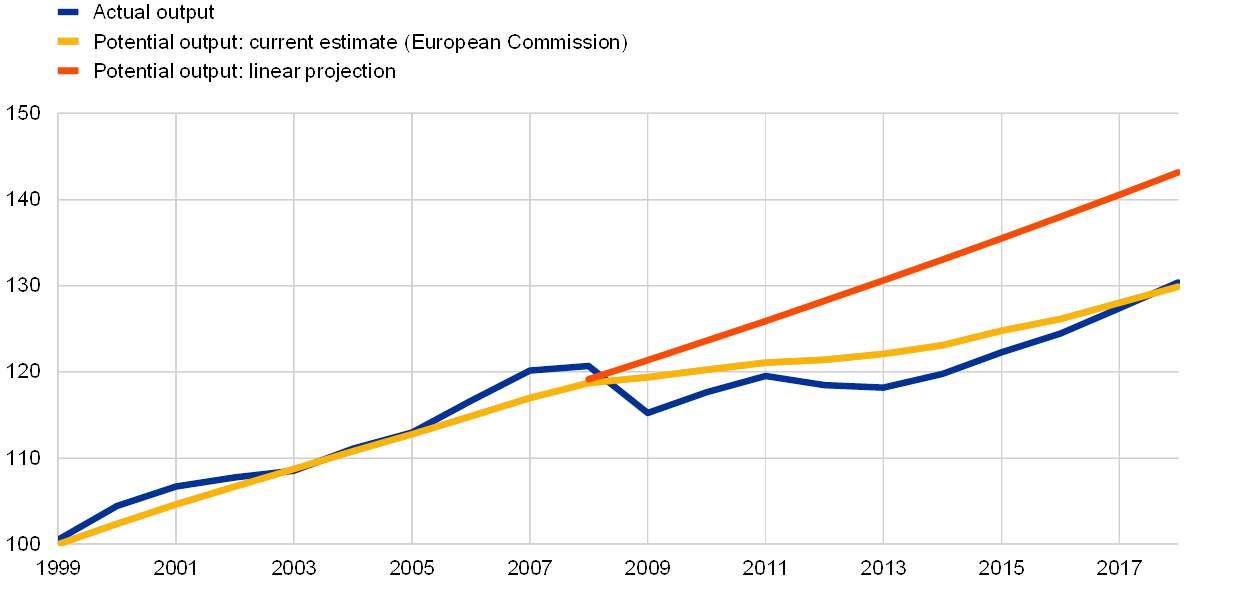

The level of euro area potential output remains well below the path implied by the pre-crisis trends. This can be illustrated with a simple linear projection in which it is assumed that from 2007 onwards potential output steadily increased at the pace recorded in that year. The European Commission’s latest estimate of potential output in 2017 is around 10% below the level implied by the linear projection (see Chart 2). However, caution is warranted when using such gaps as a proxy for the impact of the crisis. Real-time estimates of potential output are often subject to substantial revisions, especially in times of crisis. In fact, the potential output estimates for the euro area were widely revised downwards following the onset of the global financial crisis, before these revisions went into reverse more recently.

Chart 1

Estimates of potential growth

(percentage changes)

Sources: European Commission, IMF, OECD and ECB staff calculations.

Notes: The dark blue area indicates the range of estimates by international institutions, and the light blue area indicates interval estimates based on the UCM‑PF model presented in Box 1 (with an uncertainty band of plus/minus two standard deviations around the point estimate).

Chart 2

Levels of actual and potential output

(index: 1999=100)

Sources: Eurostat, European Commission and ECB staff calculations.

Notes: Actual output is real GDP. Potential output is based on European Commission estimates. The counterfactual scenario assumes that from 2007 onwards potential output steadily increased at the potential growth rate recorded in that year.

The available estimates imply that the euro area economy is currently operating close to its potential. Following the eruption of the global financial crisis, actual output – i.e. real GDP – declined precipitously. At the same time, potential output apparently continued to increase, albeit at a slower pace than before the crisis. As a result, a negative output gap opened up, signalling slack in the euro area economy (see Chart 3).[9] During the economic recovery, GDP growth consistently exceeded available estimates of potential growth. Consequently, the negative output gap gradually declined and now seems to be close to zero. Supply constraints are likely to become increasingly binding going forward, which would be conducive to a gradual strengthening of wage growth and underlying inflation.

Chart 3

Output gap estimates

(percentages of potential output)

Sources: European Commission, IMF, OECD and ECB staff calculations.

Notes: The dark blue area indicates the range of estimates by international institutions, and the light blue area indicates interval estimates based on the UCM‑PF model presented in Box 1 (with an uncertainty band of plus/minus two standard deviations around the point estimate). The UCM‑PF estimates for 2018 only incorporate data up to the second quarter of 2018.

The similarity in estimates by international institutions understates the uncertainty surrounding the current output gap in the euro area. In particular, it has been argued that economic slack might still be larger than indicated by the consensus view of international institutions. This argument is often based on the observation that the underlying potential growth estimates and their revisions tend to co-move with economic activity.[10] This procyclicality could partly be a statistical artefact due to methodological issues, such as the well-known end-point problem of filtering procedures. There may therefore be reason to believe that the degree of economic slack in the euro area over recent years has been larger than indicated by the estimates of international institutions.[11] This could also help explain the relatively muted dynamics of underlying inflation over this period. However, the procyclicality of potential growth and output gap estimates may also stem from hysteresis, the downward rigidity of prices and wages, and other effects that pull down potential growth during economic downturns and gradually wane during upturns (see Section 2.1).

4 Dissecting recent developments in potential output

In an accounting sense, potential output is determined by the trend components of the factors of production – capital and labour – and total factor productivity (TFP). A macroeconomic production function can be used to decompose potential growth into the contributions from labour, capital and TFP (see Section 2.2). TFP captures the overall efficiency of the use of the factors of production and its evolution is therefore often seen as a rough indication of technological progress. In practice, TFP is not directly observable and is typically calculated as a residual term in a growth accounting exercise. Thus it cannot be considered a pure measure of productivity.

Both the decline in potential growth during the crisis and its subsequent recovery were largely driven by the contributions of capital and labour. Both contributions declined during the crisis, before recovering in the post-crisis period (see Chart 4). The latest estimates for 2017 indicate that the contributions of labour and TFP to potential growth are broadly in line with those in 2007. However, the contribution of capital is still weaker than before the crisis, explaining why potential growth has not yet fully recovered. The downward trend in potential growth in the pre-crisis period mainly reflected a secular decline in TFP growth.[12]

Chart 4

Decomposition of potential growth

(percentage points)

Source: European Commission.

While the inverted J-shaped path of potential growth found in the euro area has also been observed in other major advanced economies, there are notable cross-country differences in the underlying driving forces. Box 2 illustrates this for the United States and Japan. Moreover, from a long-term perspective, potential growth in the euro area has fallen short of that in other major advanced economies, in particular the United States.

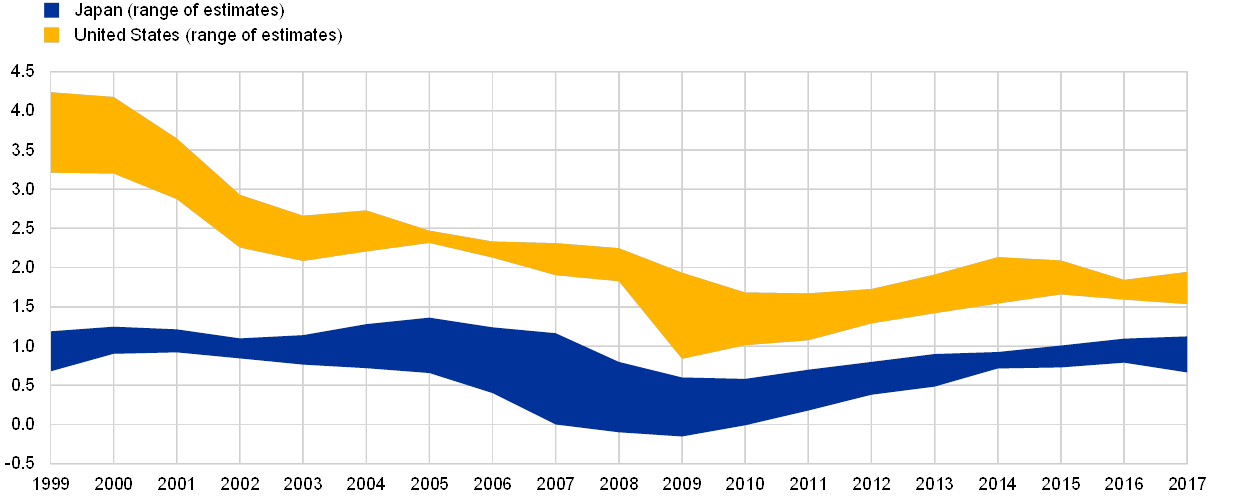

Box 2 Potential output developments in the United States and Japan

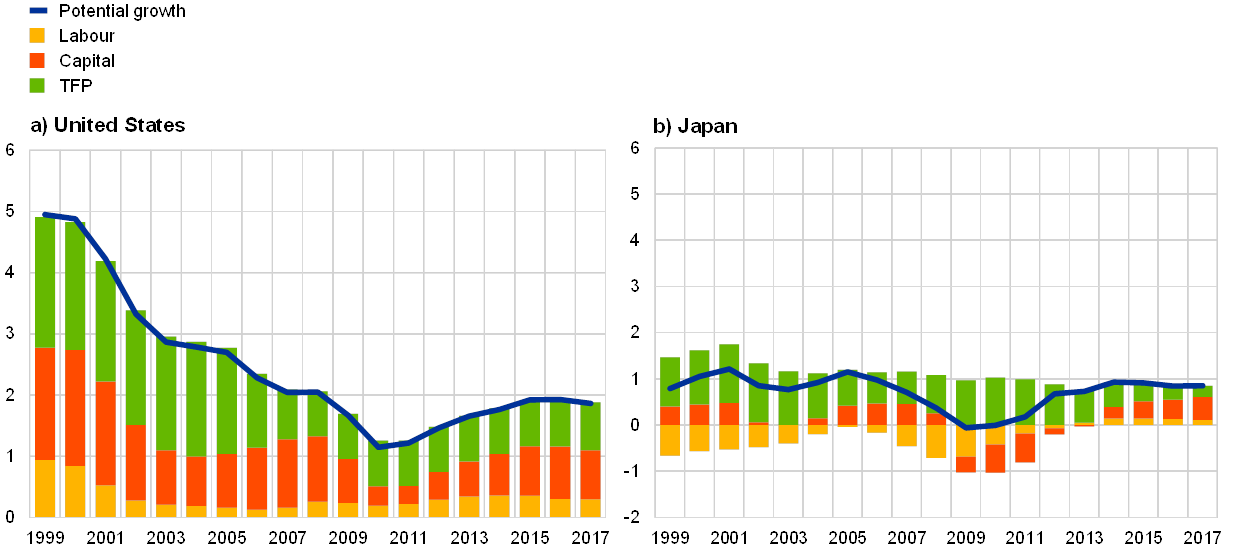

Similarly to developments in the euro area, estimated potential output in the United States and Japan has recovered since 2013 along with economic activity. At the same time, the current pace of potential growth in the US economy remains well below the growth rates recorded prior to the global financial crisis, while it is broadly comparable to pre-crisis rates in the case of Japan. According to a broad range of estimates, including from national sources and international institutions, potential growth is currently estimated at close to 2% in the United States and around 1% in Japan (see Chart A).

Chart A

Estimates of potential growth in the United States and Japan

(annual percentage changes)

Sources: Congressional Budget Office, Bank of Japan, Cabinet Office of the Government of Japan, IMF, OECD and ECB staff calculations.

An increasing stock of capital, reflecting strengthening investment activity in this period, was a key contributory factor in the recovery in potential output in both countries. While investment activity plummeted in the aftermath of the global financial crisis, the ensuing demand recovery – supported by economic policies – helped stimulate investment spending amid gradually declining spare capacities (see Chart B).

By contrast, the contribution of the labour component to potential growth in the United States and Japan differed, owing to secular trends observed in these two countries. In the United States, the labour contribution has remained positive and broadly unchanged since the global financial crisis, as slower growth in the potential labour force was counteracted by a gradual decline in the trend unemployment rate. The latter could reflect the gradual waning of hysteresis effects and also shifts in the composition of the workforce, which in turn may reflect, for example, the fact that older and more educated workers tend to have lower unemployment rates. In Japan, the contribution of labour to potential growth turned positive in 2013, following a prolonged period of strong negative readings. Demographic developments, leading to a shrinking workforce, are the main factor that led to labour having acted as a drag on potential output. Recent measures taken by the Japanese government to encourage the participation of women in the labour market, the increasing willingness of retired workers to remain active amid rising longevity, and more flexible working contracts offered by Japanese firms have all helped to increase labour force participation in the Japanese economy, thereby limiting the negative impact of the shrinking workforce amid very tight labour market conditions.

Chart B

Decomposition of potential growth in the United States and Japan

(annual percentage changes, percentage points)

Sources: Congressional Budget Office, Bank of Japan and ECB staff calculations.

Notes: For the United States, “potential growth” refers to the non-farm business sector and “labour” refers to the contribution of hours worked, while “capital” refers to the contribution of capital services. For Japan, “labour” refers to the sum of contributions of the number of people employed and hours worked.

TFP growth contributed positively to potential output in both countries, although it has shown diverging patterns over the recent past. In the United States, the contribution from TFP growth has remained broadly stable during the post-crisis period. In Japan, the estimated positive contribution of TFP growth has roughly halved over the same period, which can be attributed to an ageing capital stock and delays in the introduction of new technologies.[13] However, the increasing implementation of technological advances, especially in sectors currently facing acute labour shortages, could strengthen underlying productivity growth over the longer term.[14]

Looking ahead, demographic developments present both countries with a challenge that needs to be resolved to avoid weakening their potential growth. In Japan, progress in implementing the government’s growth strategy, including regulatory and institutional reforms, further increases in labour force participation, and continued efforts by firms to increase productivity are expected to tackle this and contribute to gradually accelerating potential growth over the next few years.[15] In the United States, the recent changes in income taxes could encourage more people to enter the labour force, thereby limiting the negative impact on potential growth stemming from population ageing.[16] Also, the reduction in corporate income tax could boost investment and thereby contribute to higher potential output, whereas recent policies aimed at reducing immigration could have an opposite effect by further weakening the growth of the labour force.

5 A closer look at the factors driving potential output

This section takes a closer look at some of the underlying factors driving recent developments in potential output in the euro area. In particular, it seeks to answer the question of why the contributions of labour and TFP to potential growth have broadly returned to their pre-crisis levels, while the capital contribution remains subdued. The section concludes by looking at the longer-term outlook for potential growth.

5.1 Labour

The contribution of labour to potential growth can be traced back to trends in the labour force, the unemployment rate and hours worked per employee. The labour force includes all those in work or seeking work. Changes in the labour force, in turn, can be decomposed into changes in the working age population (15‑74 years of age) and the labour force participation rate (i.e. the percentage of the working age population participating in the labour force).

The enlargement of the working age population on account of immigration has supported potential growth over recent years. Following a contraction between 2009 and 2015, the working age population has been increasing over recent years. These developments reflect two countervailing forces (see Chart 5). On the one hand, “natural” population growth has been negative for some time now, since the “baby-boomer” generation is reaching retirement age and fertility rates are low. On the other hand, there has been a net inflow of people of working age, in particular from other EU Member States.[17]

Chart 5

Cumulative changes in the working age population of the euro area since the first quarter of 2007 by citizenship

(thousands)

Source: Eurostat (European Union Labour Force Survey).

Notes: “Euro area citizens” refers to all members of the working age population aged 15 to 74 holding citizenship of an EU Member State whose currency is the euro. The data have been adjusted for structural breaks, in particular for Germany (first quarter of 2010) and France (first quarter of 2014). The chart is based on four-quarter averages.

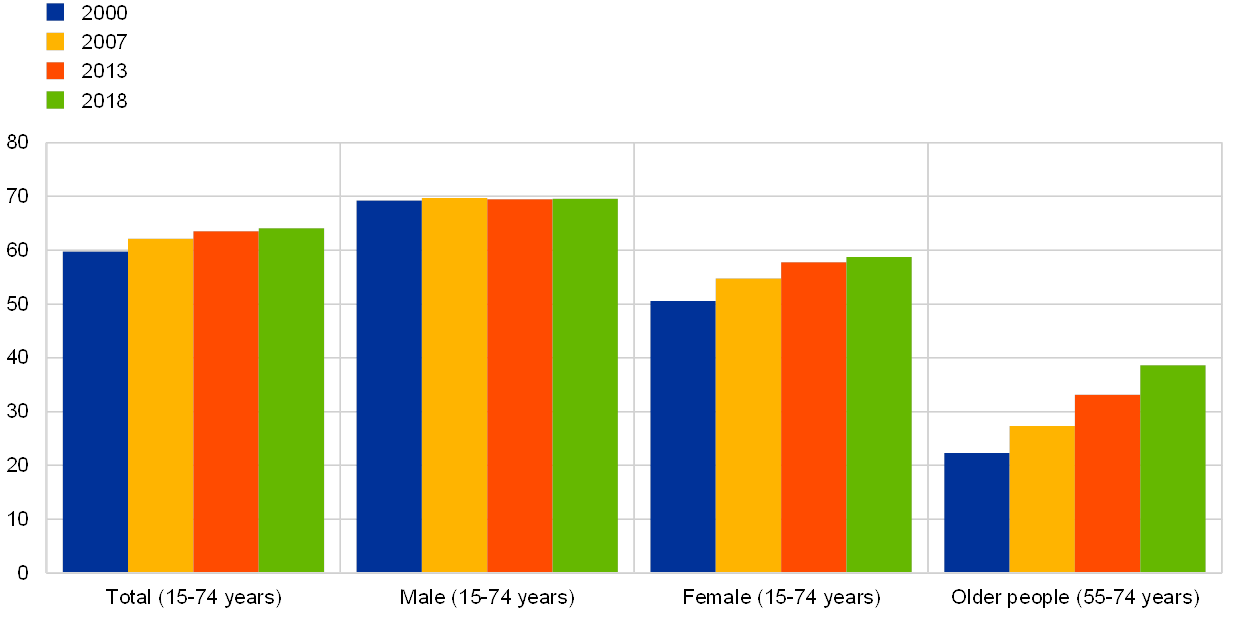

Labour force participation has continued to increase during the recovery, underpinned by increased participation of the older generations and women.[18] While the euro area labour force is ageing, more people are remaining economically active later in life. In line with this longer-term trend, the participation rate of those aged 55 to 74 has continued to increase during the recovery. This reflects increases in the pension age in many euro area countries, as well as other factors, most notably rising education levels. In addition, the labour force participation of women has continued to increase, which is also partly due to rising education levels.[19] All these structural changes have contributed to a steady increase in the participation rate over recent years (see Chart 6). Coupled with a growing working age population, this trend has led to an expansion of the labour force during the ongoing economic recovery. However, the rate of growth of the labour force still remains below that recorded in the pre-crisis period.

Chart 6

Labour force participation rate by gender and age

(percentages)

Source: Eurostat.

Notes: The total participation rate is defined as the labour force as a percentage of the working age population. The latter comprises those aged between 15 and 74. The participation rates for individual groups (i.e. women, men and older people) only relate to the relevant parts of the labour force and the population.

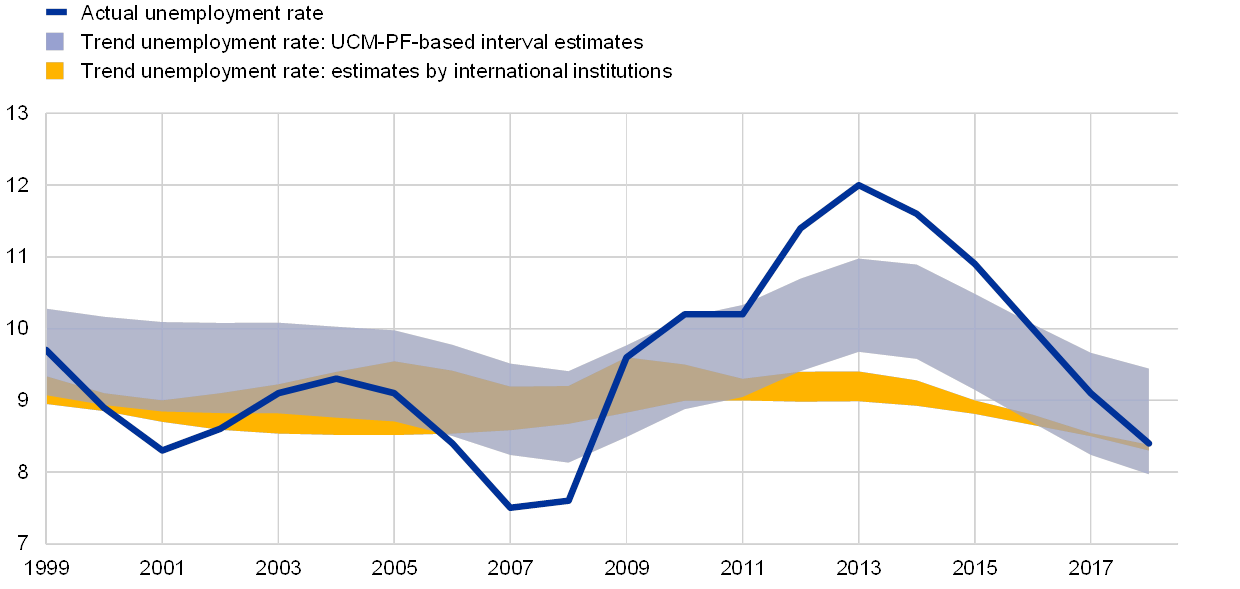

A decline in the trend unemployment rate is estimated to be another important driver of the post-crisis recovery in potential growth. The trend unemployment rate broadly corresponds to the unemployment rate that is consistent with non-accelerating wage (or price) inflation.[20] Available estimates overall suggest that the trend unemployment rate in the euro area increased in the crisis period, partly due to hysteresis effects, before declining to around 8.0‑9.5% more recently (see Chart 7). To some extent, these developments reflect transitory factors. Since wages tend to adjust slowly to shocks, the macroeconomic adjustment partly operates through persistent changes in the unemployment rate. However, the post-crisis decline in the estimated trend unemployment rate is also likely to be driven by structural factors, most notably the labour market reforms undertaken in some euro area countries.

Chart 7

Unemployment rate and estimates of the trend unemployment rate

(percentages)

Sources: Eurostat, European Commission, IMF, OECD and ECB staff calculations.

Notes: The yellow area indicates the range of estimates by international institutions, and the light blue area indicates interval estimates based on the UCM‑PF model presented in Box 1 (with an uncertainty band of plus/minus two standard deviations around the point estimate). The UCM‑PF estimates for 2018 only incorporate data up to the second quarter of 2018.

Hours worked per employee have continued to decline over recent years, although there are some signs of stabilisation.[21] The longer-term downward trend in average hours worked per employee mainly reflects secular changes in the composition of euro area employment. Most importantly, the shares of part-time workers and the services sector (where hours worked are typically lower than in other sectors) in overall employment have increased over the past decade.

5.2 Capital

The capital stock is another essential determinant of potential output, but data are not easy to obtain. The gross capital stock is the physical capital available in the private and public sectors of the economy for production processes.[22] The true potential capital stock is not directly measurable but can be calculated using the “perpetual inventory” method. The current net capital stock is then derived from the past capital stock, subtracting depreciation and adding new investment. Such capital stock data come with a long publication lag.[23] The real capital stock also depends on price trends of capital goods. These trends could be very different from those of intermediate and consumer goods. Over the past two decades, the investment deflator – and in particular the quality-adjusted prices of information and communications technology (ICT) goods – has been less dynamic than the overall value added deflator, which has supported the capital-output ratio in real terms.[24]

The rising share of intangible investment increases capital consumption and poses challenges to measuring the capital stock. The capital stock in the construction sector generally depreciates very slowly, while the business sector capital stock, particularly intangibles, depreciates much faster.[25] Aggregate depreciation rates are likely to increase gradually as countries’ income levels rise, assuming that the share of assets with shorter lifespans (such as intangible assets) grows in economically more advanced countries. As a result, the amount of investment required to offset the consumption of capital and to maintain the capital stock at a constant level increases. At the same time, it is possible that the size of the capital stock remains underestimated owing to insufficient incorporation of intangible investment[26] in the national accounts (see also the box entitled “Investment in intangibles in the euro area” in this issue of the Economic Bulletin).[27] Intangible investment has long been considered largely as intermediate consumption – as opposed to investment – on the balance sheets of firms, reflecting the fact that such investment was thought to exclusively benefit firms themselves. Available estimates suggest that GDP (and gross saving and investment rates) in Europe would be 5 to 10 percentage points higher if all intangibles were classified as investment.[28]

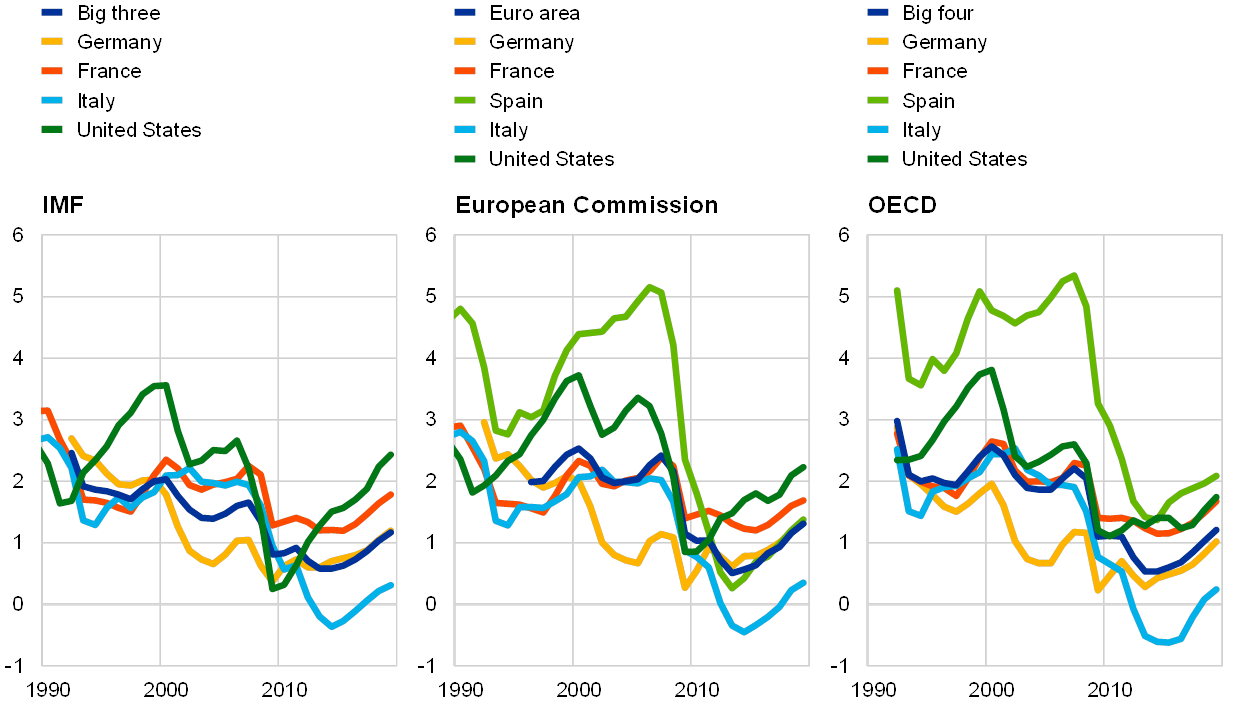

The cyclical recovery in overall investment since the crisis has given some positive impetus to the capital stock in the euro area, although its contribution to the capital stock has been lower than in the pre-crisis period. Increasing demand, low financing costs and better access to finance as a result of the ECB’s accommodative monetary policy have supported the recovery in investment.[29] As a result, capital stock growth rates have accelerated in the euro area in the period since the crisis (see Chart 8). However, lower than pre-crisis growth rates of investment[30] have weighed on capital stock contributions to potential growth in the recovery period (see Chart 4). There are a number of factors behind the lower growth rates. First, it took time to unwind excess capacity accumulated during the crisis in the construction sector – particularly in housing, but also in commercial and industrial construction – which resulted in underutilised capital and excess capacity. Second, recent years have still been characterised by persistently high uncertainty, slowing growth expectations related partly to population ageing, and remaining deleveraging needs, both in the private and public sectors. Third, in the early phase of the recovery the average scrapping rate might have been higher due to crisis-related company liquidations. Also, in this period public investment was subdued owing to fiscal constraints in some countries. Public investment has been shown to have considerable spillover effects on private investment.[31]

Chart 8

Growth in the real capital stock in selected economies

(annual percentage changes; total capital stock)

Sources: European Commission (AMECO), IMF and OECD.

Notes: The “big three” of the euro area are Germany, France and Italy, while the “big four” also includes Spain. The growth rates of the capital stocks include projections until 2019. Data for Spain from the IMF are missing.

5.3 Total factor productivity

In the decade leading up to the global financial crisis, TFP growth was on a downward trend in the euro area and in other advanced economies. Between 1999 and 2007, trend TFP growth gradually slowed from 1.0% to 0.5%, according to European Commission estimates (see Chart 9). Several explanations have been proposed for this deceleration, some of which are complementary.[32] Mismeasurement problems, for instance with regard to intangible investments, may have led to an underestimation of TFP growth. More fundamentally, recent innovations might have been less pervasive than earlier technological advances, such as the railways and electricity. Moreover, there is evidence that it takes longer for technological innovations by pioneering firms to be incorporated into the production processes of other firms.

Chart 9

Total factor productivity growth

(percentage changes)

Source: European Commission.

Note: The trend is based on estimates by the European Commission.

The global financial crisis exacerbated the decline in TFP growth. In fact, TFP growth is even estimated to have turned negative during the crisis, albeit largely driven by its cyclical component. Firm-level evidence indicates that bank forbearance and inadequate insolvency regimes locked capital into firms with low levels of productivity, weakening the cleansing effects typically associated with recessions.[33] Following the unwinding of macroeconomic imbalances in euro area countries, structural rigidities may have hampered the necessary reallocation of resources towards more productive sectors and firms. Moreover, protracted private sector balance sheet repair has weakened investment, thereby potentially limiting technological innovation.

TFP growth has increased during the ongoing economic recovery, broadly returning to its pre-crisis rates. The adverse effects of the crisis on TFP growth, for instance through disruptions in financial intermediation, cuts in research and development budgets and subdued spending on public infrastructure, have started to wane. There is also evidence that the crisis has ultimately led to a reallocation of resources towards more productive firms (e.g. through the elimination of unviable businesses). Moreover, it may simply take some time for innovations in the field of digitalisation to be widely adopted throughout the economy. Sustained improvements in educational attainment also continue to support TFP growth.

5.4 Longer-term outlook

Euro area potential growth will remain broadly stable over the coming years, according to the projections by international institutions. On average, the European Commission, the IMF and the OECD envisage potential growth of 1.4% in 2018 and 1.5% in 2019 (see Table 1). The projections are below those for actual GDP growth, implying that supply constraints will become more binding.

Table 1

Projections for actual and potential growth by international institutions

(percentage changes)

Sources: European Commission, IMF and OECD.

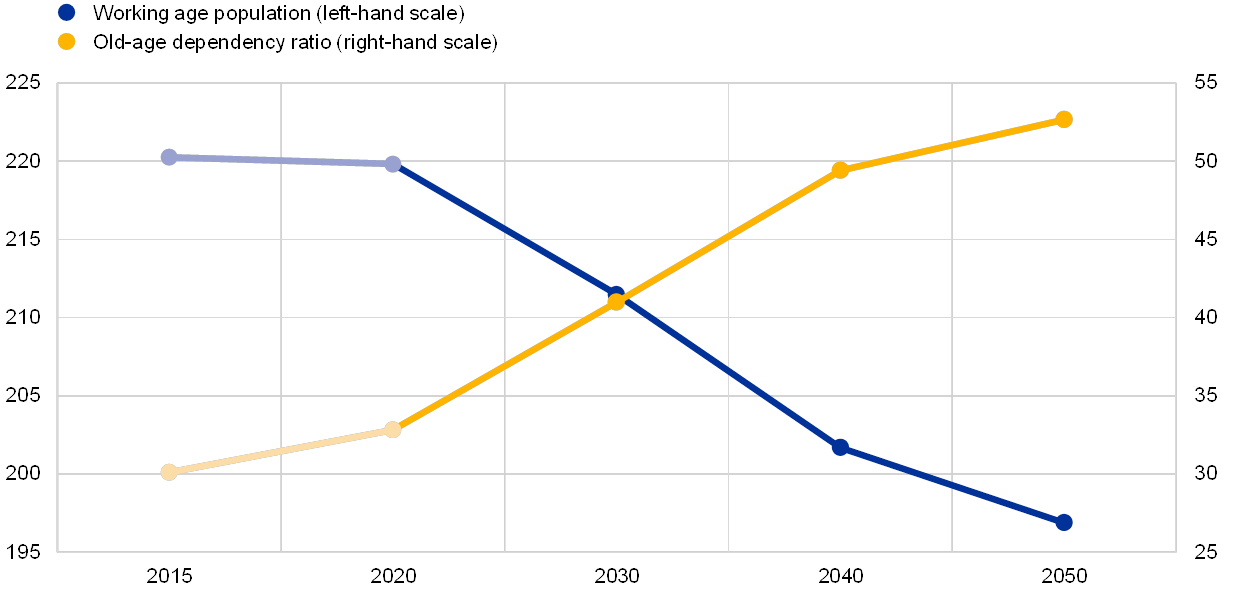

While the longer-term outlook for potential growth is more uncertain, population ageing looks set to exert increasing downward pressure.[34] According to projections by Eurostat, the euro area’s old-age dependency ratio (i.e. the number of people aged 65 or over as a percentage of the working age population) will increase from around 30% at present to around 50% by 2050 and the working age population will decline by around 23 million over the same period (see Chart 10). This forecast already takes into account net immigration of around 800,000 persons per year. The expected decline in the working age population could be partly offset by further increases in the overall participation rate on the back of previous pension reforms and rising education levels. However, on the basis of these projections, the euro area labour force looks set to decline over the coming decades, exerting downward pressure on potential growth.

Chart 10

Working age population and old-age dependency ratio (Eurostat projections)

(left-hand scale: millions; right-hand scale: percentages)

Source: Eurostat (population projections 2015).

The impact of population ageing on potential growth could be partly offset by other factors. In particular, automation and digitalisation could support TFP growth (see Box 3). However, when and to what extent this will happen is highly uncertain.

With regard to the capital stock, it could be expected to continue growing and to contribute positively to potential growth. International institutions also expect capital stock growth to accelerate further in the next few years. The reasons for continued capital accumulation include sustained cyclical demand, near-full capacity utilisation in the capital goods-producing sector and a continued need to replace and upgrade capital in order to face the challenges posed by globalisation and the digital economy. In the longer term, expectations of further advances in technology – and the resulting changing composition of the capital stock – point to an accelerating need for capital accumulation to keep up with rising overall depreciation rates. Recent research has also found that the capital stock of intangible assets adjusts more slowly to fluctuations in the economy than tangible investment,[35] given the irreversible nature of intangible investment. This could result in a capital stock that is becoming less sensitive to the business cycle.

Box 3 The role of digitalisation in shaping developments in potential output and the output gap in the euro area

Digitalisation may be viewed as a supply shock affecting key macroeconomic aggregates for the euro area, including potential output and the output gap, largely via possible competition, productivity and employment effects.[36] One aspect of this is the digitalisation of production and supply chains, involving automation, robotisation and artificial intelligence. This tends to change relative prices and the allocation of work across factors of production, for instance between labour and capital or between routine and non-routine jobs, and thereby affect productivity. Another aspect of digitalisation is digital and mobile communication and connectivity, encompassing the internet, social media, cloud computing and big data analysis. These have an impact on competition by altering relative prices and market shares between, for instance, digital and non-digital firms or small and large firms (the “winner takes all” phenomenon). The third aspect of digitalisation is new goods and services, both information technology (IT)-related and non-IT-related, which may lead to changes in prices and/or consumer preferences.

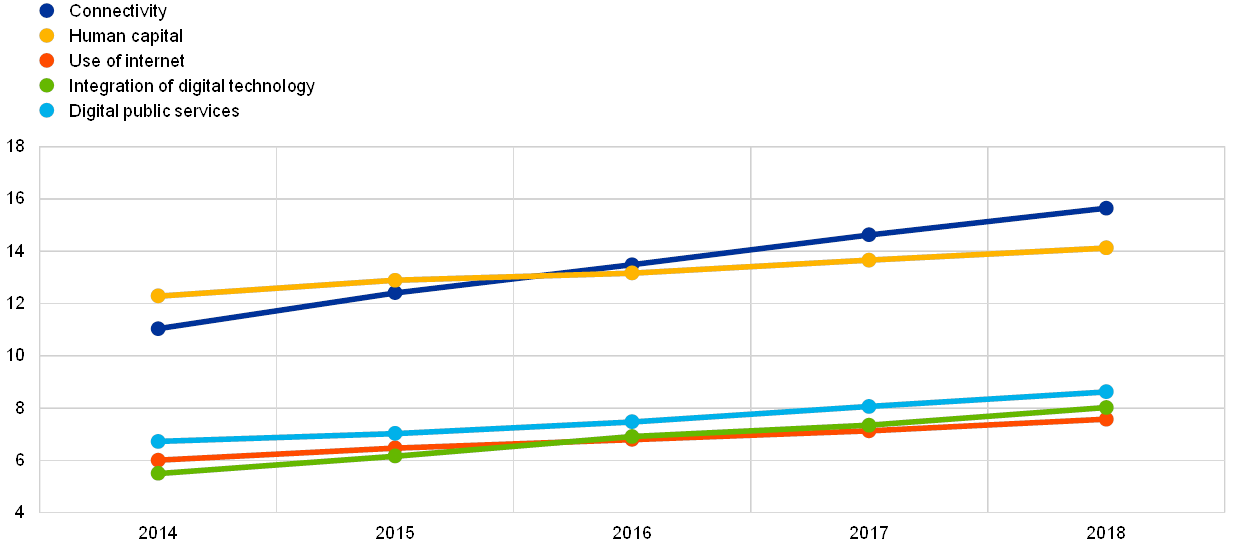

While some aspects of digitalisation are more advanced than others, it seems to be progressing relatively steadily for the EU as a whole. This can be seen, for example, from the European Commission’s Digital Economy and Society Index (DESI), as displayed in Chart A for the EU for the sample between 2014 and 2018. It is important to note, however, that many of the major milestones of digitalisation occurred before the sample covered in Chart A, such as early research on artificial intelligence in the 1950s, the first computer networks in the 1960s, the first email in the 1970s, the first driverless car in the 1980s, the world-wide web, the internet of things and search engines in the 1990s, and social media in the 2000s. As a result, digitalisation is perhaps best described as a succession of supply shocks occurring, and impacting on the economy, over time.

Chart A

Digitalisation in the EU28 from 2014 to 2018

(index: between 0 and 25 for connectivity and human capital; between 0 and 20 for integration of digital technology; between 0 and 15 for use of internet and digital public services)

Source: European Commission.

Digitalisation may affect all the contributions to potential output – namely labour, capital and TFP. Digital production and supply chains, for example, may raise TFP, because of the greater efficiency (in terms of time and/or quality) of digitally-enhanced or digitally-supported (e.g. just-in-time) production technology. Digital communication and connectivity may also support TFP, by enabling the faster collection and evaluation of data. At the same time, there have been suggestions that some digital and mobile communication applications could act as a distraction from productive activity. While it is unclear how the TFP contribution has been or is going to be affected by digital technology, it seems likely that the overall effect would be supportive of potential growth. It is also likely that the TFP contribution of digital technologies has been supportive of potential growth in the past, although it is noteworthy that this has not been sufficient to offset the decline in trend TFP growth.

While digitalisation may support potential output via the TFP contribution, the effects via the contributions from labour and capital are more uncertain. Digital production and supply chains may lead to an increased need for labour for non-repetitive, non-routine tasks, digital skills and professions, or other skills and professions for the digital work environment (such as openness to change and/or adaptability to new technologies). At the same time, however, they may entail a reduced requirement for lower skilled labour for more routine tasks and a corresponding shift to more (IT) capital. Although these effects might be expected to be broadly offsetting, it is also conceivable that the labour contribution to potential output may be pushed up or pulled down somewhat in ways that are difficult to predict. The same might be true of the capital contribution. While substantial investments in digital technology might be expected, the effect on the overall physical capital stock might be limited, particularly if the new technologies increase the intensity with which capital assets can be used.

How the effects of digitalisation on potential output might unfold depends on a number of factors, and is therefore difficult to predict. It is noticeable, however, that some economies are more advanced than others in certain aspects of digitalisation (see Chart B). Going forward, economies with an environment conducive to research and innovation are likely to see faster adoption and implementation of digital technologies and thus also a faster impact on potential output.

Chart B

Digitalisation in the EU28 in 2018

(index: between 0 and 25 for connectivity and human capital; between 0 and 20 for integration of digital technology; between 0 and 15 for use of internet and digital public services)

Source: European Commission.

Summing up, digitalisation is likely to affect potential output and the output gap, but the dynamics of those effects are difficult to predict. While the effects of digitalisation on the labour and capital contributions to potential output are particularly uncertain, the effects of digitalisation on the TFP contribution are more likely to be supportive of potential output.

Conclusions

Available estimates indicate that euro area potential growth has increased over recent years, although it remains weaker than before the global financial crisis. Following a significant slowdown during the crisis, potential growth is estimated to have recovered since the start of the ongoing economic recovery. Over recent years, potential growth has been underpinned by an expansion of the labour force, a decline in trend unemployment and stronger productivity gains. While capital formation has also accelerated over recent years, it remains weaker than before the crisis.

Supply constraints are expected to become increasingly binding going forward, which would be conducive to a gradual strengthening of wage growth and underlying inflation. During the ongoing economic recovery, real GDP growth has consistently exceeded available estimates of potential growth. This has led to a gradual shrinking of the output gap that opened up during the crisis. The economy now seems to be operating close to its potential. It should be noted, however, that estimates of potential output and the output gap are fraught with uncertainty.

Given the imminent challenges arising from population ageing, well-designed structural policies with a focus on enhancing productivity are essential to boost potential growth.[37] Population ageing is expected to exert downward pressure on euro area potential growth over the coming decades. This could be offset at least partly by sound structural policies for labour, product and services markets that can be expected to raise the labour or TFP contribution to potential growth. To exploit the full potential of digitalisation, the euro area economy needs improvements in the quality of the digital infrastructure and the availability of digital skills. The deepening of the Single Market and competition-enhancing product market reforms, in particular in the services sector, would also foster productivity growth. In addition, the cutting of red tape would facilitate firm entry and exit and the efficient reallocation of resources across firms. Labour force and employment growth could be supported by policies that help the long-term unemployed, migrants and other groups whose participation rates remain low to enter or return to the labour market, or to find jobs that better match their skills.

- Alternative concepts whereby potential output is defined as the level of output that could be obtained in the absence of price-setting frictions or market inefficiencies (such as imperfect competition) also appear in the literature. However, the corresponding potential output series are highly dependent on the underlying model and the frictions assumed therein. See Vetlov, I., Hlédik, T., Jonsson, M., Kucsera, H. and Pisani, M., “Potential output in DSGE models”, Working Paper Series, No 1351, ECB, June 2011.

- See Acemoglu, D., Johnson, S. and Robinson, J., “Institutions as a Fundamental Cause of Long-Run Growth”, in Aghion, P. and Durlauf, S. (eds.), Handbook of Economic Growth, Vol. 1, Part A, Elsevier, 2005, pp. 385‑472.

- See Masuch, K., Anderton, R., Setzer, R. and Benalal, N. (eds.), “Structural policies in the euro area”, Occasional Paper Series, No 210, ECB, June 2018.

- See Ball, L., “Long-term damage from the Great Recession in OECD countries”, European Journal of Economics and Economic Policies: Intervention, Vol. 11, No 2, 2014, pp. 149‑160, and Blanchard, O., “Should We Reject the Natural Rate Hypothesis?”, Working Papers, No 17‑14, Peterson Institute for International Economics, November 2017.

- See Yellen, J.L., “Macroeconomic Research After the Crisis”, speech at the 60th annual economic conference sponsored by the Federal Reserve Bank of Boston, Boston, October 2016.

- The potential output estimates by the IMF are not based on a uniform method and may incorporate judgement. For the euro area countries, the production function approach is usually applied.

- See Coenen, G., Smets, F. and Vetlov, I., “Estimation of the Euro Area Output Gap Using the NAWM”, Working Paper Series, No 5, Lietuvos bankas, 2009.

- For the crisis period, see Anderton et al., “Potential output from a euro area perspective”, Occasional Paper Series, No 156, ECB, November 2014, and the articles entitled “Potential output, economic slack and the link to nominal developments since the start of the crisis”, Monthly Bulletin, ECB, November 2013, and “Trends in potential output”, Monthly Bulletin, ECB, January 2011.

- See also the box entitled “Measures of slack in the euro area”, Economic Bulletin, Issue 3, ECB, 2018.

- See Coibion, O., Gorodnichenko, Y. and Ulate, M., “The Cyclical Sensitivity in Estimates of Potential Output”, NBER Working Papers, No 23580, National Bureau of Economic Research, 2017.

- See Jarocinski, M. and Lenza, M., “An Inflation-Predicting Measure of the Output Gap in the Euro Area”, Journal of Money, Credit and Banking, Vol. 50, No 6, September 2018, pp. 1189‑1224.

- See the article entitled “The slowdown in euro area productivity in a global context”, Economic Bulletin, Issue 3, ECB, 2017.

- See Sakurai, M. and Kataoka, M., “Hysteresis and Sluggish Growth in Wages and Prices: The Case Study of Japan”, paper presented at the 30th Villa Mondragone International Economic Seminar, Rome, June 2018.

- See Amamiya, M., “Japan’s Economy and Monetary Policy”, speech at a meeting with business leaders in Kyoto, Bank of Japan, August 2018.

- See “Outlook for Economic Activity and Prices”, Bank of Japan, July 2018.

- See The Budget and Economic Outlook: 2018 to 2028, Congressional Budget Office, April 2018.

- It should be noted that the decomposition of changes in the working age population by citizenship is only an imperfect proxy of migration flows.

- See the article entitled “Labour supply and employment growth”, Economic Bulletin, Issue 1, ECB, 2018, and the box entitled “Recent developments in euro area labour supply”, Economic Bulletin, Issue 6, ECB, 2017.

- See Thévenon, O., “Drivers of Female Labour Force Participation in the OECD”, OECD Social, Employment and Migration Working Papers, No 145, OECD, 2013.

- An alternative concept is the “structural unemployment rate”, which is affected only by structural factors, such as institutions and technology – see Havik et al., “The Production Function Methodology for Calculating Potential Growth Rates & Output Gaps”, European Economy – Economic Papers, No 535, European Commission, November 2014, Box 1.

- See the box entitled “Factors behind developments in average hours worked per person employed since 2008”, Economic Bulletin, Issue 6, ECB, 2016.

- See Anderton et al. (2014), op. cit.

- Official capital stock data (based on non-financial asset balance sheets) that are in line with the ESA 2010 Transmission Programme are available for the total economy and by asset (at annual frequency) for most EU countries, but not for the euro area as a whole, with a publication lag of about 24 months.

- For evidence on Germany, see the article entitled “Investment in the euro area”, Monthly Report, Deutsche Bundesbank, January 2016, pp. 31‑49.

- Depreciation rates range from about 1% per year for the stock of residential structures to around 20% for research and development, and around 30% for software, according to data from the EU KLEMS database.

- See Haskel, J. and Westlake, S., Capitalism without Capital: The Rise of the Intangible Economy, Princeton University Press, 2017.

- However, since its revision in 2014, the European System of Accounts (ESA 2010) has distinguished between construction investment (about 50% of euro area total investment), machinery and equipment (about 30%) and investment in intellectual property products (about 20%).

- See Corrado, C., Haskel, J., Jona-Lasinio, C. and Iommi, M., “Intangible Capital and Growth in Advanced Economies: Measurement Methods and Comparative Results”, IZA Discussion Paper, No 6733, July 2012. See also http://www.intan-invest.net/.

- See the article entitled “Business investment developments in the euro area since the crisis”, Economic Bulletin, Issue 7, ECB, 2016.

- See “Investment in the EU Member States: An Analysis of Drivers and Barriers”, European Economy – Institutional Papers, No 062, European Commission, October 2017.

- See “Business investment in EU countries”, Occasional Paper Series, No 215, ECB, October 2018.

- See the article entitled “The slowdown in euro area productivity in a global context”, Economic Bulletin, Issue 3, ECB, 2017.

- See Andrews, D. and Petroulakis, F., “Breaking the Shackles: Zombie Firms, Weak Banks and Depressed Restructuring in Europe”, Economics Department Working Papers, No 1433, OECD, 2017.

- See the article entitled “The economic impact of population ageing and pension reforms”, Economic Bulletin, Issue 2, ECB, 2018.

- See Peters, R. and Taylor, L., “Intangible capital and the investment-q relation”, Journal of Financial Economics, Vol. 123(2), February 2017, pp. 251‑272.

- Information on the findings of an ad hoc ECB survey of leading euro area companies on the impact of digitalisation on the economy is available in the box entitled “Digitalisation and its impact on the economy: insights from a survey of large companies” in this issue of the Economic Bulletin.

- See Masuch et al. (2018), op. cit., and “Economic Surveys: European Union”, OECD, 2018.