Foreword

This is the third issue of the Financial Stability Review (FSR) prepared in the context of the coronavirus COVID-19 pandemic, with many euro area countries having faced a third wave of infections. As a result, a vast number of firms – particularly those in the services, leisure and travel sectors – still cannot operate normally, and the economy is still reliant upon policy support to prevent widespread unemployment, corporate insolvencies and economic contraction. The human and economic costs of the pandemic continue to accrue.

That said, vaccination programmes are progressing and offering a route out of the pandemic. Financial markets have been driven by expectations of an upswing, exemplified by a striking rally in global equity markets. We are optimistic that financial and economic conditions will bounce back. There is, however, a reality that the pandemic will leave a legacy of higher debt and weaker balance sheets, which – if unaddressed – could prompt sharp market corrections and financial stress or lead to a prolonged period of weak economic recovery.

The May 2021 FSR assesses financial stability vulnerabilities – particularly in the corporate sector – and their implications for financial market functioning, debt sustainability, bank profitability and the non-bank financial sector. Risks to financial stability remain elevated and have become more unevenly distributed. The pandemic has imposed higher costs on some vulnerable countries with larger services sectors, which in turn implies a greater need for continued policy support and growing interconnections between their government, corporates and banks. More broadly, the euro area banking sector also continues to face headwinds, with its profitability subject to uncertainty about the balance of loan losses to come and provisions already booked.

This issue of the FSR also looks beyond the pandemic at the other great challenge of our time – climate change – and the risks that this poses to euro area financial stability. A special feature brings together the further enhancements that we have made to our framework for monitoring and assessing climate-related risks to financial markets, banks and non-banks.

The Review has been prepared with the involvement of the ESCB Financial Stability Committee, which assists the decision-making bodies of the ECB in the fulfilment of their tasks. The FSR exists to promote awareness of systemic risks among policymakers, the financial industry and the public at large, with the ultimate goal of promoting financial stability.

Luis de Guindos

Vice-President of the European Central Bank

Overview

Euro area recovery has been delayed, with the impact of the pandemic increasingly concentrated in some sectors

A third wave of coronavirus infections in the euro area has weighed on the near-term economic outlook. More targeted lockdown and social distancing measures and economic adaptation have helped euro area economies to cope better with the pandemic. Nonetheless, many euro area countries faced a third wave of infections in the first months of 2021 that – together with the slow start of the vaccine roll-out – has delayed the economic recovery (see Chart 1, left and middle panels). Looking ahead, progress with vaccinations and the gradual easing of containment measures should support a rebound in economic activity in the course of 2021.

The impact of the pandemic has been increasingly concentrated in some sectors and countries with pre-existing vulnerabilities. The euro area services sector continues to be more adversely affected by the restrictions on social interaction and mobility than manufacturing. The weakest performing sectors, such as trade, transport and accommodation, as well as arts and entertainment, have seen continued declines in gross value added of 2-4 times the aggregate. By contrast, the industrial sector has been recovering faster, supported by improved foreign demand. This sectoral divergence, combined with differing trajectories of the pandemic, has led to a wide divergence in 2021 economic forecasts at the euro area country level (see Chart 1, middle panel).

Chart 1

US growth prospects have improved, triggering a rise in nominal yields with global implications, while the pace of euro area recovery has moderated in the short term

Sources: Our World in Data, Consensus Economics Inc., Bloomberg Finance L.P., Reuters and ECB calculations.

Note: Left panel: vaccination rate refers to people who have received at least one dose of a COVID-19 vaccine as a share of the total population. Data are obtained from the Our World in Data international COVID-19 dataset, which includes a full list of the national authorities disseminating country-level data. For more information, see Mathieu et al., “A global database of COVID-19 vaccinations”, Nature Human Behaviour, 2021. Middle panel: the minimum-maximum range covers 11 euro area countries surveyed by Consensus Economics (Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Portugal and Spain).

Improved economic prospects for the United States led to a notable increase in US long-term nominal interest rates, with global effects. A faster roll-out of vaccinations and agreement on a sizeable fiscal stimulus programme have led to a marked improvement in the US economic growth and inflation outlook (see Chart 1, left and middle panels). The ensuing 60 basis point rise in US ten-year government bond yields since the start of 2021 (see Chart 1, right panel), first driven by higher inflation expectations and later by rising real rates, led to some modest spillovers to the euro area (see Chapter 2). These spillovers were partially offset as the ECB’s Governing Council reinforced its accommodative policy stance by significantly stepping up its asset purchases. Beyond the euro area, rising US yields coupled with an appreciation of the US dollar could generate larger shifts in global capital flows and, as indicated by past crises, may represent a source of risk for emerging market economies with external financing needs (see Box 1 and Chart 2.8, right panel).

Financial markets exhibited remarkable exuberance as US yields rose

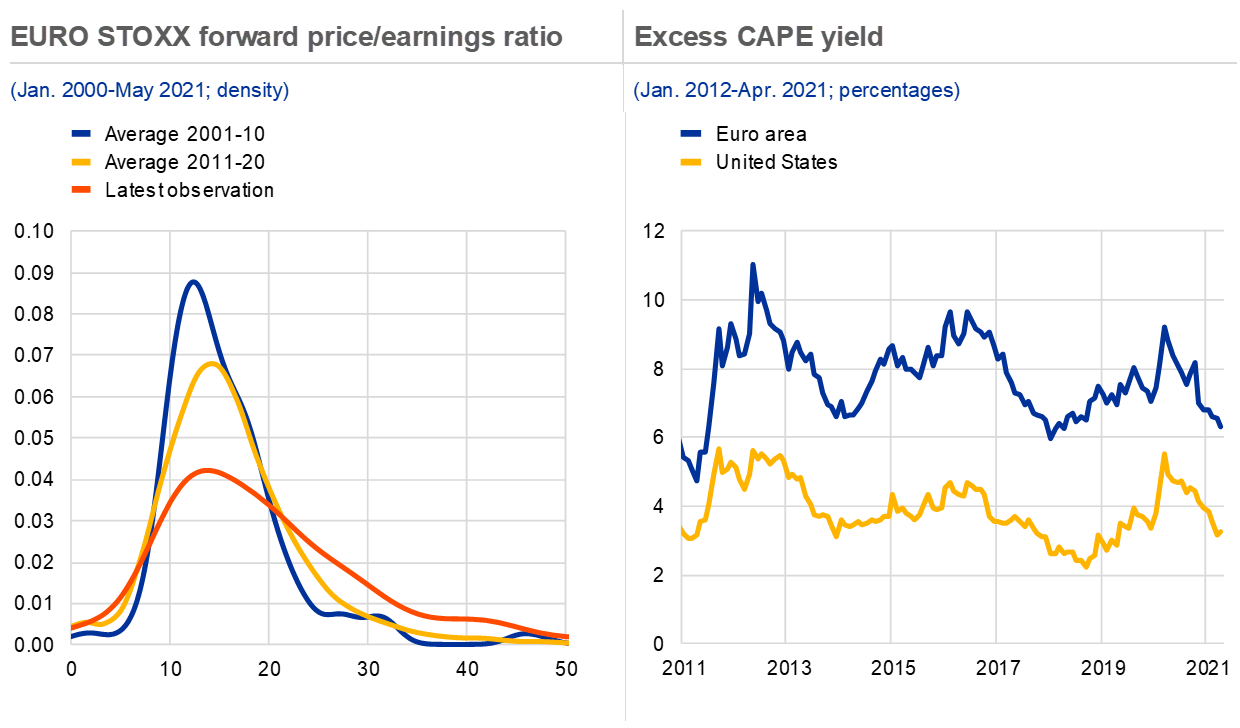

As US interest rates rose and global bond markets sold off, equity markets saw a renewed rally. The rise in US benchmark bond yields led to a global sell-off in bond markets (see Chart 2, left panel). At the same time, equity markets remained buoyant, supported by a recovery in expected earnings and robust risk sentiment (see Chapter 2). The recent rise in composite stock indices has been coupled with a somewhat stronger advance by financial stocks. These had previously underperformed technology stocks, which were among the best performers in 2020 (see Chart 2, right panel).

Chart 2

Despite the recent rotation across and within asset classes, some market segments continue to show signs of elevated valuations and may be at risk of a correction

Sources: Bloomberg Finance L.P., IHS Markit and ECB calculations.

Notes: Left panel: global equity markets are reflected by the MSCI All Country World Index and global bond markets by the Bloomberg Barclays Multiverse Index. Right panel: FAANG: Facebook, Amazon, Apple, Netflix and Google; NFC: non-financial corporate.

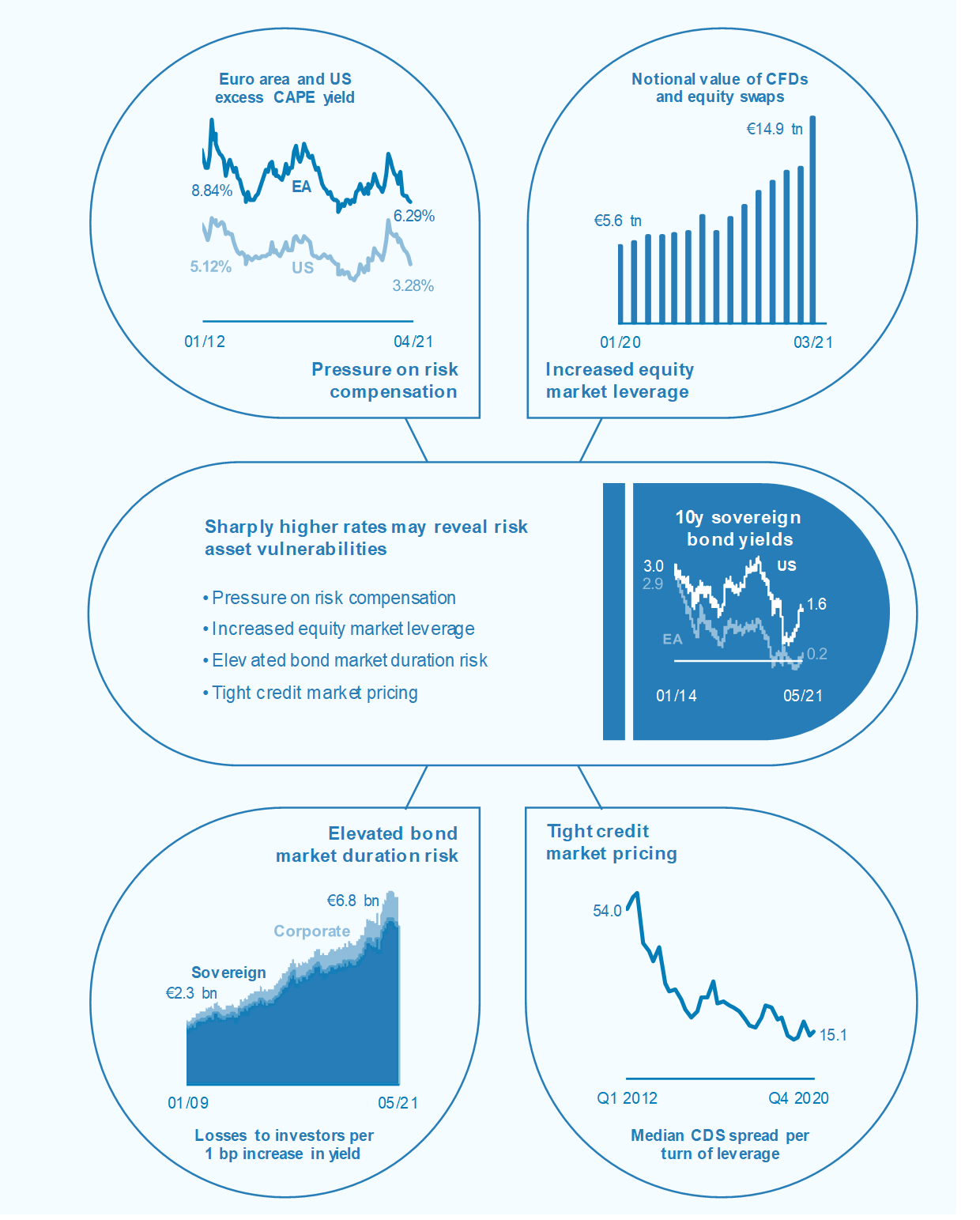

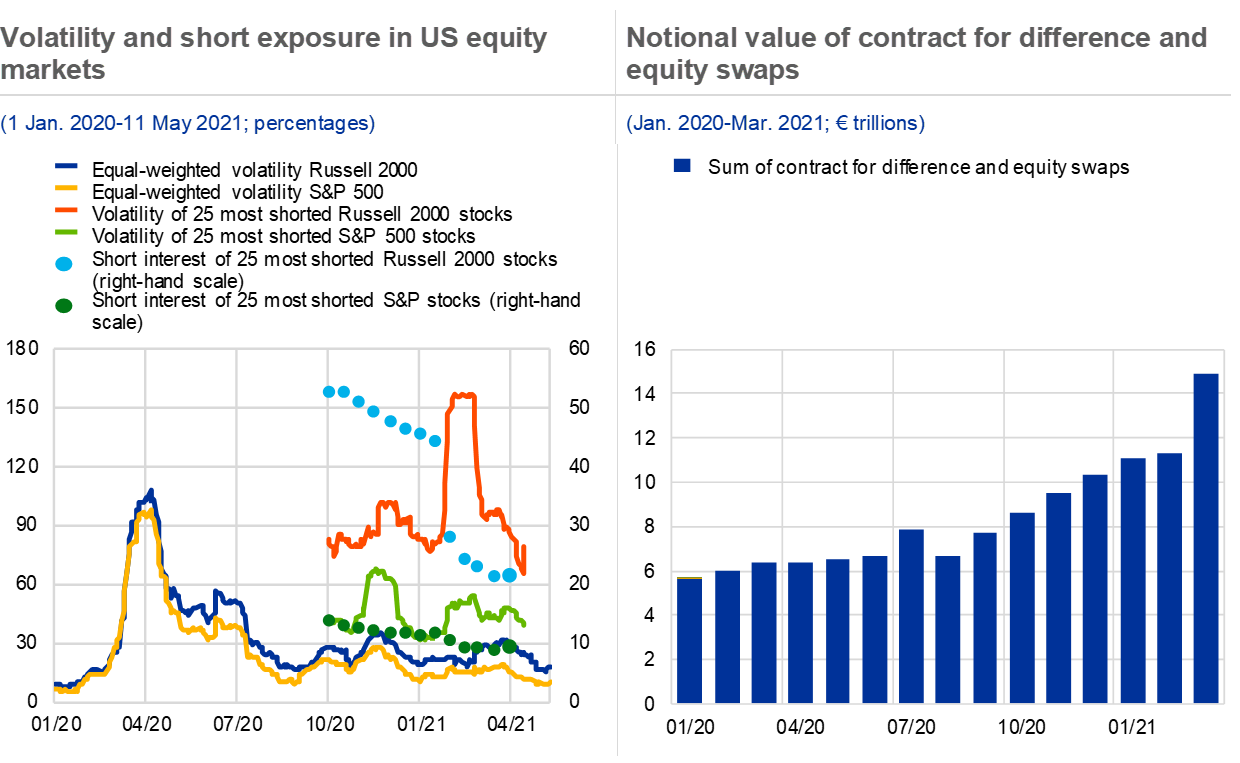

The buoyancy of financial markets has stood in contrast to weaker economic fundamentals, while recent bouts of volatility highlight the risk of repricing. Despite the recent stock price declines in some sectors, stock market valuations remain elevated. In the United States, valuations stand well above pre-pandemic levels, whereas they are at more moderate levels in the euro area. Spreads on euro area non-financial corporate (NFC) bonds remain at risk of an abrupt repricing, in particular for the high-yield segment, where they have fallen below pre-pandemic levels despite growing vulnerabilities. Overall, risk assets remain sensitive to changes in the benchmark yield curve and a reassessment of valuations could ensue if investor expectations regarding the likelihood and pace of monetary policy tightening were to change without an accompanying improvement in growth prospects (see Chapter 2).

Chart 3

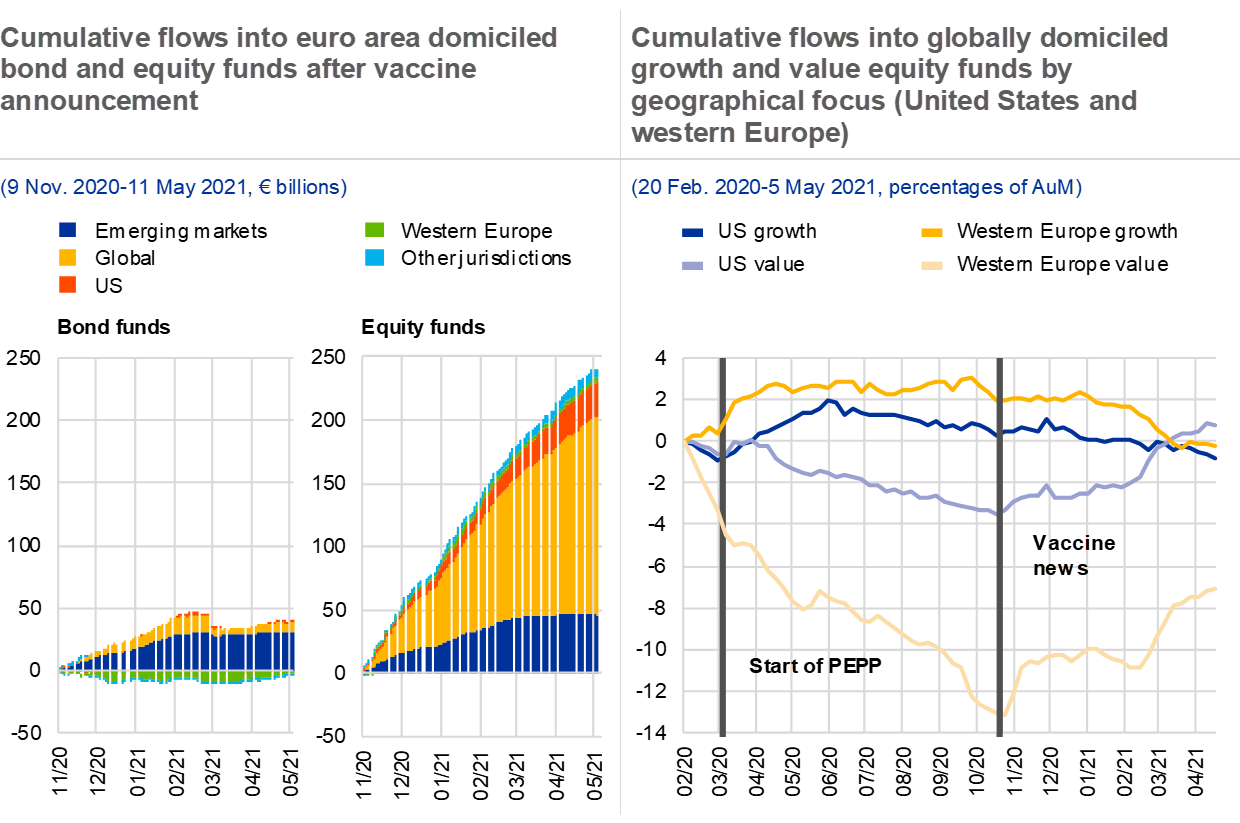

Investment fund flows rebalanced from debt to equity, while non-bank financial institutions overall continue to have large exposures to firms with weak fundamentals

Sources: EPFR Global, S&P Global Market Intelligence, ECB securities holdings statistics and ECB calculations.

Notes: Left panel: “March 2020 turmoil” covers the period from 20 February to 26 March 2020, “Recovery phase” the period from 27 March to 6 November 2020, “Vaccine news” the period from 9 November 2020 to 12 February 2021 and “Since bond market correction” the period from 15 February to 11 May 2021. “Other jurisdictions” refer to euro area funds with an investment focus in the Asia-Pacific region and Canada. AUM: assets under management. Right panel: vulnerable holdings are defined as holdings with a negative credit watch or outlook by Standard & Poor’s. ICs: insurance corporations; IFs: investment funds; PFs: pension funds.

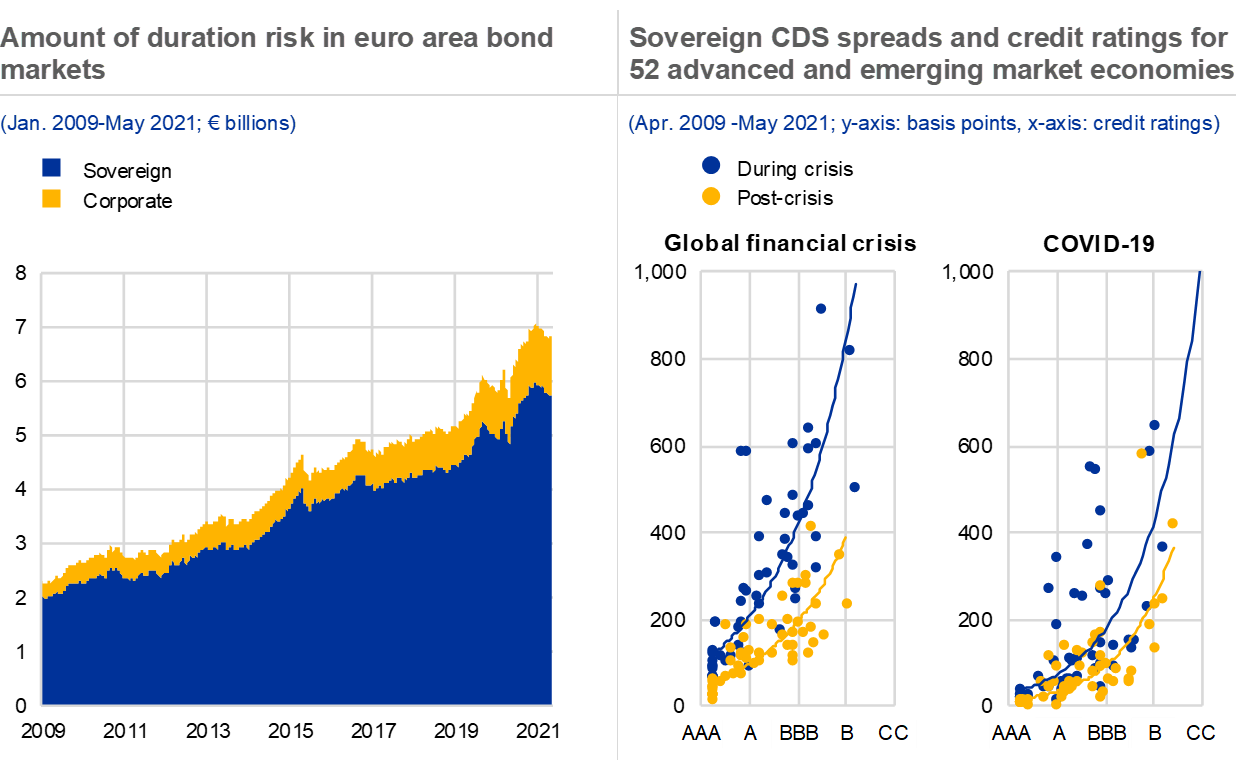

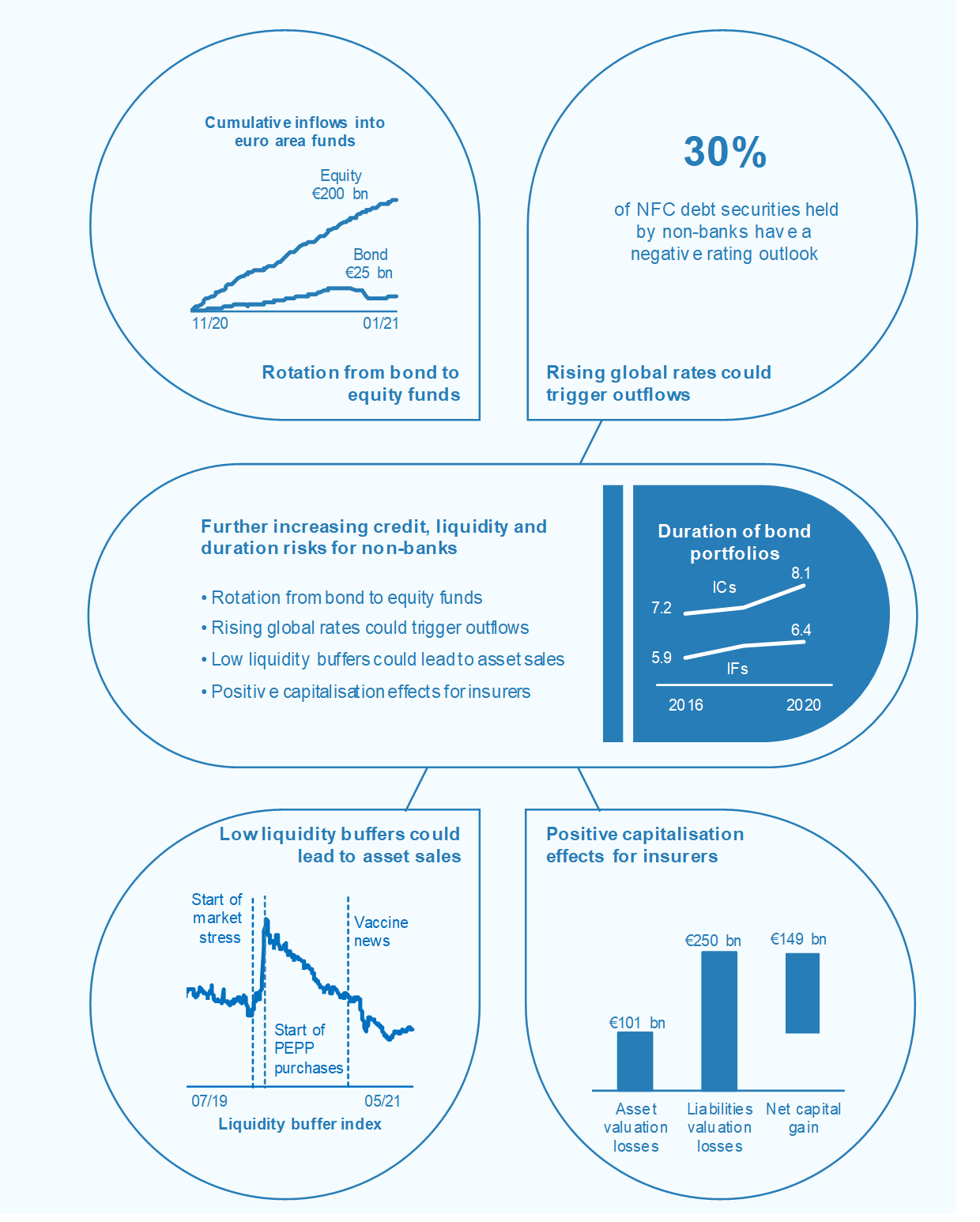

Many euro area investment funds, insurers and pension funds are exposed to a further rise in yields or a correction in credit markets. Investment fund flows have also rebalanced from debt to equity given rising yields (see Chart 3, left panel). Still, in their search for yield over recent years, non-banks have increased the duration risk of their debt securities portfolios to multi-year highs. This increases the sensitivity of their assets to higher rates, though for insurers and pension funds asset valuation losses could be compensated for by a fall in the value of their liabilities given the sector’s negative duration gap. Non-banks also have large exposures to firms with weak fundamentals, with more than a quarter of the sector’s NFC debt holdings subject to a negative credit outlook or credit watch by rating agencies (see Chart 3, right panel). Roughly half are also BBB-rated, only one notch above high-yield status.

In parallel, since last November, investment funds have further reduced their liquidity buffers. Cash buffers and liquid asset holdings are now below pre-pandemic levels and are approaching new lows, leaving the sector highly vulnerable to fire sales of assets in the event of large-scale redemptions. Investment funds’ liquidity risk has increased amid a search for yield (see Box 6) over recent years. This underscores the importance of strengthening the resilience of the non-bank financial sector, including from a macroprudential perspective (see Chapter 5).

Corporate solvency challenges could weigh on sovereigns, households and creditors

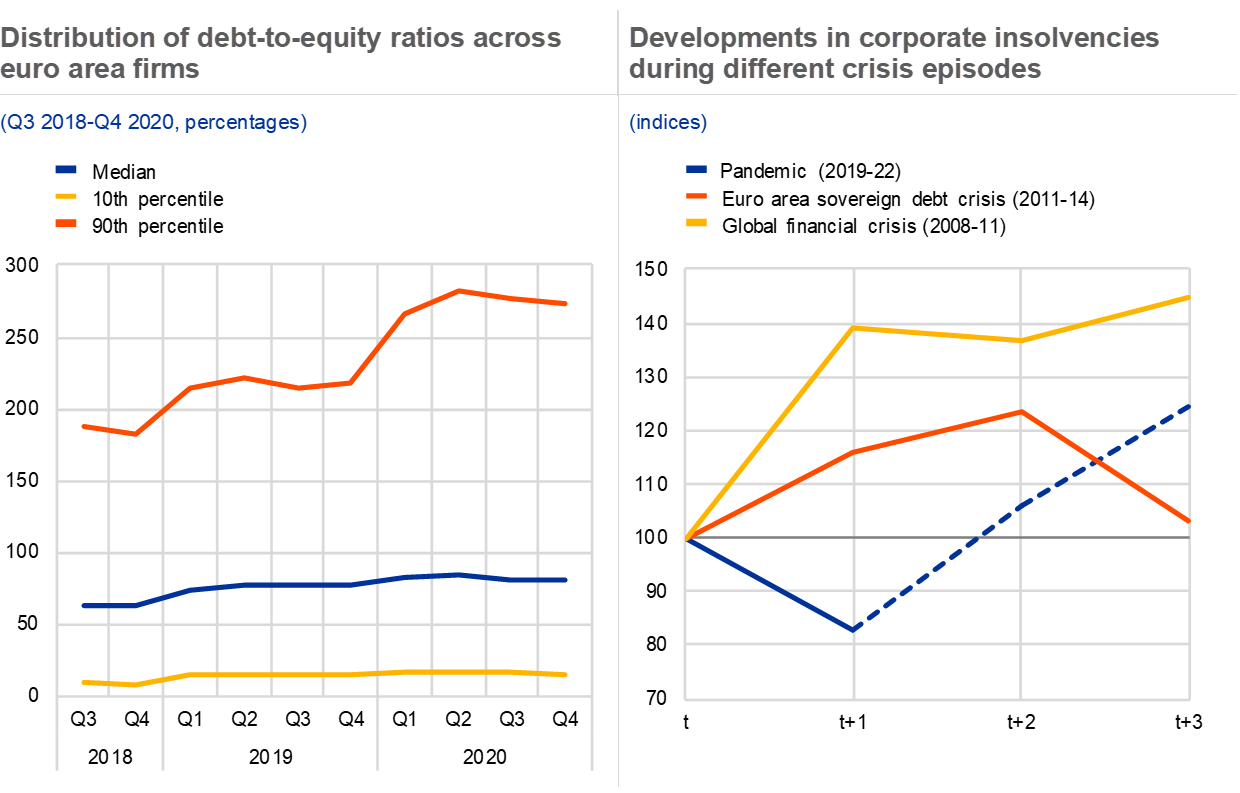

Reliance on debt has increased among vulnerable firms, amid higher rollover risks. Debt-to-equity ratios have increased considerably among the most leveraged firms, with the 90th percentile increasing from 220% at end-2019 to over 270% in the final quarter of 2020 (see Chart 4, left panel). Corporate earnings expectations for the euro area have remained below pre-pandemic levels, while corporate funding conditions remained around the tightest levels since the pandemic started, especially for small and medium-sized enterprises (SMEs), highlighting elevated refinancing risks. Higher (risk-free) rates would increase debt servicing costs from historical lows and could raise medium-term risks in countries with elevated debt levels. The substantial increase in liquidity buffers among euro area firms may cushion corporate rollover risks, even though this appears to be particularly relevant for large listed firms.

Chart 4

Increased leverage, in particular by the most vulnerable corporates, may contribute to an increase in corporate insolvencies

Sources: S&P Global Market Intelligence, Allianz Euler Hermes and ECB calculations.

Notes: Left panel: a fixed sample of 1,183 euro area non-financial corporations with total assets larger than €50 million as at Q3 2019; data available for Q4 2020 are used. Right panel: the dashed line indicates projections. On the x-axis, “t” refers to the starting year of the respective crisis episode, i.e. 2008, 2011 and 2019 respectively; “t+1” refers to the year after, i.e. 2009, 2012 and 2020, and so on. Insolvency statistics and projections are taken from “Vaccine Economics”, Euler Hermes, Allianz Research, 18 December 2020.

Solvency risks in the corporate sector are set to rise as public support measures fade. Extensive policy support has kept corporate insolvencies unusually low in a period of extreme economic weakness, unlike during previous crisis episodes (see Chart 4, right panel). The impact of the pandemic on corporates is increasingly concentrated in the services sectors and among SMEs. This implies that a sudden tightening of financing conditions or a further delayed economic recovery could have more severe implications for financial stability than the aggregate picture suggests, in particular in countries heavily reliant on pandemic-sensitive sectors. Therefore, even as the economy recovers, corporate insolvencies are expected to increase from the very low levels observed in 2020, partly driven by a backlog of insolvency cases. As a result, governments face a delicate balance between prematurely adjusting support measures, which may contribute to triggering a wave of corporate insolvencies, and maintaining support measures for too long and thus keeping unviable corporates alive (see Special Feature A).

Chart 5

Euro area households may be challenged by spillovers from corporates and a correction in residential property markets

Sources: Eurostat, ECB, Jones Lang LaSalle and ECB calculations.

Notes: Left panel: sensitive sectors comprise mining, construction, retail and wholesale trade, transport, accommodation and food services, professional and administrative services, as well as arts and entertainment and other services. Sensitivity to the pandemic has been determined by the relative year-on-year loss in gross value added. Capital letters refer to NACE codes as follows: A – Agriculture; J – Communication; K – Financials; O – Public sector; P – Education; Q – Health services. The size of the bubbles refers to the sectors’ share in total bank loans to all sectors. The grey line indicates the linear trend.

An increase in corporate insolvencies may impact households via employment prospects, so far prevented by policy support measures. On aggregate, household balance sheets have been cushioned so far, thanks to government income support schemes, record high saving rates, continued robust developments in euro area residential real estate markets and the recovery in stock markets. However, high dependence on government support schemes makes households vulnerable, and their financial and employment situation could worsen in the event of prolonged economic weakness, which may translate into job losses linked to a growing number of corporate insolvencies (see Chart 5, left panel).

At the same time, continued strength in residential real estate markets and mortgage lending has increased household indebtedness and vulnerabilities. The risk of a correction in residential real estate markets has increased amid signs of overvaluation for the euro area as a whole. In contrast to the resilience of residential real estate markets, commercial real estate markets are already facing a substantial market correction (see Chart 5, right panel). A further decline in commercial real estate prices could feed through to the financial system via increased credit risk, decreased collateral values and losses on direct holdings, as well as to lower investment and economic activity by non-financial corporations.

Chart 6

Continued need for government support may challenge the sustainability of public finances in some countries and make the withdrawal of policy support more difficult

Sources: European Systemic Risk Board, European Commission, ECB and ECB calculations.

Notes: Left panel: data refer to euro area aggregates. Government contingent liabilities include the financial sector. The snowball effect relates to the interest rate-growth differential. SovCISS: composite indicator of systemic stress in euro area sovereign bond markets; for further information, see Garcia-de-Andoain, C. and Kremer, M., “Beyond spreads: measuring sovereign market stress in the euro area”, Working Paper Series, No 2185, ECB, October 2018. Right panel: discretionary fiscal measures include direct grants as well as tax measures. Numbers refer to actual take-ups. For further information, see “Financial stability implications of support measures to protect the real economy from the COVID-19 pandemic”, European Systemic Risk Board, February 2021.

The continued need for policy support may add to medium-term sovereign debt sustainability concerns in more vulnerable countries. The aggregate euro area sovereign debt-to-GDP ratio rose to 100% in 2020, up from 86% of GDP in 2019, as governments have financed extensive economic support to cushion households and firms. Fiscal policy support has been particularly large in some countries with a larger share of economic sectors most impacted by the pandemic and lockdowns (see Chart 6, right panel). As a result, vulnerabilities from the outstanding stock of debt appear higher than in the aftermath of the global financial crisis and the euro area sovereign debt crisis, although debt servicing and rollover risks appear more benign given continued favourable sovereign financing conditions in terms of both pricing and duration (see Chart 6, left panel). Contingent liabilities could increase sovereign debt levels further if the economic situation turns out to be weaker than expected and pandemic-related corporate loan guarantees are called on a broader scale (see Box 2). The associated increase in public debt levels, further delays in the implementation of the EU recovery fund or the emergence of an adverse sovereign-bank-corporate nexus (see Box 4) could trigger a reassessment of sovereign risk by market participants and reignite market pressures on more vulnerable sovereigns. This may render the exit from policy measures more challenging in vulnerable countries with a higher reliance on fiscal support measures.

Improved market sentiment towards euro area banks, but profitability and asset quality concerns remain

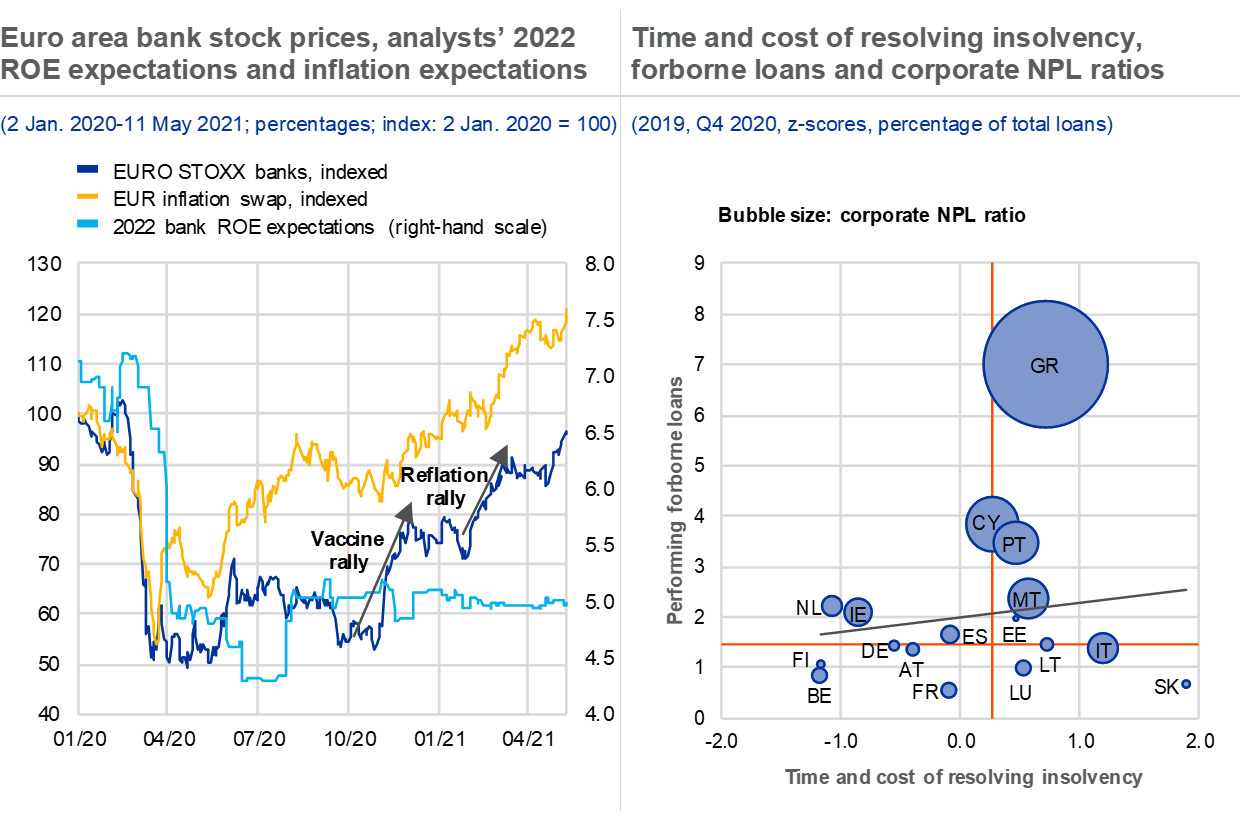

Euro area bank stock prices have recovered markedly from the low levels of October 2020. Bank equity prices have rallied in two waves on positive news about vaccines and reflation expectations. Banks outperformed the overall market, mirroring a wider recovery in previously underperforming stocks. While investors appear to anticipate that a steepening of the yield curve could support bank profitability, analysts’ return on equity (ROE) expectations for 2022 have remained unchanged since last summer (see Chart 7, left panel). Nonetheless, euro area bank valuations remain depressed by both international and historical standards. Improved market sentiment towards banks, coupled with market expectations of an extension of the pandemic emergency purchase programme, have also translated into tighter spreads on bank bonds, further improving market funding conditions for euro area banks.

Chart 7

Market sentiment towards euro area banks has improved significantly, despite continued profitability challenges and growing asset quality concerns

Sources: Bloomberg Finance L.P., World Bank Doing Business Indicators, ECB supervisory data and ECB calculations.

Notes: Left panel: “EUR inflation swap” refers to the euro area five-year forward inflation-linked swap rate five years ahead. Right panel: measures of time and cost of resolving insolvency are transformed into z-scores, i.e. they are presented as standard deviations from the sample mean and then averaged so that they can be jointly presented on one scale. Forborne loans refer to the share of total loans with forbearance measures. The bubble size corresponds to the NPL ratio for corporate loans. The red lines indicate sample medians. The grey line represents the linear trend. NPL: non-performing loan.

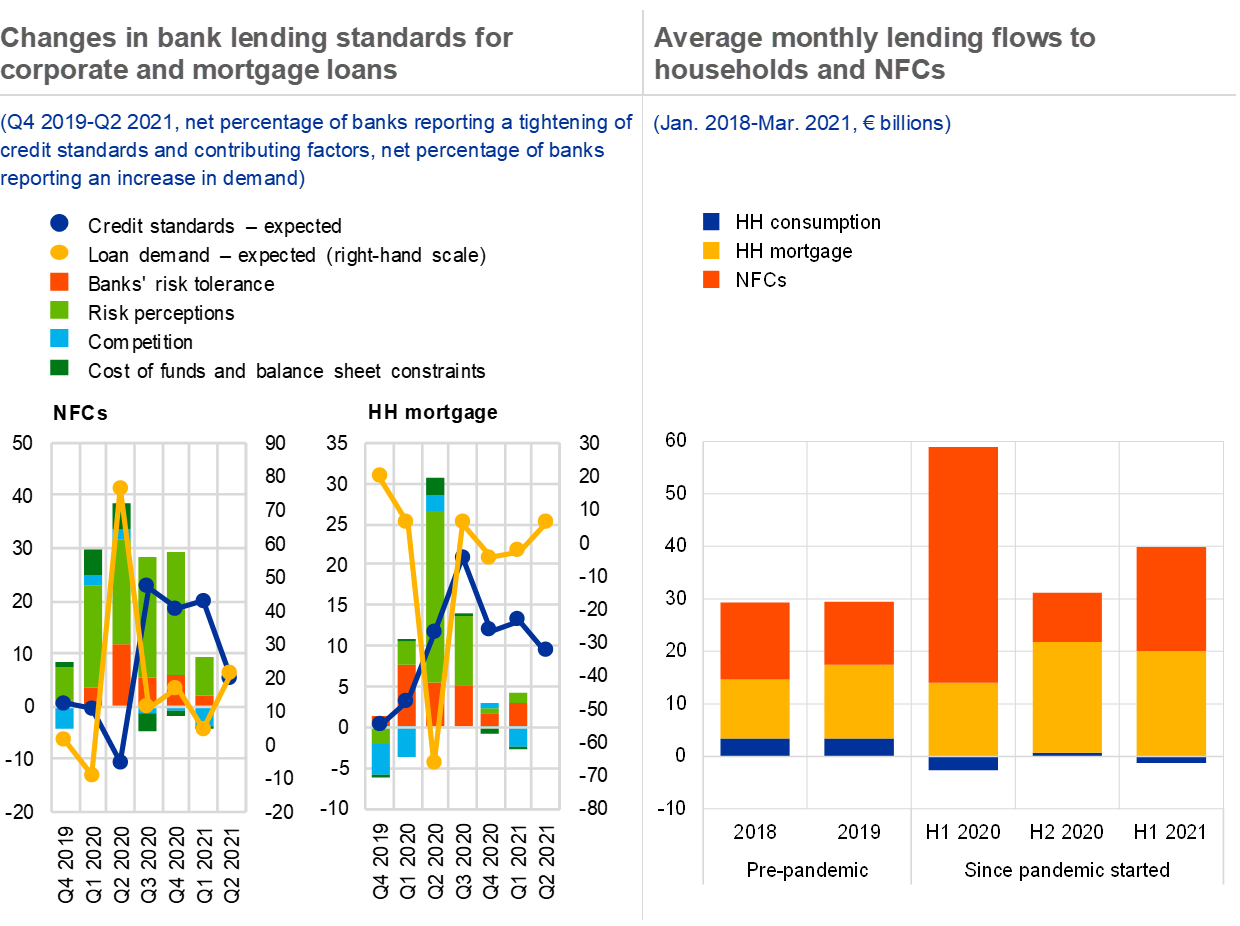

Nevertheless, the outlook for bank profitability remains weak and the prospects for loan demand are uncertain. Euro area banks’ ROE fell from 5.3% in 2019 to 1.3% in 2020 owing to pandemic-related loan loss provisions and ongoing margin compression in a low interest rate environment (see Chapter 3). Heterogeneity across countries was high, with banking sectors in some countries recording sizeable losses (see Chart 3.4). Despite recently improving market sentiment towards euro area banks, market analysts still expect profitability to recover only gradually, projecting an ROE of 3% and 5% for 2021 and 2022 respectively, given higher provisioning needs and lower expected operating income. The outlook for lending could be challenging as a result of both tighter credit standards and lower corporate credit demand. The former is related to banks’ heightened risk perceptions, while the latter is associated with the adjustment of state guarantee programmes and the need to improve balance sheets.

Early signs of a rise in loan impairments are becoming increasingly visible. Cushioned by large-scale fiscal, monetary and prudential support, bank asset quality has been preserved despite the sharp recession. In fact, the aggregate non-performing loan (NPL) ratio for the euro area reached its lowest level on record at 2.7% in 2020, as banks reduced legacy portfolios. Loan loss provision flows returned to pre-pandemic levels in the second half of 2020. But the normalisation may prove temporary, as early indicators of deteriorating asset quality are becoming increasingly visible, including a rise in forbearance. This is particularly the case in countries where lengthy and costly insolvency procedures inhibit claim enforcement (see Chart 7, right panel). A weaker than expected economic recovery and growing vulnerabilities in the corporate sector may entail higher loan loss provisioning going forward. In addition, as moratoria and public guarantees are gradually adjusted (see Chapter 1 and Box 2), credit risk may reappear with a lag, also implying increased loan loss provisions.

Climate change may pose material risks to financial stability

Climate-related risks to euro area banks, funds and insurers could be material, particularly if climate change is not mitigated in an orderly fashion. Banks and non-bank financial institutions alike are faced with the task of managing the implications of climate change over the medium to long term (see Special Feature B). Both need to manage their exposure to a transition to a low-carbon economy and their exposure to physical risks associated with extreme weather and climate-related events or more insidious changes in climate (see Chart 8). ECB analysis suggests that such risks appear to be particularly concentrated in certain sectors, geographical regions and individual banks, exacerbating the related implications for financial stability. At the same time, data and methodological gaps still need to be addressed to evaluate climate-related risks comprehensively. In addition, climate-related financial risks that may emerge from the interplay between banks and insurers need to be recognised, with insurance coverage likely deteriorating as extreme weather and climate-related events become more frequent.

Chart 8

Climate-related risks, both transitional and physical, could be material for euro area banks, funds and insurers, given high risk exposures and concentration

Sources: Four Twenty Seven, Urgentem, ECB (AnaCredit), ECB securities holdings statistics and ECB calculations.

Notes: The left panel shows the exposure of banks and non-bank financial institutions to firms that issue bonds or are listed in the equity market. The sample for loans consists of €4 trillion of exposures above €25,000 to non-financial corporations (NFCs) matched with emission data, corresponding to 80% of euro area loans to NFCs. The firms are classified as low, medium and high emitters according to their emission intensities in December 2019, i.e. the ratio of CO2 emissions to revenues. Low emitters are firms with less than 309 CO2-equivalent tonnes per million USD revenue (33rd percentile), while high emitters are firms with more than 1,068 CO2-equivalent tonnes per million USD revenue (66th percentile). Right panel: “high-risk firms” include those firms that are located in areas already highly exposed, or increasingly exposed, to physical hazards. See also notes to Chart B.2 for further details.

Policy action may be required to ensure the resilience of the financial system to climate-related risks. Enhanced climate-related disclosure requirements, including in relation to companies’ forward-looking emission targets, and deeper, more effective green financing are essential steps in a smooth transition towards a sustainable economy and a general reduction of climate-related vulnerabilities. At the same time, possible market failures can stem from data gaps, which would raise the risk of greenwashing. The upcoming ECB climate stress test will also analyse trade-offs in a forward-looking manner, thereby providing a further basis for future policy discussions. Ultimately, given the systemic dimension, considerations about how to mitigate climate-related risks in the financial system require a macroprudential perspective to be effective and to ensure cross-sector consistency.

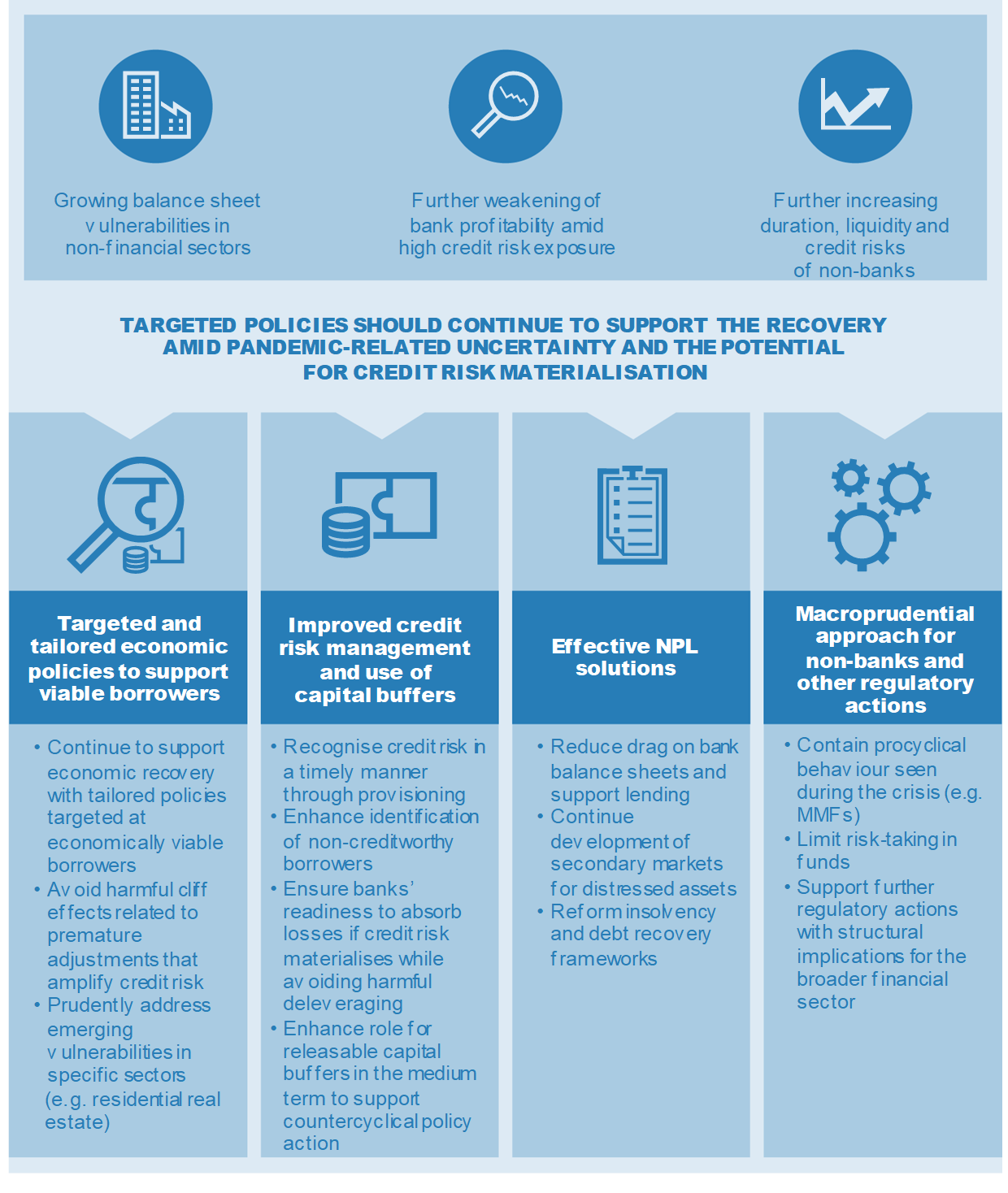

Policies should continue to support the recovery, while targeting the build-up of vulnerabilities in selected areas

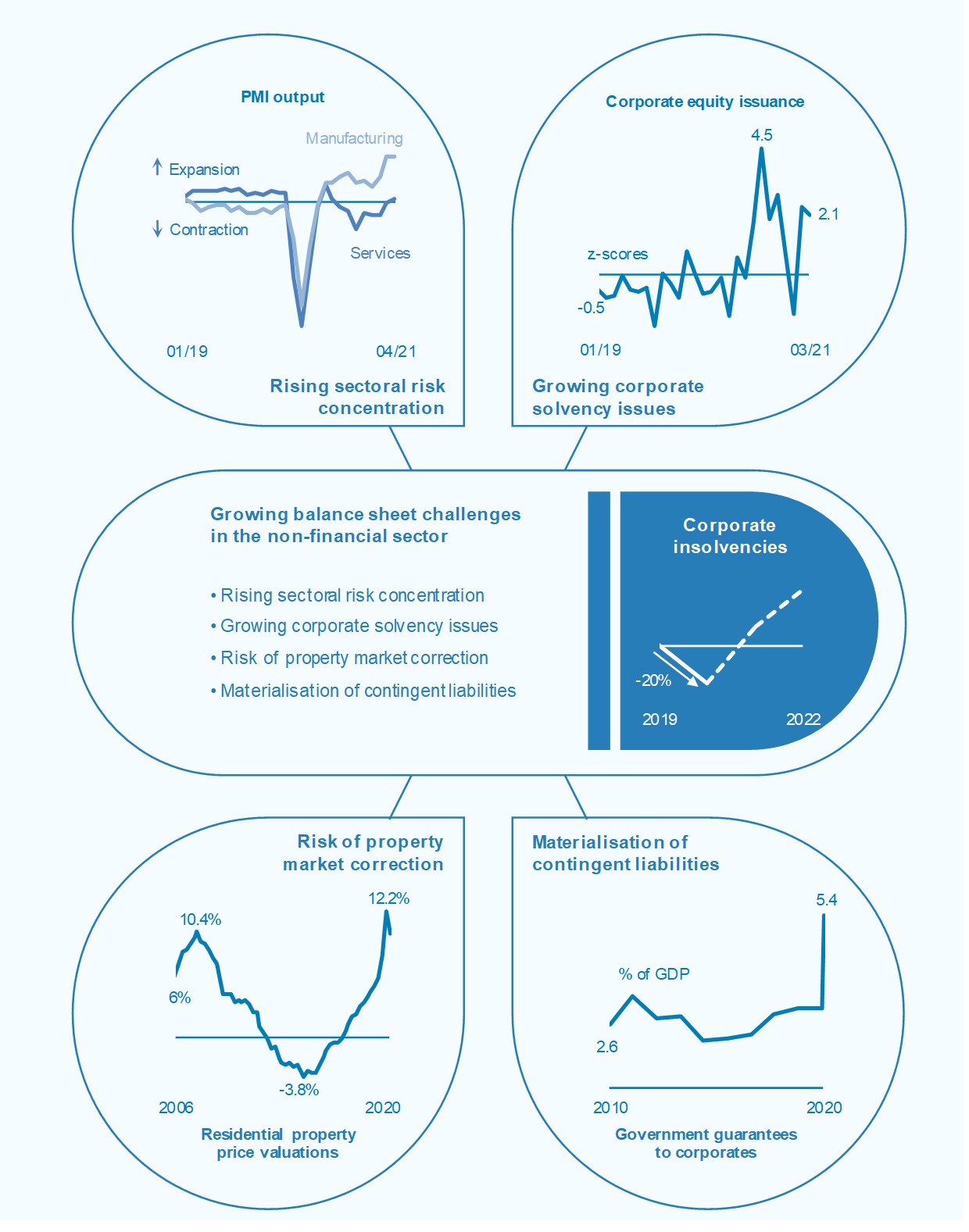

Extended policy measures have remained key in mitigating the economic costs of the pandemic, but vulnerabilities continue to build up in some areas. With many euro area countries facing renewed surges in infections, lockdown measures have been reinstated and economic support measures maintained. Divergence across countries and sectors has continued to increase, ultimately leading to a concentration of risk that often coincides with pre-existing vulnerabilities in both the real economy and the financial sector. Looking ahead, medium-term vulnerabilities for euro area financial stability remain elevated and relate to: (i) a mispricing of some asset classes, raising the risk of corrections in markets; (ii) growing balance sheet challenges in the public and non-financial private sectors; (iii) weaker bank profitability amid high credit risk exposure; and (iv) further increases in duration, liquidity and credit risks of non-banks. The financial stability implications could be amplified by the emergence of an adverse feedback loop across various sectors of the economy.

Policies should remain broadly accommodative but could be more targeted to support a robust economic recovery amid remaining uncertainty and the potential for credit risk to materialise. Conditional on the economic impact of the pandemic, the extensive policy support, in particular for corporates, could continue to move gradually from being broad based to more targeted. In this context, fast and effective use of the €750 billion Next Generation EU (NGEU) recovery funds would complement national support measures and mitigate cross-country divergences in the coming years. Specifically for banks, capital relief measures should continue to prevent excessive deleveraging, while proper and timely recognition of credit risk would maintain confidence in balance sheets. In this context, it is worth noting the preliminary evidence which suggests that some banks may be reluctant to use available capital buffers, which could in turn affect credit conditions, especially for corporate lending. In the medium term, a higher share of releasable capital buffers could be considered, as it can enhance banks’ ability to absorb losses and maintain the provision of key financial services in a crisis. In addition, concerns related to the expected asset quality deterioration in the banking sector reinforce the need for effective NPL solutions. Given the low interest rate environment and profitability challenges, efforts to address structural issues across banks should be stepped up. Finally, from a broader regulatory perspective, strengthening the banking union and the timely, full and consistent application of Basel III remain key policy priorities for the banking sector going forward.

Further progress towards developing a macroprudential framework for non-banks is expected and would be highly welcome. In particular, the Financial Stability Board is developing recommendations targeting structural vulnerabilities associated with money market funds, open-ended investment funds and margining practices in order to enhance the resilience of the non-bank financial sector. Once issued, they should be swiftly implemented in the European Union as appropriate.

1 Macro-financial and credit environment

1.1 Increasing concentration of risk in more vulnerable sectors and countries

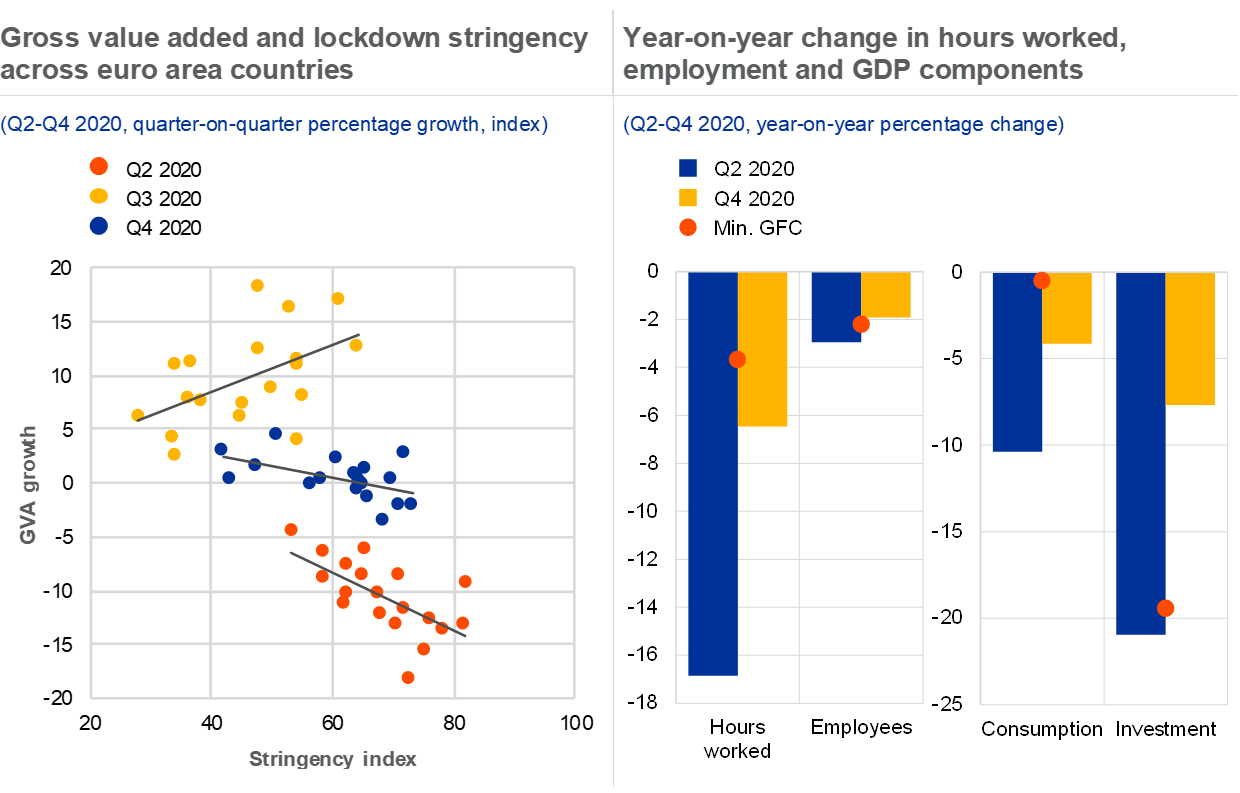

Economic activity fell amid renewed lockdown measures, but activity has proved more resilient than during the first lockdown. The resurgence of coronavirus cases last autumn caused euro area governments to reinstate tight containment measures, which weighed on economic activity in the euro area in the fourth quarter of 2020 and the first quarter of 2021. At the same time, the economic impact of the second lockdown remained more contained than that of the first lockdown for two reasons. First, containment measures were on average less stringent than in the second quarter of 2020. Second, economic activity has become less sensitive to the stringency of lockdown measures, including across countries with different stringency levels, as firms and households have adapted to the new environment (see Chart 1.1, left panel). This higher resilience is not only visible on average, but also when comparing countries with different levels of stringency.

Chart 1.1

Economy more resilient to lockdown measures, but considerable slack remains

Sources: ECB quarterly sectoral accounts, Hale et al., Eurostat and ECB calculations.

Notes: Left panel: the stringency index used is the Oxford COVID-19 Government Response Tracker from the Blavatnik School of Government, University of Oxford. It is based on 20 indicators, ranging from information on containment and closure policies (e.g. school closures, restrictions on movement) to economic (e.g. income support to citizens) and health system (e.g. coronavirus testing regime or emergency investments in health care) policies. It reports the strictness of lockdown-style policies that primarily restrict people’s behaviour on a scale between 0 and 100. See Hale, T., Angrist, N., Goldszmidt, R., Kira, B., Petherick, A., Phillips, T., Webster, S., Cameron-Blake, E., Hallas, L., Majumdar, S. and Tatlow, H., A global panel database of pandemic policies (Oxford COVID-19 Government Response Tracker), Nature Human Behaviour, 2021. GFC: global financial crisis; GVA: gross value added.

Slack in labour markets and subdued investment could point to a sluggish recovery. Although economic activity recovered to some extent in the second half of 2020, the number of employees and total hours worked remain substantially below pre-pandemic levels (see Chart 1.1, right panel). While hours worked are likely to rebound once employees on short-time work return to full-time work, the high share of laid-off workers who left the labour force altogether could herald a more persistent disruption to labour markets. Non-employed workers, especially from sectors that face a more permanent drop in demand, could face difficulties in re-entering the labour market after the pandemic, which would weigh on economic growth. Similarly, investment remains subdued, reflecting firms’ uncertainty about the timing of the pandemic and their own growth prospects after the pandemic subsides (see Chart 1.1, right panel). Looking back at the global financial crisis as a precedent, a slow recovery of investment may also be a harbinger of a more sluggish recovery from the pandemic than the swift rebound in consumption suggests.

While the availability of vaccines has improved the medium-term economic outlook, uncertainties remain in the near term. The approval of multiple vaccines in late 2020 and early 2021 improved the economic outlook for the euro area and reduced the uncertainty about the length of the pandemic. While this has boosted the growth prospects for 2022, the ongoing containment measures weigh on the near-term outlook (see Chart 1.2, left panel). In addition, the slow start to the vaccine roll-out in the euro area makes it unclear when the euro area will reach herd immunity and return to normal economic activity. Moreover, the virus continuing to evolve poses considerable tail risks as vaccine-resistant mutations may yet emerge, necessitating a prolonged period of constrained social and economic activity.

Chart 1.2

Vaccines improve growth outlook, but slow roll-out and moderate fiscal support cause divergence from the United States and create tail risk of a prolonged pandemic

Sources: ECB Survey of Professional Forecasters (SPF) and Our World in Data.

Notes: Left panel: the horizontal axis displays the different quarterly SPF vintages containing the average real GDP expectations among professional forecasters. Growth rates are cumulative with 2019 = 100. Right panel: For more information on the data see the notes to chart 1 in the Overview. The linear projection is based on the average daily vaccination pace in the two weeks before the data cut-off date (11 May 2021). The shaded area indicates the levels of vaccinations typically associated with herd immunity (here excluding persons who have recovered from COVID-19). Emerging market economies (EMEs) are broadly consistent with the countries covered in Box 1 (subject to data availability) and comprise Argentina, Brazil, India, Indonesia, Mexico and Russia.

The slow start to the vaccination campaign and a more moderate fiscal stance may leave the euro area lagging its advanced economy peers. The euro area was initially much slower than other advanced economies to ramp up vaccination (see Chart 1.2, right panel). As the pace of vaccination in the euro area picks up, however, this gap is narrowing. Nonetheless, the euro area may take longer than the United States or the United Kingdom to reach herd immunity depending on the further vaccination progress, which would allow for a return to normal. In addition, euro area governments have adopted a more moderate fiscal stance relative to GDP and compared with the respective output gap than the US administration in 2021. Although the “Biden package” of USD 1.9 trillion is expected to generate positive spillovers of up to 0.3% of real GDP for the euro area, the more accommodative fiscal stance in the United States could further increase the divergence between the two economic areas. Such a disparity in growth prospects could create upward pressure on real interest rates in the euro area and tighten overall financing conditions to the detriment of euro area corporates, households and sovereigns.

Global risks remain contained, and emerging markets proved resilient as policy uncertainty in the United Kingdom and the United States fell. Despite the economic challenges and the slow global vaccination roll-out, financial conditions and capital flows in emerging markets have remained fairly resilient so far. These dynamics are, however, highly dependent on global risk appetite and monetary policy accommodation in advanced economies (see Box 1). The agreement of a trade deal between the United Kingdom and the European Union at the end of 2020 and the transition to a new administration in the United States have reduced policy uncertainty in both the United Kingdom and the United States. At the same time, the tensions relating to export controls on vaccines highlight the importance of trade in overcoming the pandemic, but also its fragility.

Chart 1.3

Increasingly asymmetric impact of the pandemic gives rise to tail risks in most affected sectors

Sources: IHS Markit and ECB quarterly sectoral accounts.

Notes: Right panel: the horizontal axis shows the percentage change in gross value added (GVA) between the fourth quarter of 2019 and the second quarter of 2020, whereas the vertical axis shows the difference between GVA in the second quarter of 2020 and the fourth quarter of 2020 in percentage points. Observations refer to country/sector observations at NACE Rev. 1 level. More sensitive sectors comprise mining, construction, retail and wholesale trade, transport, accommodation and food services, professional and administrative services, arts and entertainment, and other services. Sensitivity to the pandemic is determined by the relative year-on-year loss in gross value added.

The divergence across sectors widened as containment measures became more targeted. The gradual reopening and the more targeted containment measures during the second lockdown allowed less badly affected sectors to widely resume normal activity, whereas services such as tourism, entertainment and travel to a large extent remained shut (see Chart 1.3, left panel). Consequently, the most affected sectors were not only hit most in the first half of 2020, but also rebounded less relative to the initial drop in the second half of 2020, increasing the divergence across sectors (see Chart 1.3, right panel). This divergence may widen further if the slow roll-out of vaccines necessitates continued containment measures over the summer tourism season, especially in southern European countries.

Continued cross-sectoral divergence could trigger a costly reallocation of resources. The widening sectoral divergence poses risks to financial stability for two reasons. First, the most affected sectors face more severe liquidity and solvency risks than aggregate economic indicators suggest, and the materialisation of these risks could trigger an unravelling of macro-financial imbalances with adverse spillovers to other sectors. Second, the continued divergence will at some stage lead to a reallocation of resources from the most affected sectors to sectors with better growth prospects. The costs associated with such a cross-sectoral reallocation of resources, for example due to retraining of workers, could further weigh on the strength and pace of the economic recovery in the short to medium term.

Box 1

Emerging markets’ vulnerability to a reassessment of risk

Financial conditions in emerging market economies (EMEs) have weathered the COVID-19 crisis well so far, despite an intense but short-lived stress episode at the onset of the pandemic. Financial conditions in EMEs have rebounded strongly since March 2020; they currently stand at levels similar to before the pandemic thanks to lower bond spreads and higher equity prices. Capital flows have also recovered, with market segments typically judged to be riskier by foreign investors, such as equity and local currency debt, recording strong inflows in the second half of last year. This rebound helped to relieve pressures on financial systems and support activity in EMEs. Nevertheless, recent concerns about rising bond yields and higher than expected inflation in advanced economies have translated in a tightening of financial conditions and slowdown of capital flows to EMEs. In this context, this box assesses potential vulnerabilities facing large EMEs and the risks posed to euro area financial stability.

More1.2 Benign financing conditions limit debt sustainability risks

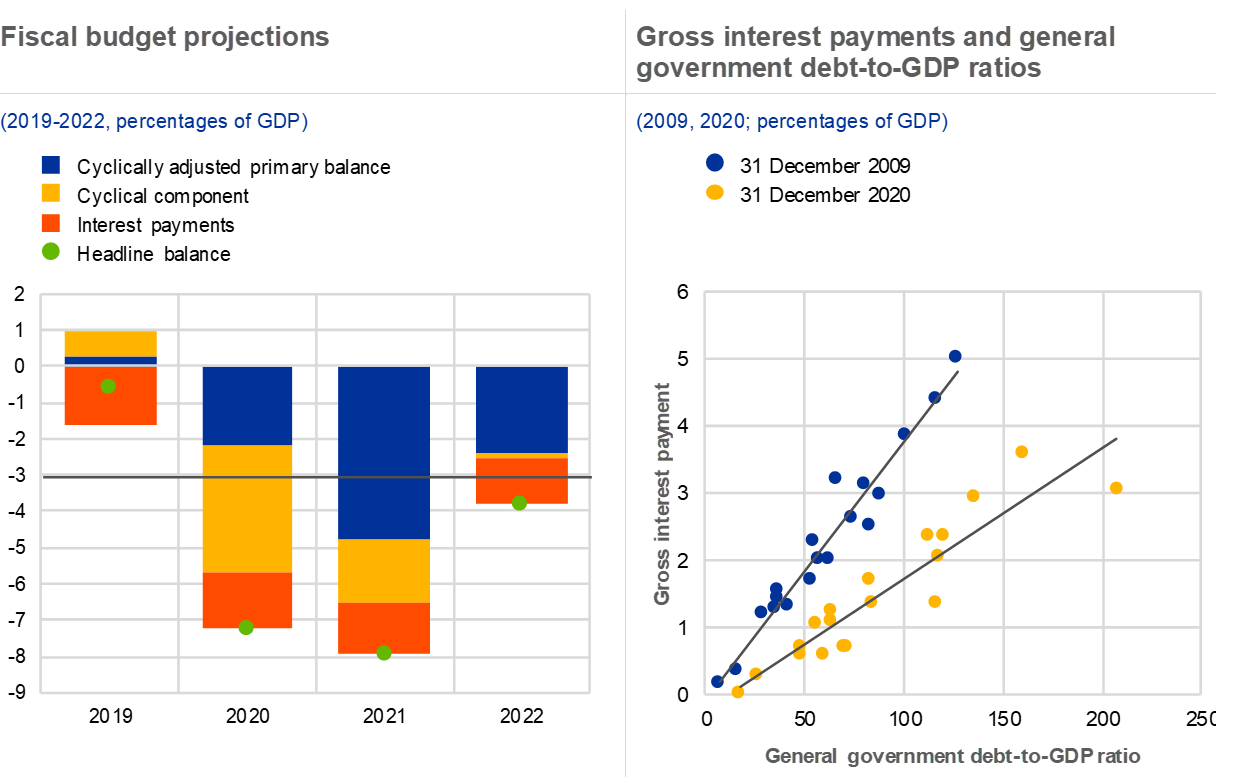

The pandemic continues to weigh on fiscal budgets in 2021 as governments extend support measures. When governments reinstated strict containment measures at the end of last year, they also extended existing support measures to cushion the economic impact on firms and households. As a consequence, fiscal deficits in 2021 will be higher than projected last autumn and are expected to exceed the deficit in 2020 for the euro area as a whole (see Chart 1.4, left panel). In addition to existing liquidity support measures, governments started shifting more towards solvency support, for example by replacing government-guaranteed loans with grants or by injecting capital into larger, often state-associated companies. While the shift towards solvency support may be more effective in supporting weaker corporates which increasingly face solvency rather than liquidity problems, it also weighs on fiscal budgets more directly than indirect support measures that constitute contingent liabilities (see Box 2).

Chart 1.4

Fiscal deficits remain large due to pandemic-related expenses, but gross interest payments benefit from the low interest rate environment

Source: European Commission (annual macroeconomic database (AMECO)).

Notes: Left chart: the solid line depicts the 3% fiscal deficit threshold which delineates excessive government deficits according to the Maastricht Treaty. Right chart: consolidated debt and interest payments refer to the general government of the 19 euro area countries.

Extending the general escape clause of the Stability and Growth Pact until the end of 2022 could pre-empt a premature fiscal tightening. Current projections indicate that, due to the economic fallout from the pandemic, governments will continue to run up considerable fiscal deficits in 2022. As the deficits in more than half of the euro area countries are projected to exceed the 3% criterion in 2022, deactivating the escape clause at the end of 2021 might trigger a premature fiscal tightening in 2022. Extending the use of the clause this year already gives governments greater certainty about fiscal space going forward, which reduces the risk of an expectations-driven adverse spiral of reduced fiscal support, tighter corporate financing conditions and a further contraction in economic activity (see Box 4). At the same time, a strong rebound in economic activity would alleviate the need for additional fiscal support and thereby cushion the impact of already reinstating the Stability and Growth Pact rules in 2022.In addition, some stabilisation measures may be phased out as the economy recovers without a major contractionary impact.

Even so, the recent increase in sovereign debt will have less of an impact on fiscal budgets than would have been the case in previous crises. The steady decline in government bond yields has reduced the average gross interest payments of euro area sovereigns despite higher debt-to-GDP ratios than in 2009 (see Chart 1.4, right panel). Aside from this effect, lower interest rates also imply that gross interest payments are less sensitive to changes in debt-to-GDP ratios over time. In 2009, a country with a debt-to-GDP ratio that was 10 percentage points higher on average faced gross interest payments that were 0.4 percentage points higher. That elasticity has shrunk by half since 2009, to 0.2 percentage points. As a consequence, increases in sovereign debt levels due to unexpected events such as the pandemic impose a smaller burden on fiscal budgets, which implies that sovereign balance sheets are more resilient to exogenous shocks than at the time of the global financial crisis. Nevertheless, a sustained rise in sovereign bond yields could raise refinancing costs for governments, which would have a negative effect on sovereign debt sustainability in the medium to long run.

Chart 1.5

Low interest rates and longer maturities alleviate the fiscal footprint of higher sovereign debt

Source: Government Finance Statistics (ECB).

Notes: Left chart: cumulative net issuance refers to the cumulative issuance of government debt securities since February 2020 net of redemptions. Right chart: the calculation of the debt service ratio follows the methodology in Drehmann, M. and Juselius, M., “Do Debt Service Costs Affect Macroeconomic and Financial Stability?”, BIS Quarterly Review, Bank for International Settlements, September 2012. The decomposition is based on changes in annual data.

Governments locked in low interest rates in the second half of 2020 and early 2021 by issuing longer maturity debt, thus reducing rollover risk. Between December 2019 and March 2021, average sovereign bond yields declined by 43 basis points in the euro area, supported by accommodative monetary policy. Following an initial surge in short-term debt issuance last spring, governments locked in these favourable financing conditions by shifting their net issuance towards longer-term debt, in particular bonds with maturities of more than five years (see Chart 1.5, left panel and Chapter 2). This has not been affected so far by the recent rise in sovereign bond yields. Accordingly, the average residual maturity of sovereign debt increased by four months between May 2020 and March 2021.

Low interest rates coupled with longer maturities partially offset the adverse impact of higher debt levels on debt service ratios. The large increase in sovereign debt-to-GDP ratios in 2020 increased the debt service ratio[2] relative to GDP for all euro area countries (see Chart 1.5, right panel). At the same time, longer maturities and to a lesser extent lower rates alleviated the increase in debt service ratios for sovereigns, especially in countries where debt-to-GDP ratios have increased significantly. In addition, approximately 35% of the increase in the euro area debt-to-GDP ratio is driven by the drop in GDP. As the economy recovers, this denominator effect will subside, further easing the debt service ratio and the rollover risk of sovereign debt. In addition, governments continue to hold sizeable deposits with the Eurosystem, which further cushions short-term debt servicing needs.

The effectiveness of the EU recovery package is constrained by countries’ absorption capacity and depends on the productive use of the funds. The €750 billion Next Generation EU (NGEU) package can complement national fiscal support measures in the coming years and help sustain the recovery without national budgets being directly negatively affected.[3] However, historical absorption rates of structural EU funds show that Member States would need to absorb the NGEU funds at an unprecedented pace to make full use of the package (see Chart 1.6, left panel).[4] Based on the absorption rates of year 6 in the 2007-13 multiannual financial framework (MFF), up to 55% of the more than €300 billion in grants contained in the NGEU Recovery and Resilience Facility (RRF) may remain unused (see Chart 1.6, right panel).[5] The lack of absorption capacity in the worst affected countries in particular may impede the disbursement of the NGEU funds, which could further exacerbate the cross-country divergence following the pandemic and potentially spur refragmentation pressures in sovereign bond markets. In addition, the need to absorb NGEU funds quickly may compromise the efficient and productive use of those funds.

Chart 1.6

Limited absorption capacity at national level may inhibit the take-up and effectiveness of NGEU funds

Sources: European Commission and ECB staff calculations based on Darvas, Z., “Will European Union countries be able to absorb and spend well the bloc’s recovery funding?”, Bruegel Blog, 24 September 2020.

Notes: Year 1 is the first year of the respective programme, i.e. 2007 for the 2007-13 MFF, 2014 for the 2014-20 MFF and 2021 for NGEU. The 2007-13 MFF covers the Cohesion Fund, European Regional Development Fund and European Social Fund, while the latter is excluded in the 2014-20 MFF. The MFF payout rate is the share of the total amount committed to a Member State in the EU budget that has been paid out by the Commission. The MFF-related calculations cover euro area countries only (unweighted average). The NGEU grant profile shows the disbursements expected by the Commission as at July 2020. Right panel: the volumes only refer to the grants component of the RRF and absorption rates are based on the absorption of MFF funds in year 6 of the MFF period 2007-13.

While favourable financing conditions mitigate short-term risks in the public sector, the continued need for fiscal support poses medium-term risks. Although financing conditions have limited the impact of increased sovereign debt levels on fiscal budgets and debt service costs, the pandemic continues to take a substantial toll on fiscal budgets. The need to extend existing support measures and retain automatic stabilisers will keep fiscal budgets tightly linked to the evolution of the pandemic. In addition, the adverse impact of continued containment measures on corporate balance sheets increases the risk that contingent liabilities will materialise and further strain public budgets (see Box 2). Finally, a sudden rise in interest rates could raise concerns about the sustainability of sovereign debt over the medium term, although the impact on sovereigns’ debt service needs would be alleviated by the extended average maturity of sovereign debt portfolios.

Box 2

Contingent liabilities: past materialisations and present risks

Fiscal policy support has mitigated financial stability risks during the pandemic, but the vulnerabilities arising from contingent liabilities have increased for euro area sovereigns. National policy responses to support households and firms during the pandemic directly increased the aggregate euro area general government debt-to-GDP level by around 14 percentage points to around 100% of GDP in 2020. Additionally, public guarantee schemes that were introduced in 2020 constitute sizeable contingent liabilities for governments in most euro area countries, adding to the stock of both existing government guarantees and other implicit contingent liabilities, which reinforces concerns about the emergence of an adverse sovereign-bank-corporate nexus. Against this backdrop, this box presents historical evidence from contingent liability materialisations, investigates their commonalities and differences with the situation under the current pandemic-induced shock and assesses the ensuing risk for sovereigns.

More1.3 Aggregate household resilience masks uneven impact of the pandemic

Households’ economic sentiment has improved on hopes of a swift economic recovery, although uncertainty about employment lingers. Survey-based measures of economic confidence started to improve at the end of 2020 when the vaccine roll-out began (see Chart 1.7, left panel). Despite the overall improvement in sentiment, forward-looking measures of unemployment continue to signal a deterioration in employment prospects. The euro area aggregate sentiment masks considerable differences between euro area countries, reflecting the uneven impact of the pandemic on households across the euro area. Households that report the largest deterioration in their financial situation over the last year also show the highest unemployment expectations for the coming 12 months, leaving them in a vulnerable position when support measures are scaled back (see Chart 1.7, right panel).

Chart 1.7

Sentiment improved on the prospects for a vaccine, but unemployment expectations remain high

Sources: ECB, European Commission and Hale et al.

Notes: Left panel: “Stringency” is presented using an inverted scale, i.e. an increase (decrease) in the indicator corresponds to more (less) stringent policy to contain the coronavirus. For more information see the notes to chart 1.1, left panel. Right panel: “Unemployment expectations” reflects consumer expectations for the number of people who will lose their jobs over the next 12 months. “Financial situation” reflects how households score the change in their financial situation over the last 12 months on a five-point scale. A negative score reflects a deterioration in their perceived financial situation. Bubble size reflects the household debt-to-disposable income ratio in the fourth quarter of 2020 or the latest available figure for the household debt-to-disposable income ratio.

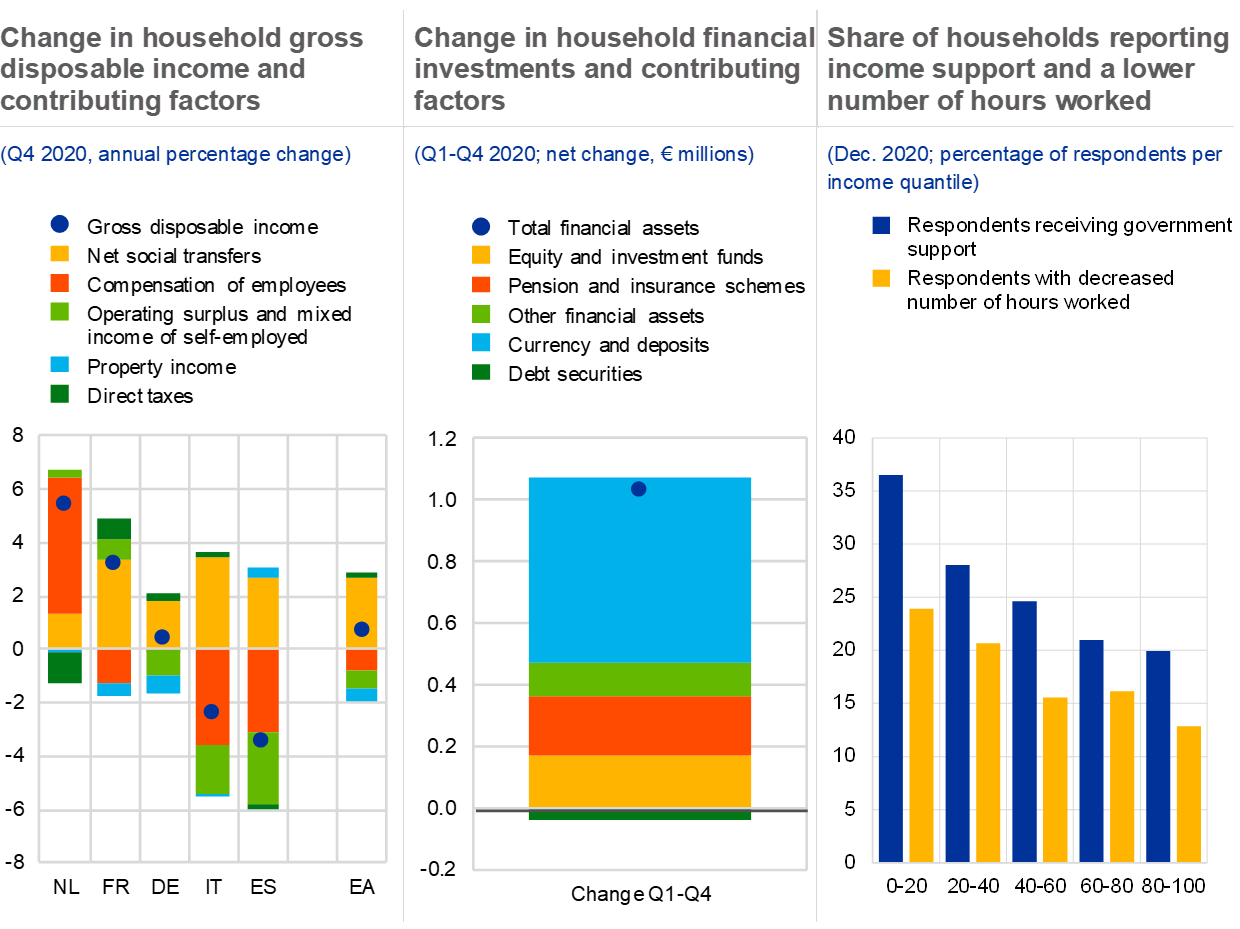

Cushioned household income, excess savings and record high net worth have increased the overall financial resilience of households. Despite recovering from the initial shock of the pandemic, disposable income remains reliant on government support in the form of higher net social transfers (see Chart 1.8, left panel). Moreover, households saved a significant amount of their income as containment measures limited spending on durable goods.[6] Cumulative excess savings compared to the pre-pandemic savings rate stood at around 4% of GDP in the fourth quarter of 2020. Whether pent-up demand will translate into higher future consumption remains uncertain, despite a large share of the excess savings ending up in deposit accounts (see Chart 1.8, middle panel). Excess savings are likely held by higher-income households, which have a lower marginal propensity to consume. Finally, robust house price growth and recovering stock prices continued to support net wealth, causing this metric to surge to 754% of disposable income in 2020 (see Section 1.5).

Chart 1.8

Household income gains flowed into deposit accounts and the stock market as containment measures reduced opportunities to consume

Sources: ECB, Eurostat, ECB Consumer Expectations Survey (CES) – December 2020 wave.

Note: Right panel: all reported numbers are aggregated using individual household weights. Euro area average reflects Belgium, France, Germany, Italy, the Netherlands and Spain.

The increase in aggregate household financial wealth masks considerable differences across countries and income groups. Low-income individuals and countries that already exhibited slow economic growth before the pandemic are affected disproportionately. For this group of households, dependence on policy support measures remains high (see Chart 1.8, right panel). Moreover, there are indications of tighter access to credit combined with cliff effects on their expenditure stemming from the phasing out of moratoria and other economic support policies. Strains on this group of households are likely to intensify if support is dialled back prematurely, resulting in lower consumption and a lower debt service capacity.

Household borrowing varies significantly across different types of credit (see Chart 1.9, left panel). Growth in aggregate bank lending to households stabilised at 3% from the start of 2020, mainly on account of a 5% increase in lending for house purchase. Consumer credit declined by 2%, reflecting the ongoing impact of the tighter COVID-19 restrictions on consumer confidence and demand for durable goods. Going forward, a further moderation in banks’ risk perceptions towards households might support looser credit standards and boost consumption when lockdown measures are scaled back and the economy fully reopens (see Chart 1.9, middle panel).

Chart 1.9

Credit for consumption declined as households had less opportunity to spend

Sources: ECB and Eurostat.

Notes: Left panel: “Loans for other purposes” mainly reflects lending to sole proprietors. “Loans for house purchase” represents 77% of total lending, “Consumer credit” 12% and “Loans for other purposes” 11%. Lending figures are not corrected for securitised loans. Middle panel: “Risk perceptions” is the unweighted average of BLS survey questions on the “general economic situation and outlook”, “housing market prospects, including expected house price developments” and “borrower’s creditworthiness”.

Government schemes and record low debt servicing costs have helped to make household debt more sustainable. So far, the pandemic has had a relatively modest impact on household debt ratios, as disposable income increased while spending opportunities were limited during lockdowns. As a result, nominal household debt increased at a slower pace in the first half of 2020 compared to the pre-pandemic path (see Chart 1.9, right panel), while the debt-to-liquid assets ratio declined to 76% in the fourth of 2020. In addition, very low interest rates have driven debt servicing costs down to all-time lows, with interest payments as a share of disposable income falling to 2.2%. Households increasingly favoured fixed rate mortgages in new annual credit flows over variable rate alternatives, further contributing to lower overall vulnerability. As a result, the share of fixed rate mortgages had increased to 59% in March 2021 compared to just 47% in March 2016.

Overall, financial stability risks stemming from the household sector have been less pronounced than previously anticipated. With stronger balance sheets, robust net wealth and record low debt servicing costs, households have built up some capacity to weather economic headwinds. However, lower-income workers have not generally benefited from mitigating factors in the form of higher financial wealth, leaving them in a potentially vulnerable position when policy support is scaled back. In addition, household resilience remains highly contingent on the extent to which corporate insolvencies rise, as this could translate into significantly higher unemployment. Whether these risks materialise will depend on the ability of governments to keep supporting the households that have been hardest hit by the pandemic, especially in those countries where the take-up of policy support is substantial, residential properties are overvalued and debt levels are elevated.

1.4 Corporate solvency risks on the rise

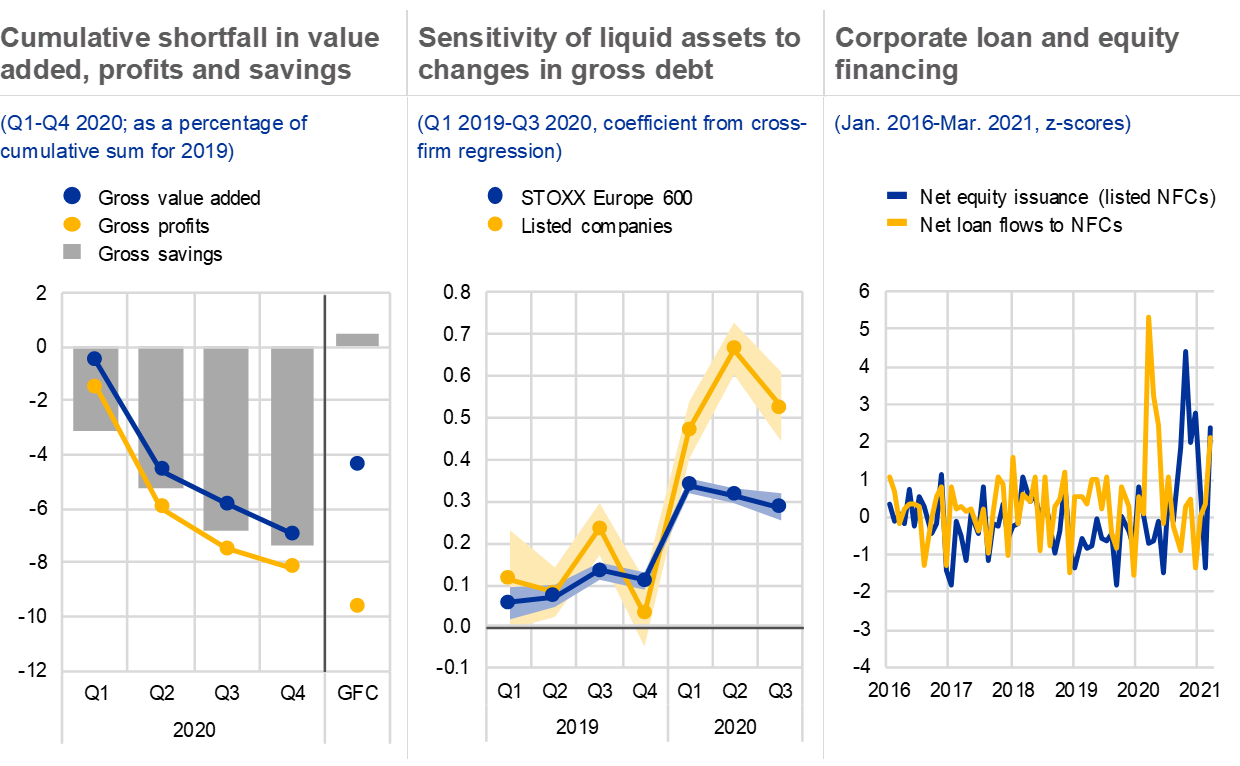

Weak revenues and low profit margins continue to weigh on corporate profits, gradually raising the pressure on corporate solvency. Similar to previous recessions, gross corporate profits declined more than gross value added in 2020, as squeezed profit margins added to the fall in corporate revenues (see Chart 1.10, left panel). Although both profits and revenues were more resilient in the second wave than during the initial phase of the pandemic, their continued decline added to the total shortfall compared with 2019 levels. In total, corporate profits in 2020 were 8.1% below gross profits in 2019. Consequently, retained earnings (measured by gross savings) dropped substantially, unlike in the global financial crisis when they recovered during the first year of the recession. This sharp and persistent drop in corporate savings limits the scope for new investment going forward, although firms may use available cash buffers to support capital accumulation.

Chart 1.10

Falling profits weigh on liquidity and leverage ratios at the most vulnerable firms

Sources: ECB and Eurostat (quarterly sectoral accounts, securities issues statistics); middle panel: Refinitiv and ECB calculations.

Notes: Middle panel: data do not include unlisted firms and are therefore likely to be biased towards larger corporates. Right panel: both time series are z-scores based on the respective sample from January 2012 to January 2021. Note that net equity issuance refers to listed non-financial corporates whereas net loan flows covers all non-financial corporates.

Aggregate liquidity and capital buffers conceal a divergence across corporates, as risks rise for cash-strapped and overindebted firms. On aggregate, the considerable increase in gross debt has so far largely been offset by a similar rise in corporate holdings of liquid assets. Granular data for listed firms confirm that corporates took on more debt to build up precautionary liquidity buffers as the correlation between changes in gross debt and changes in cash buffers across firms increased (see Chart 1.10, middle panel). However, this effect is particularly prominent for large listed corporates whereas SMEs, which were more heavily affected by the pandemic and are less likely to have access to market-based funding, face more severe liquidity challenges. The concentration of liquidity risk among the most vulnerable corporates implies that a sudden tightening of financing conditions or a protracted economic recovery could have more severe consequences for financial stability than the aggregate picture suggests. In addition, liquidity problems increasingly morph into solvency issues – while the first wave of the pandemic was characterised by bond issuance and bank borrowing to meet liquidity needs, firms have recently issued more equity (see Chart 1.10, right panel). Among listed firms, however, equity issuance has been concentrated in a few firms, especially in the technology sector, which tend to have benefited from the pandemic.

More recently, corporate credit growth has slowed, reflecting both corporates deferring investment and banks tightening lending conditions. In the second half of 2020, demand for bank loans slowed abruptly as bank lending conditions tightened and the need to bridge working capital needs subsided (see Chart 1.11, left panel), especially in the worst affected sector, services. Besides the drop in demand for liquidity and the more cautious risk perceptions of banks, the slowdown in bank lending to corporates also reflects the reduced willingness of firms to invest in fixed capital while uncertainty remains about the timing and pace of the economic recovery. However, the subdued investment activity could also indicate a more structural pessimism about the viability of certain business models or the limited scope for new investments amid elevated debt levels. That in turn would have a more lasting impact on the economic recovery and corporate balance sheets. Moreover, building up liquidity buffers in the early stages of the pandemic has shielded some firms from revenue shortfalls and reduced the subsequent need for additional external financing.

Government-guaranteed loans may have become less effective in supporting corporate financing conditions. Following the large take-up of guaranteed loans in the second quarter of 2020, the demand for such loans has dropped sharply in tandem with the slowdown in new bank loans to corporates in the second half of 2020 (see Chart 1.11, middle panel). Looking ahead, the take-up of government-guaranteed loans is likely to fall further, as guarantees appear to have become less effective in supporting corporate financing conditions. Throughout 2020, credit standards eased considerably for guaranteed loans while tightening for non-guaranteed loans (see Chart 1.11, right panel). However, this gap in credit standards between guaranteed and non-guaranteed loans is projected to narrow in the first half of 2021. Also, overindebted corporates may be unwilling to take on additional debt, given the uncertain outlook.

Smaller firms benefited most from government guarantees but are particularly affected by a recent tightening of bank lending conditions. SMEs have been more likely to resort to government-guaranteed loans than larger firms, given their reliance on bank lending and the disproportionate impact of the pandemic on smaller enterprises. They have also been more likely to benefit from the benign effect of guarantees on credit standards, as they faced a sharper tightening of credit conditions for non-guaranteed loans (see Chart 1.11, right panel). The projected tightening of credit standards on guaranteed loans therefore disproportionately affects SMEs.

Chart 1.11

Corporate loan demand has faded as external financing needs moderated, credit conditions tightened and guarantees became less attractive for SMEs

Sources: ECB bank lending survey and national sources.

Notes: Right panel: the net percentage refers to the difference between the sum of the percentages for “tightened considerably” and “tightened somewhat” and the sum of the percentages for “eased somewhat” and “eased considerably". Data for H1 2021 reflect expectations indicated by banks in the latest round of the bank lending survey.

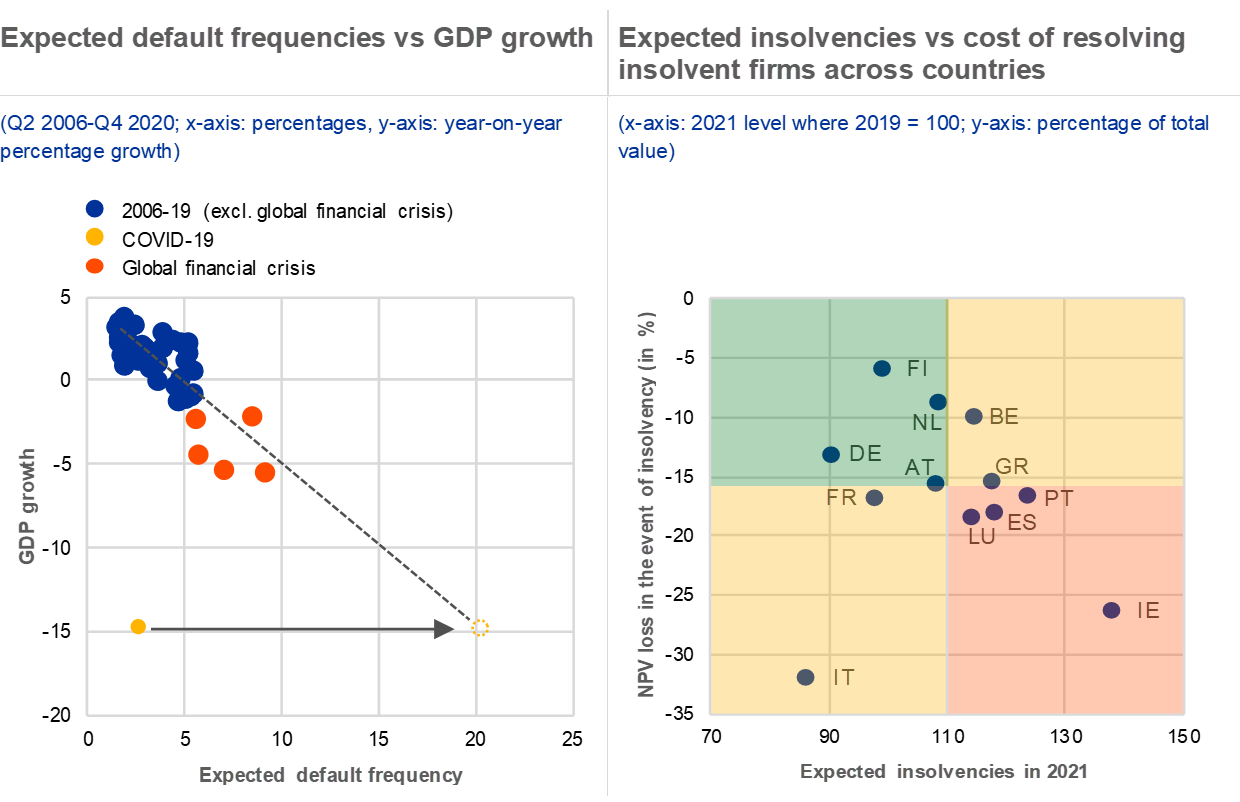

An abrupt increase in bankruptcies could challenge insolvency frameworks and impede the efficient reallocation of resources. Despite the unprecedented fall in corporate revenues and profits, bankruptcies in the euro area decreased by approximately 20% in 2020 relative to 2019 levels as public authorities provided policy support and in some cases suspended mandatory insolvency filings. Dealing with such a backlog of delayed bankruptcies would prove a challenge for judicial systems even in normal times. Although corporate solvency is likely to be more resilient than historical comparisons suggest, given the relatively swift recovery and the sizeable policy support, the number of insolvencies-in-waiting could still be higher than the current expected default frequency suggests (see Chart 1.12, left panel). Once support measures end, bankruptcy courts could therefore see an abrupt increase in insolvency filings, which could lead to the legal system becoming congested and insolvent firms taking longer to be resolved. That in turn could result in an inefficient and delayed reallocation of resources to more viable businesses, with adverse macroeconomic consequences in the medium term. Public authorities should therefore ensure that insolvency frameworks are sufficiently resourced to deal with a higher number of corporate insolvencies (see Chart 1.12, right panel).

Chart 1.12

Backlog of insolvencies could lead to challenges in countries with inefficient insolvency frameworks

Sources: Moody’s Analytics and Eurostat; right panel: EBA and Allianz Euler Hermes (see notes to Chart 4 in the Overview for details).

Notes: Left panel: the yellow dotted circle shows the counterfactual expected default frequency (EDF) based on the historical relation between GDP growth and EDFs for the second quarter of 2020. Right panel: expected insolvencies are relative to 2019 levels, based on projections provided by Euler Hermes in December 2020. The net present value (NPV) loss associated with insolvencies encompasses the direct administrative costs and the time until the insolvency is resolved. It does not contain the additional NPV loss if the underlying loan is sold to an investor.

Given the uncertain outlook for the viability of business models, targeting policy support towards viable firms remains challenging. Ideally, the broad-based liquidity support measures that shaped the early phase of the pandemic would be superseded by more targeted measures that help viable firms remain solvent. However, assessing corporate viability remains challenging in the light of the uncertain economic outlook and the post-pandemic prospects of different business models. While broad-based measures may lead to some misallocation of resources to non-viable firms (see Special Feature A), the alternative of withdrawing support to viable firms too early may have even more adverse consequences.

1.5 Euro area property market cycles diverge further

Euro area residential real estate (RRE) prices continued rising throughout the fourth quarter of 2020. At the euro area level, nominal house prices increased by 5.8% in the last quarter of 2020 (see Chart 1.13, left panel). While on aggregate prices continued to trend upwards in the euro area, growth rates varied widely across countries (see Chart 1.13, middle panel). The overall resilience observed in housing markets reflects several factors. First, household income has largely recovered as a result of the continued policy support and a rebound in economic activity. Second, the low interest rate environment and elevated macro uncertainty continue to put a floor under demand, as housing is perceived as a safe investment. Third, subdued construction activity in the second half of 2020 weighed on housing supply, adding upward pressure on prices, especially in markets with already tight housing supply.

Chart 1.13

House price growth remains buoyant, but risks of a price correction remain elevated, especially for markets with high overvaluation

Sources: ECB and ECB calculations.

Notes: Middle panel: the valuation estimate is the simple average of the price-to-income ratio and an estimated Bayesian vector autoregression (BVAR) model. For details of the methodology, see Box 3 in Financial Stability Review, ECB, June 2011, and Box 3 in Financial Stability Review, ECB, November 2015. Overall, estimates from the valuation models are subject to considerable uncertainty and should be interpreted with caution. Alternative valuation measures can point to lower/higher estimates of overvaluation. Right panel: results from a house price-at-risk model based on a panel quantile regression on a sample of 19 euro area countries over the period from the first quarter of 1999 to the first quarter of 2021. Explanatory variables: lag of real house price growth, overvaluation (average of deviation of house price-to-income ratio from long-term average and econometric model), systemic risk indicator, consumer confidence indicator, financial market conditions indicator capturing stock price growth and volatility, government bond spread, slope of yield curve, euro area non-financial corporate bond spread, and an interaction of overvaluation and a financial conditions index.

A combination of buoyant house price growth and the uncertain macro backdrop kept measures of overvaluation elevated. Moreover, house price growth during the pandemic has generally been higher for those countries that were already experiencing pronounced estimated overvaluation prior to the pandemic (see Chart 1.13, middle panel). While providing a consistent set of benchmarks across countries, measures for overvaluation are surrounded by significant uncertainty and may be sensitive to country-level specificities, such as tax treatment or structural property market characteristics. In addition to elevated valuation measures, risks related to household indebtedness remain high for some countries, as credit for house purchase has continued to increase (see Section 1.3). This adds to the already elevated vulnerabilities that had accumulated in some euro area countries before the pandemic started.

Estimates of downside risk to house prices signal an expected slowdown of price growth in the coming year (see Chart 1.13, right panel). Despite high measures of overvaluation in some euro area countries, house price growth is expected to moderate, but prices are not expected to decline in the coming year. This expectation mainly reflects the improved economic outlook and overall more robust household balance sheets. Moreover, results from the bank lending survey also indicate credit standards for loans to households for house purchase eased slightly in net terms in the first quarter of 2021, possibly further supporting demand. However, future RRE price developments remain highly dependent on the recovery path and the ability of policymakers to prevent cliff edges by not abruptly ending support measures, especially given much of the resilience observed in household balance sheets is a direct result of policy support measures (see Section 1.3).

Chart 1.14

Prime commercial real estate prices declined as the market entered a downturn and financing conditions deteriorated

Sources: ECB, ECB calculations and RICS Global Commercial Property Monitor.

Note: The RICS Global Commercial Property Monitor is a quarterly guide to the trends in the commercial property investment and occupier markets. Respondents are asked to compare conditions over the latest three months with the previous three months and to give their views as to the outlook.

In contrast to the residential market, the pandemic sparked a price correction in the commercial real estate (CRE) market. Prices for prime CRE declined in the fourth quarter of 2020, albeit with large difference between those sectors hit hardest by the pandemic (retail) and those less affected (office) (see Overview chapter). Moreover, market intelligence suggests that prices in prime locations might also have been impacted less, as high-quality assets are typically easier to adapt to changing demand. Survey data indicate that the CRE market entered a downturn in the second quarter of 2020. Moreover, rising overvaluation in recent years has left room for a substantial price correction, as a majority of investors indicate that valuations have not bottomed out yet (see Chart 1.14, left panel). Also, activity remained at levels around half of the long-run average, potentially masking a further decline in property prices.

A sharper CRE market correction could have implications for bank balance sheets and introduce negative economic feedback loops. A further decline in CRE prices could feed through to the financial system via increased credit risk, decreased collateral values and losses on direct holdings. Bank lending to the CRE segment accounts for 7% of exposure to the non-financial private sector in the euro area, although levels vary substantially across countries. A significant drop in CRE prices could result in lower investment and economic activity by non-financial corporates, as CRE is often used as collateral to obtain finance. Survey data show that over half of survey participants have seen financing conditions deteriorate each quarter since the outbreak of the pandemic (see Chart 1.14, right panel). In addition, a further price correction may also spark procyclical behaviour within the financial system when risk exposure is reduced, loan loss provisions fall, and lending standards tighten. Moreover, a combination of low market liquidity and high redemption pressure on CRE investment funds could amplify the price decline and lead to fire sales, further increasing negative feedback loops.

Risks to financial stability stemming from real estate markets remain elevated. A sharper than expected decline in CRE valuations might set off negative economic feedback loops, while the RRE market might prove vulnerable to a withdrawal of policy support measures. Against this background, the financial sector may be exposed to the risk of corrections in the real estate market, especially in those countries where debt levels are elevated and policy support measures contribute significantly to household income.

2 Financial markets

2.1 Partial spillover of risks from rising US rates

A rise in US government bond yields led global sovereign bond yields higher, with euro area yield curves also steepening mildly. Rising US yields in recent months reflected the combination of a substantial fiscal stimulus package and optimism around vaccine roll-outs. The bond market sell-off also spilled over to some degree to other advanced economies, resulting in a mild steepening of the euro area GDP-weighted yield curve (see Chart 2.1, left panel). 2021 has seen the largest upward move in the ten-year US Treasury yield since the “taper tantrum” in 2013. However, the drivers of the yield change in 2021 appear more benign than in 2013, as a much smaller share relates to uncertainty on the outlook for US monetary policy (see Chart 2.1, middle panel). Foreign spillovers also explain a structurally increasing share of the euro area term premium (see Chart 2.1 right panel). Excessive increases in yields not motivated by domestic fundamentals threaten to unduly tighten financial conditions, if a rise in US yields has a large spillover effect on the euro area.

Chart 2.1

Steeper yield curves in advanced economies with structurally increasing spillovers

Sources: ECB, Refinitiv, Haver Analytics and ECB calculations.

Notes: Left panel: “Range” refers to advanced economies including Australia, Denmark, Canada, Japan, Norway, Sweden, the euro area, the United Kingdom, the United States and Switzerland. Euro area aggregate is based on GDP shares. Middle panel: the decomposition is derived from a structural Bayesian vector autoregression (BVAR) model with sign and magnitude restrictions, Dieppe, A., Legrand, R. and van Roye, B., “The BEAR toolbox”, Working Paper Series, No 1934, ECB, July 2016, and refers to May-June 2013. Right panel: the estimation builds on the methodology proposed by Nyholm K., “US-euro area term structure spillovers, implications for central banks”, Working Paper Series, No 1980, ECB, November 2016, and Diebold, F.X. and Yilmaz, K., “Measuring Financial Asset Return and Volatility Spillovers, with Application to Global Equity Markets”, The Economic Journal, Vol. 119, Issue 534, January 2009, pp. 158-171, and Diebold, F.X. and Yilmaz, K., “Trans-Atlantic Equity Volatility Connectedness: U.S. and European Financial Institutions, 2004-2014”, Journal of Financial Econometrics, Vol. 14, Issue 1, Winter 2016, pp. 81-127. A 250-day rolling window VAR(2) including term premia and expected short-term rates for G10 + Australia markets is estimated, where term premia and expected short-term rates are the averages of dynamic Nelson-Siegel, dynamic Svensson-Soderlind and rotated dynamic Nelson-Siegel model estimates. Generalised impulse response functions (Pesaran, H.H. and Shin, Y., “Generalized impulse response analysis in linear multivariate models”, Economics Letters, Vol. 58, Issue 1, January 1998, pp. 17-29) allowing for correlated shocks are used to estimate the variance decomposition of the forecast error with a ten-day horizon, which in turn is used to compute spillover indices.

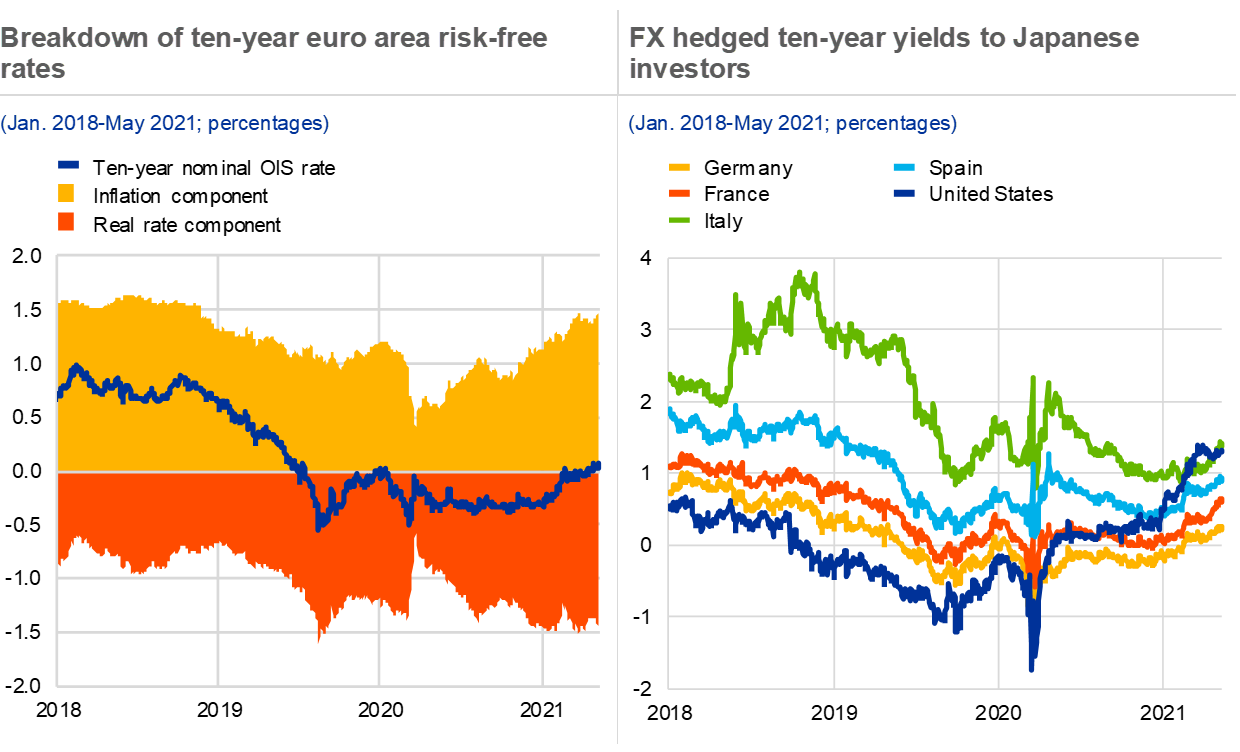

Euro area risk-free rates have risen only mildly, partly reflecting continued emphasis on accommodative monetary policy. Ten-year euro area risk-free rates moved back to pre-pandemic levels as the inflation component of risk-free rates increased to its highest level since the end of 2018 (see Chart 2.2, left panel). This reflects an improved economic outlook and a reassessment by investors of the balance of risks around the inflation outlook. In December 2020, alongside other monetary policy measures the Governing Council decided to recalibrate TLTRO III conditions and also to expand the pandemic emergency purchase programme envelope, where bond purchases were to be significantly stepped up in the second quarter of 2021.[7] The monetary policy measures help preserve favourable financing conditions, which are vital as countries take steps to re-open their economies.

The strong rise in US yields compared with euro area yields may affect global capital flows in the medium term. In recent years, FX hedged yields on ten-year US Treasuries have been relatively unattractive. However, the rise in US Treasury yields, which in February was reinforced by the largest foreign outflows since April 2020, has made this asset class more appealing. For Japanese investors, US Treasuries currently offer a higher FX hedged yield and a better credit rating than some of the largest euro area sovereign bond markets (see Chart 2.2, right panel).[8] This change could generate wider shifts in investor and capital flows and may lessen overseas demand for euro area sovereign bonds.

Chart 2.2

Mildly higher euro area risk-free rates and shift in attractiveness of FX hedged yields

Sources: Refinitiv, Bloomberg Finance L.P. and ECB calculation.

Notes: Left panel: the real rate is calculated by subtracting the inflation-linked swap (ILS) rate from the nominal overnight index swap (OIS) rate. Right panel: ten-year sovereign bond yield less the three-month JPY FX hedge cost.