Annual Accounts 2021

Key figures

1 Management report

1.1 Purpose of the ECB’s management report

The management report[1] is an integral part of the ECB’s Annual Accounts and is designed to provide readers with contextual information related to the financial statements.[2] Given that the ECB’s activities and operations are undertaken in support of its policy objectives, the ECB’s financial position and result should be viewed in conjunction with its policy actions.

To this end, the management report presents the ECB’s main tasks and activities, as well as their impact on its financial statements. Furthermore, it analyses the main developments in the Balance Sheet and the Profit and Loss Account during the year and includes information on the ECB’s financial resources. Finally, it describes the risk environment in which the ECB operates, providing information on the specific risks to which the ECB is exposed, and the risk management policies used to mitigate risks.

1.2 Main tasks and activities

The ECB is part of the Eurosystem, which comprises, besides the ECB, the 19 national central banks (NCBs) of the Member States of the European Union (EU) whose currency is the euro. The Eurosystem has the primary objective of maintaining price stability.[3] The ECB performs its tasks as described in the Treaty on the Functioning of the European Union[4] and in the Statute of the European System of Central Banks and of the European Central Bank (Statute of the ESCB)[5] (Figure 1). The ECB conducts its activities in order to fulfil its mandate and not with the intention of generating profit.

Figure 1

The ECB’s main tasks

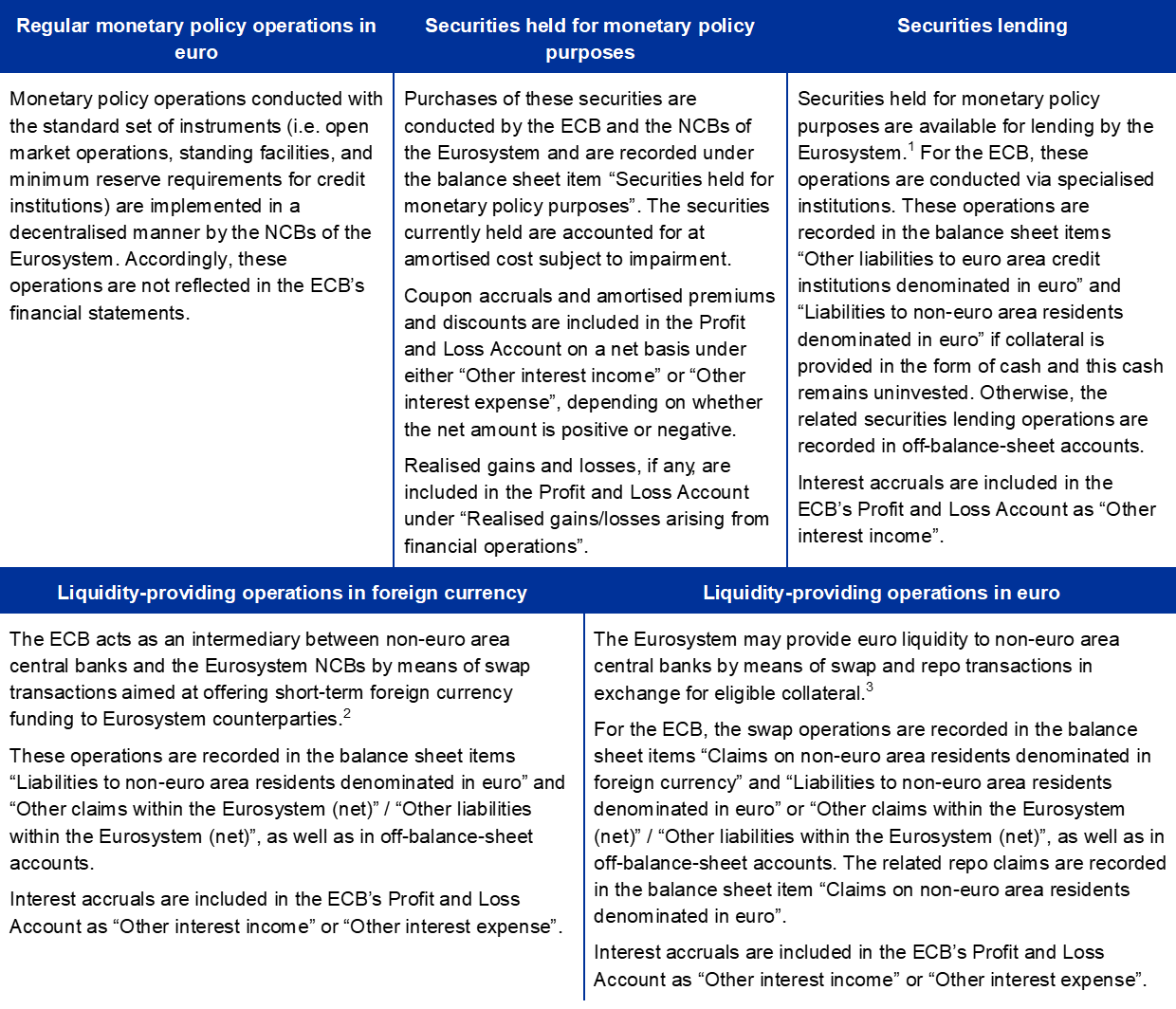

The Eurosystem’s monetary policy operations are recorded in the financial statements of the ECB and of the euro area NCBs, reflecting the principle of decentralised implementation of monetary policy in the Eurosystem. Table 1 below provides an overview of the main operations and functions of the ECB in pursuit of its mandate, and their impact on the ECB’s financial statements.

Table 1

The ECB’s key activities and their impact on its financial statements

Implementation of monetary policy

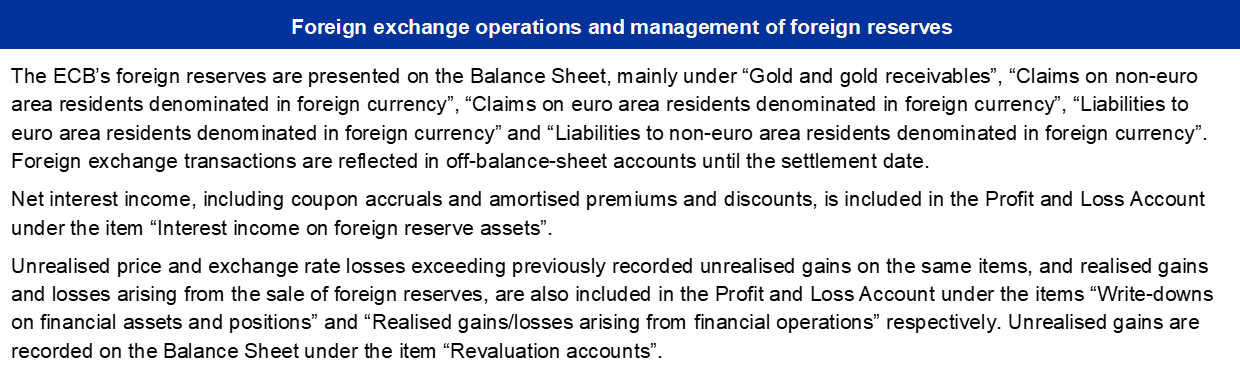

Conduct of foreign exchange operations and management of foreign reserves

Promotion of the smooth operation of payment systems

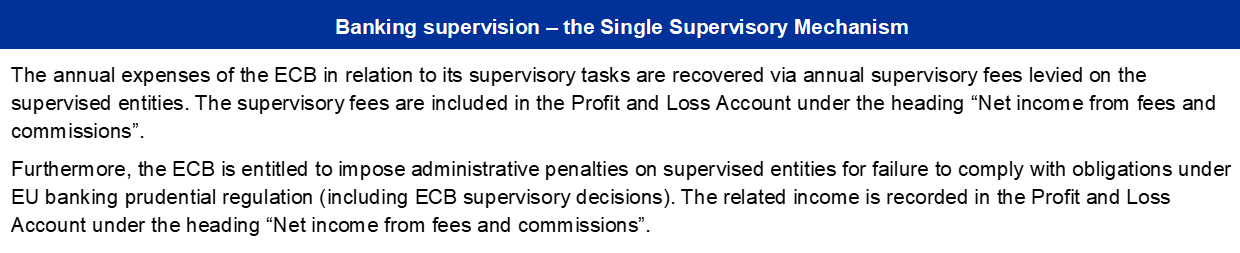

Contribution to the safety and soundness of the banking system and the stability of the financial system

Other

1) Further details on securities lending can be found on the ECB’s website.

2) Further details on the currency swap lines can be found on the ECB’s website.

3) Further details on the Eurosystem’s euro liquidity operations against eligible collateral can be found on the ECB’s website.

4) Further details on TARGET2 can be found on the ECB’s website.

1.3 Financial developments

1.3.1 Balance Sheet

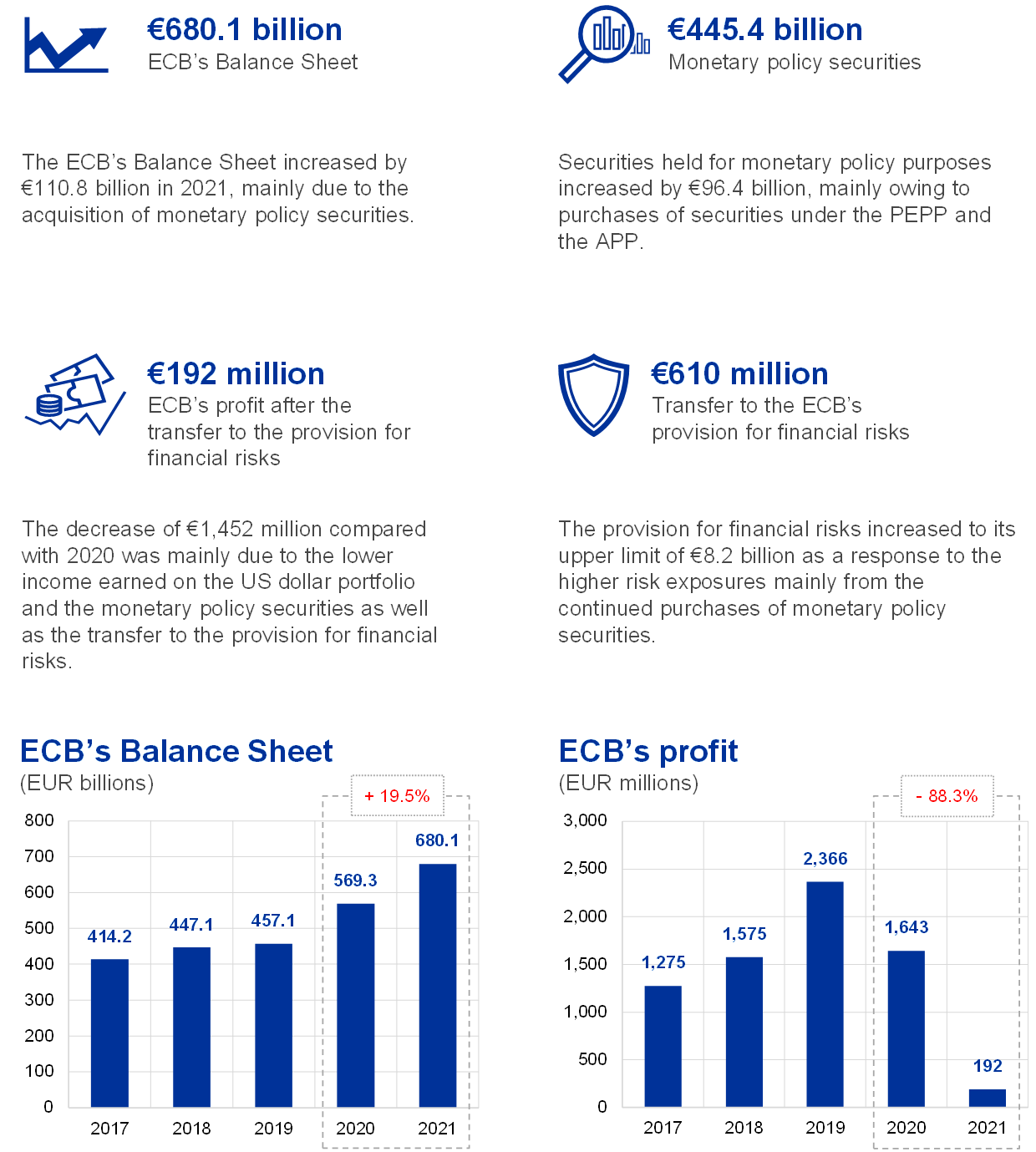

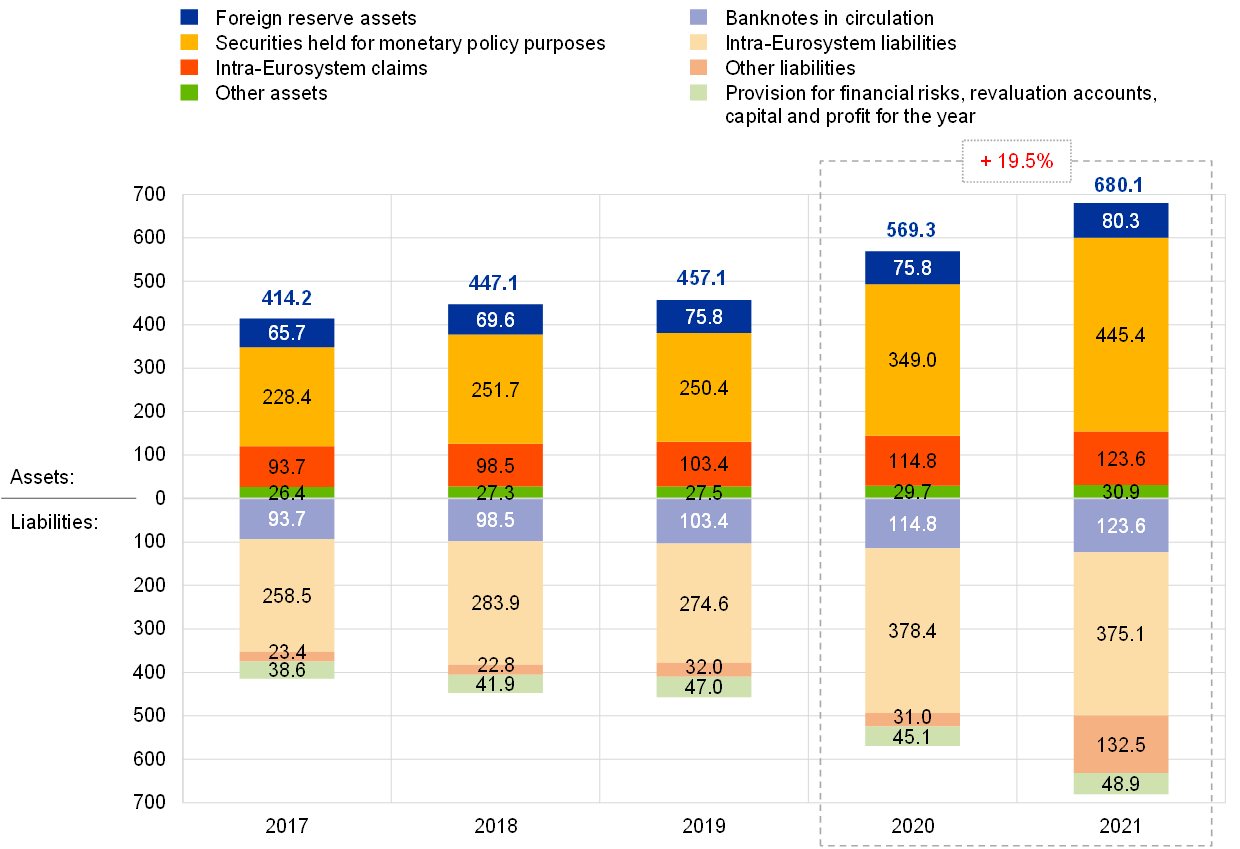

In the period from 2017 to 2021, developments in the ECB’s Balance Sheet were mainly driven by outright purchases of securities by the ECB as part of the implementation of the monetary policy of the Eurosystem (Chart 1). The ECB’s Balance Sheet expanded in 2018, mainly owing to the net acquisition of securities under the asset purchase programme (APP)[6]. Net purchases under this programme ceased in December 2018 and resumed again in November 2019. As a result, the ECB’s Balance Sheet grew more slowly in 2019, and most of this growth stemmed from rises in the market value of the ECB’s foreign reserve assets and in the value of euro banknotes in circulation. In 2020, in order to address the impact of the coronavirus (COVID-19) pandemic, the Governing Council decided on a comprehensive package of monetary policy measures, including the launch of the pandemic emergency purchase programme (PEPP)[7], leading to further balance sheet growth. Net purchases under the APP and the PEPP continued in 2021, increasing still further the size of the ECB’s Balance Sheet.

In 2021 the ECB’s Balance Sheet increased by €110.8 billion to €680.1 billion, mainly owing to the ECB’s share of securities purchases under the PEPP and the APP. These purchases resulted in an increase in securities held for monetary policy purposes, while the cash settlement of these purchases via TARGET2 accounts led to a corresponding increase in intra-Eurosystem liabilities. This increase in intra-Eurosystem liabilities was more than offset by the cash received from the ECB’s non-euro area TARGET2 customers, which also resulted in an increase in other liabilities.

In addition, the rises in the value of euro banknotes in circulation and in the market value of the ECB’s foreign reserve assets also contributed to the growth of the ECB’s Balance Sheet.

Chart 1

Main components of the ECB’s Balance Sheet

(EUR billions)

Source: ECB.

Euro-denominated securities held for monetary policy purposes made up 65% of the ECB’s total assets at the end of 2021. Under this balance sheet item, the ECB holds securities acquired in the context of the Securities Markets Programme (SMP), the three covered bond purchase programmes (CBPP1, CBPP2 and CBPP3), the ABSPP, the PSPP and the PEPP.

In 2021 the ECB, based on the relevant Governing Council decisions, continued its net purchases of securities under the APP and the PEPP, including the reinvestment of principal payments from maturing securities purchased under these programmes. As a result of these purchases, the portfolio of securities held by the ECB for monetary policy purposes increased by €96.4 billion to €445.4 billion (Chart 2), with PEPP purchases accounting for most of this increase. The €1.3 billion decrease in holdings under the SMP, CBPP1 and CBPP2 was due to redemptions.

In December 2021 the Governing Council announced[8] that it would increase net purchases under the APP to a monthly pace of €40 billion in the second quarter and €30 billion in the third quarter of 2022. From October 2022 onwards, net asset purchases will be maintained at a monthly pace of €20 billion for as long as necessary to reinforce the accommodative impact of the ECB’s policy rates, and will end shortly before the Governing Council starts raising the key ECB interest rates. The Governing Council also decided to discontinue net asset purchases under the PEPP at the end of March 2022, but they could be resumed, if necessary, to counter negative shocks related to the pandemic. The Eurosystem will continue reinvesting, in full, the principal payments from maturing securities purchased under the APP and the PEPP in line with the Governing Council decision.

Chart 2

Securities held for monetary policy purposes

(EUR billions)

Source: ECB.

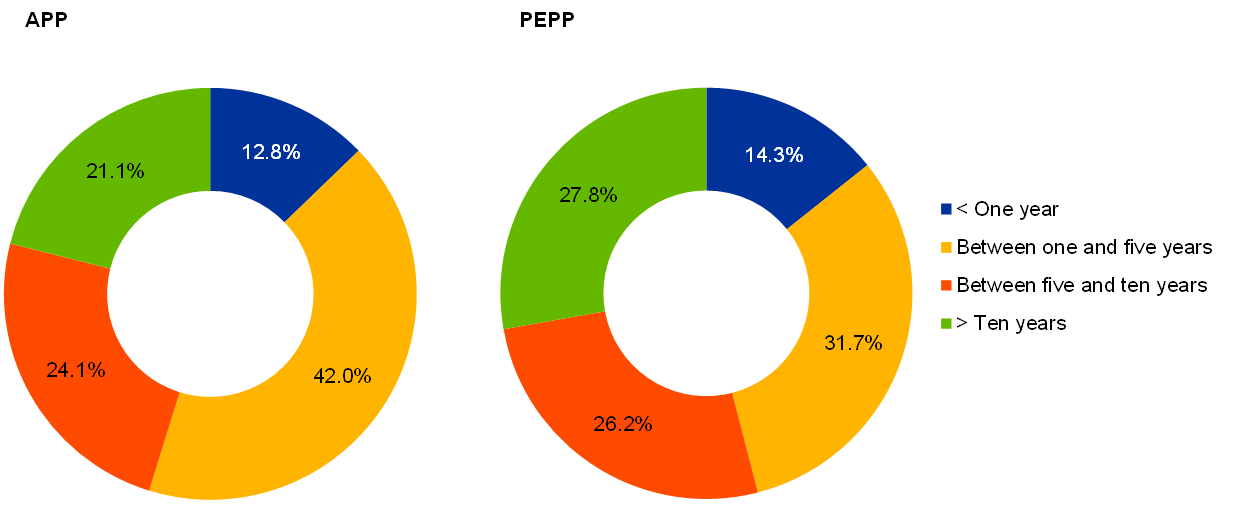

For the active programmes of securities held for monetary policy purposes, namely the APP and the PEPP, securities held by the ECB at the end of 2021 had a diversified maturity profile[9] (Chart 3).

Chart 3

Maturity profile of the APP and the PEPP

Source: ECB.

Note: For asset-backed securities, the maturity profile is based on the weighted average life of the securities rather than the legal maturity date.

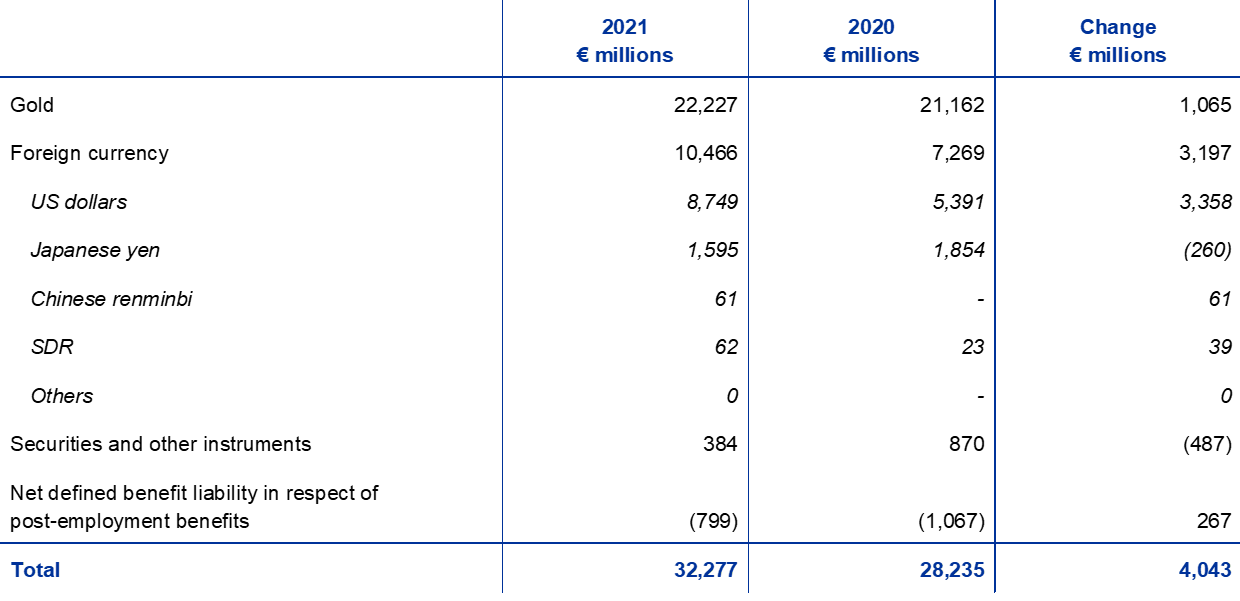

In 2021 the total euro equivalent value of the ECB’s foreign reserve assets, which consist of gold, special drawing rights, US dollars, Japanese yen and Chinese renminbi, increased by €4.5 billion to €80.3 billion.

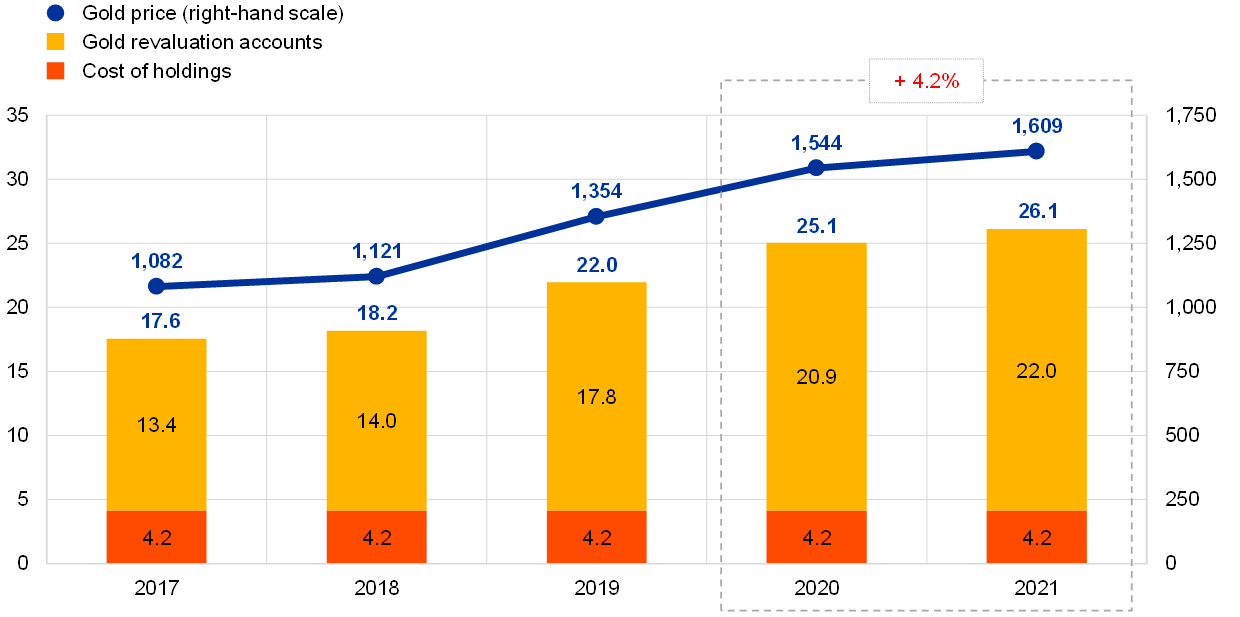

The euro equivalent value of the ECB’s holdings of gold and gold receivables increased by €1.1 billion to €26.1 billion in 2021 (Chart 4) owing to an increase in the market price of gold in euro terms, while the size of these holdings in fine ounces remained unchanged. This increase also led to an equivalent rise in the ECB’s gold revaluation accounts (see Section 1.3.2 “Financial resources”).

Chart 4

Gold holdings and gold prices

(left-hand scale: EUR billions; right-hand scale: euro per fine ounce of gold)

Source: ECB.

Note: “Gold revaluation accounts” does not include the contributions of the central banks of the Members States that joined the euro area after 1 January 1999 to the accumulated gold revaluation accounts of the ECB as at the day prior to their entry into the Eurosystem.

The ECB’s foreign currency holdings[10] of US dollars, Japanese yen and Chinese renminbi increased in euro terms by €2.9 billion to €53.0 billion (Chart 5), mainly owing to the appreciation of the US dollar against the euro. The appreciation of the US dollar is also reflected in higher balances in the ECB’s revaluation accounts (see Section 1.3.2 “Financial resources”).

Chart 5

Foreign currency holdings

(EUR billions)

Source: ECB.

The US dollar continued to be the main component of the ECB’s foreign currency holdings, accounting for approximately 77% of the total at the end of 2021.

The ECB manages the investment of its foreign currency holdings using a three-step approach. First, a strategic benchmark portfolio is designed by the ECB’s risk managers and approved by the Governing Council. Second, the ECB’s portfolio managers design the tactical benchmark portfolio, which is approved by the Executive Board. Third, investment operations are conducted in a decentralised manner by the NCBs on a day-to-day basis.

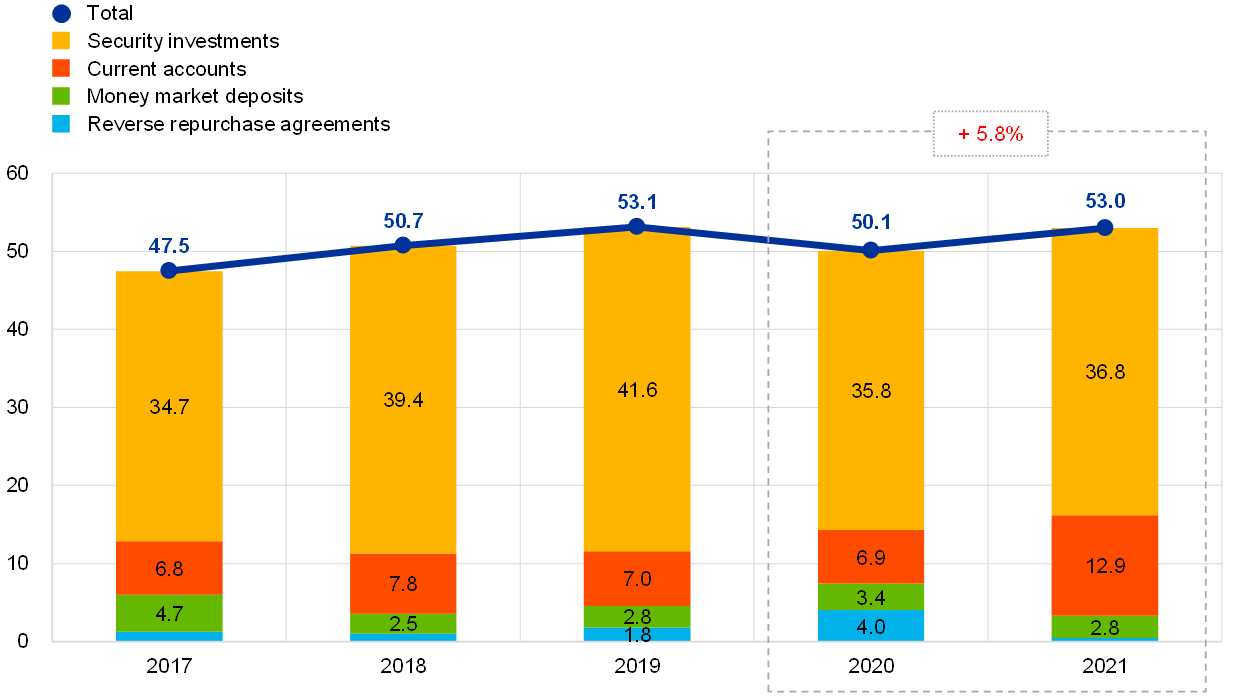

The ECB’s foreign currency holdings are mainly invested in securities and money market deposits or are held in current accounts (Chart 6). Securities in this portfolio are valued at year-end market prices.

Chart 6

Composition of foreign currency investments

(EUR billions)

Source: ECB.

The purpose of the ECB’s foreign currency holdings is to finance potential interventions in the foreign exchange market. For this reason, the ECB’s foreign currency holdings are managed in accordance with three objectives (in order of priority): liquidity, safety and return. Therefore, this portfolio mainly comprises securities with short maturities (Chart 7).

Chart 7

Maturity profile of foreign currency-denominated securities

Source: ECB.

In 2021 the value of the own funds portfolio increased by €0.4 billion to €21.1 billion (Chart 8), mainly owing to the investment of the amounts paid up by the euro area NCBs in 2021 in respect of the first instalment of their increased subscriptions in the ECB’s capital following the withdrawal of the Bank of England from the ESCB (see Section 1.3.2 “Financial resources”). This increase was partially offset, mainly by the decline in the market value of the securities held in the own funds portfolio.

The portfolio mainly consists of euro-denominated securities which are valued at year-end market prices. In 2021 government debt securities accounted for 72% of the total portfolio.

In 2021 the ECB decided to use part of its own funds portfolio to invest in the euro-denominated green bond investment fund for central banks (EUR BISIP G2) launched by the Bank for International Settlements (BIS) in January 2021. This investment complements direct purchases of green bonds in secondary markets. The share of the green investments in the own funds portfolio continued to increase steadily from 3.5% at the end of 2020 to 7.6% at the end of 2021. The ECB plans to further increase this share over the coming years.

Chart 8

The ECB’s own funds portfolio

(EUR billions)

Source: ECB.

The ECB’s own funds portfolio predominantly consists of investments of the ECB’s financial resources, namely its paid-up capital and amounts held in the general reserve fund and the provision for financial risks. Owing to the reinvestment of income proceeds and the valuation of securities at market prices, the own funds portfolio and the aforementioned financial resources do not necessarily correspond in size. The purpose of this portfolio is to provide income to help fund the ECB’s operating expenses which are not related to the delivery of its supervisory tasks.[11] It is invested in euro-denominated assets, subject to the limits imposed by its risk control framework. This results in a more diversified maturity structure (Chart 9) than in the foreign reserves portfolio.

Chart 9

Maturity profile of the ECB’s own funds securities

Source: ECB.

At the end of 2021, the total value of euro banknotes in circulation was €1,544.4 billion, an increase of 8% compared to the end of 2020. The ECB has been allocated an 8% share of the total value of euro banknotes in circulation, which amounted to €123.6 billion at the end of the year. Since the ECB does not issue banknotes itself, it holds intra-Eurosystem claims vis-à-vis the euro area NCBs for a value equivalent to the value of the banknotes in circulation.

The ECB’s intra-Eurosystem liabilities, which mainly comprise the net TARGET2 balance of euro area NCBs vis-à-vis the ECB and the ECB’s liabilities with regard to the foreign reserve assets transferred to it by the euro area NCBs when they joined the Eurosystem, decreased by €3.3 billion to €375.1 billion in 2021. The development of the intra-Eurosystem liabilities over the period from 2017 to 2020, was mostly driven by the evolution of the net TARGET2 liability as a result of the ECB’s net purchases of securities held for monetary policy purposes, which are settled via TARGET2 accounts (Chart 10).

In 2021, the impact of monetary policy securities purchases on the net TARGET2 liability was more than offset, mainly by the higher deposits of the ECB’s non-euro area TARGET2 customers and non-euro area residents accepted by the ECB in its role as fiscal agent and by the increase in cash received as collateral from security lending operations.

Chart 10

Net intra-Eurosystem TARGET2 balance and securities held for monetary policy purposes

(EUR billions)

Source: ECB.

1.3.2 Financial resources

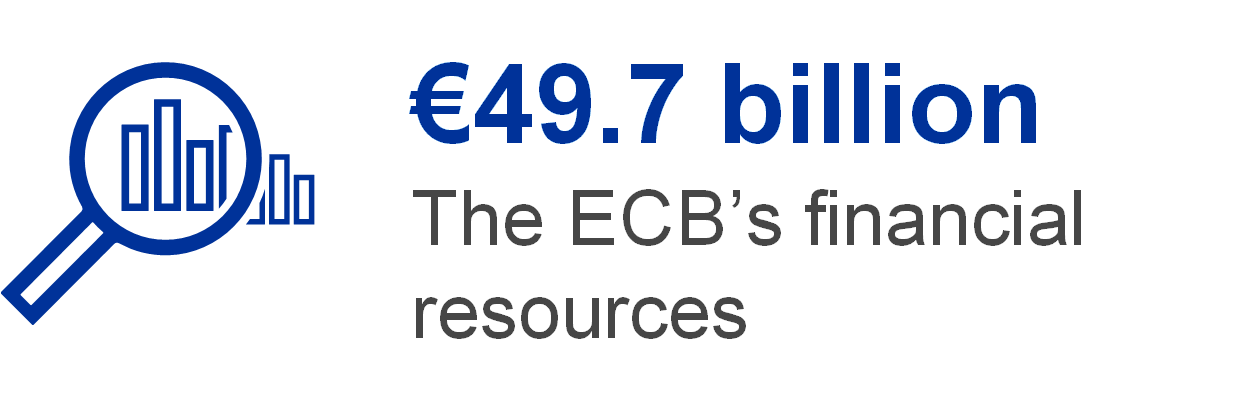

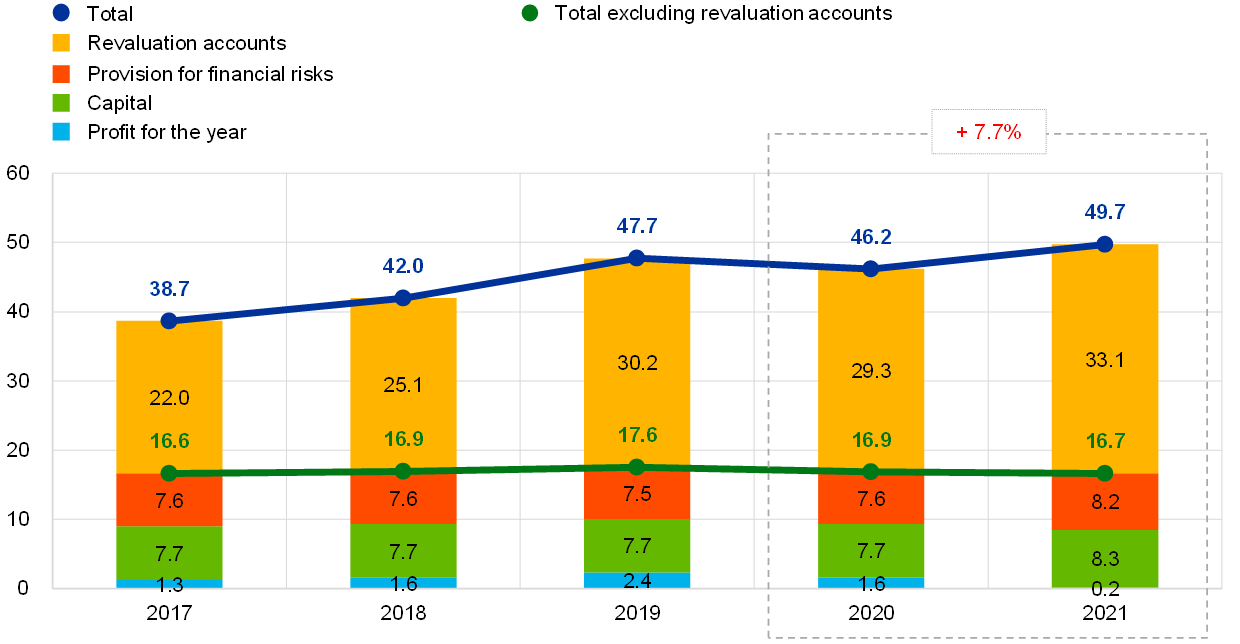

The ECB’s financial resources consist of its capital, the provision for financial risks, the revaluation accounts and the profit for the year. These financial resources are (i) invested in assets that generate income and/or (ii) used to directly offset losses materialising from financial risks. As at 31 December 2021, the ECB’s financial resources totalled €49.7 billion (Chart 11). This was €3.5 billion higher than in 2020 owing to increases in (i) the revaluation accounts following the appreciation of the US dollar against the euro as well as the rise in the market price of gold in euro terms in 2021, (ii) the paid-up capital and (iii) the provision for financial risks[12]. These increases more than offset the lower profit in 2021 compared to 2020.

Chart 11

The ECB’s financial resources

(EUR billions)

Source: ECB.

Note: “Revaluation accounts” includes total revaluation gains on gold, foreign currency and securities holdings, but excludes the revaluation account for post-employment benefits.

Unrealised gains on gold, foreign currencies and securities that are subject to price revaluation are not recognised as income in the Profit and Loss Account but are recorded directly in revaluation accounts shown on the liability side of the ECB’s Balance Sheet. The balances in these accounts can be used to absorb the impact of any future unfavourable movement in the respective prices and/or exchange rates, and thus strengthen the ECB’s resilience against the underlying risks. In 2021 the revaluation accounts for gold, foreign currencies and securities[13] increased by €3.8 billion to €33.1 billion owing to higher revaluation balances for foreign currencies and gold, mainly as a result of the appreciation of the US dollar against the euro (Chart 12) and the rise in the market price of gold in euro terms, which were partially offset by the decrease in the revaluation balances for securities.

Chart 12

The main foreign exchange rates and gold price over the period 2017-21

(percentage changes vis-à-vis 2017; year-end data)

Source: ECB.

Following the Bank of England’s departure from the ESCB in 2020, the shares of the remaining NCBs in the subscribed capital of the ECB increased. The Governing Council decided that the remaining NCBs would cover only the Bank of England’s withdrawn paid-up capital of €58 million in 2020 and that the euro area NCBs would pay up in full their increased subscriptions in two equal annual instalments in 2021 and 2022. Following the payment of the first instalment by the euro area NCBs, the ECB’s paid-up capital increased by €0.6 billion to €8.3 billion in 2021. It will increase by a further €0.6 billion to €8.9 billion in 2022.[14]

In view of its exposure to financial risks (see Section 1.4.1 “Financial risks”), the ECB maintains a provision for financial risks. The size of this provision is reviewed annually, taking a range of factors into account, including the level of holdings of risk-bearing assets, the projected results for the coming year and a risk assessment. The provision for financial risks, together with any amount held in the ECB’s general reserve fund, may not exceed the value of the capital paid up by the euro area NCBs.

As a result of the €0.6 billion increase in the ECB’s paid-up capital in 2021, the upper limit of the provision for financial risks increased by an equal amount. Taking into account the results of the assessment of the ECB’s exposures to financial risks, the Governing Council decided to transfer €0.6 billion to the ECB’s provision for financial risks, increasing it to its maximum permitted level of €8.2 billion.

The profit resulting from the ECB’s assets and liabilities in a given financial year can be used to absorb potential losses incurred in the same year. In 2021 the ECB’s profit, after the transfer to the provision for financial risks, was €0.2 billion (see Section 1.3.3 “Profit and Loss Account”).

1.3.3 Profit and Loss Account

The ECB’s annual profit reached a peak in 2019 after several years of increases, mainly owing to rising interest income generated on securities held for monetary policy purposes and on foreign reserve assets. In 2020 the ECB’s profit started to decrease, predominantly due to lower income on the aforementioned items.

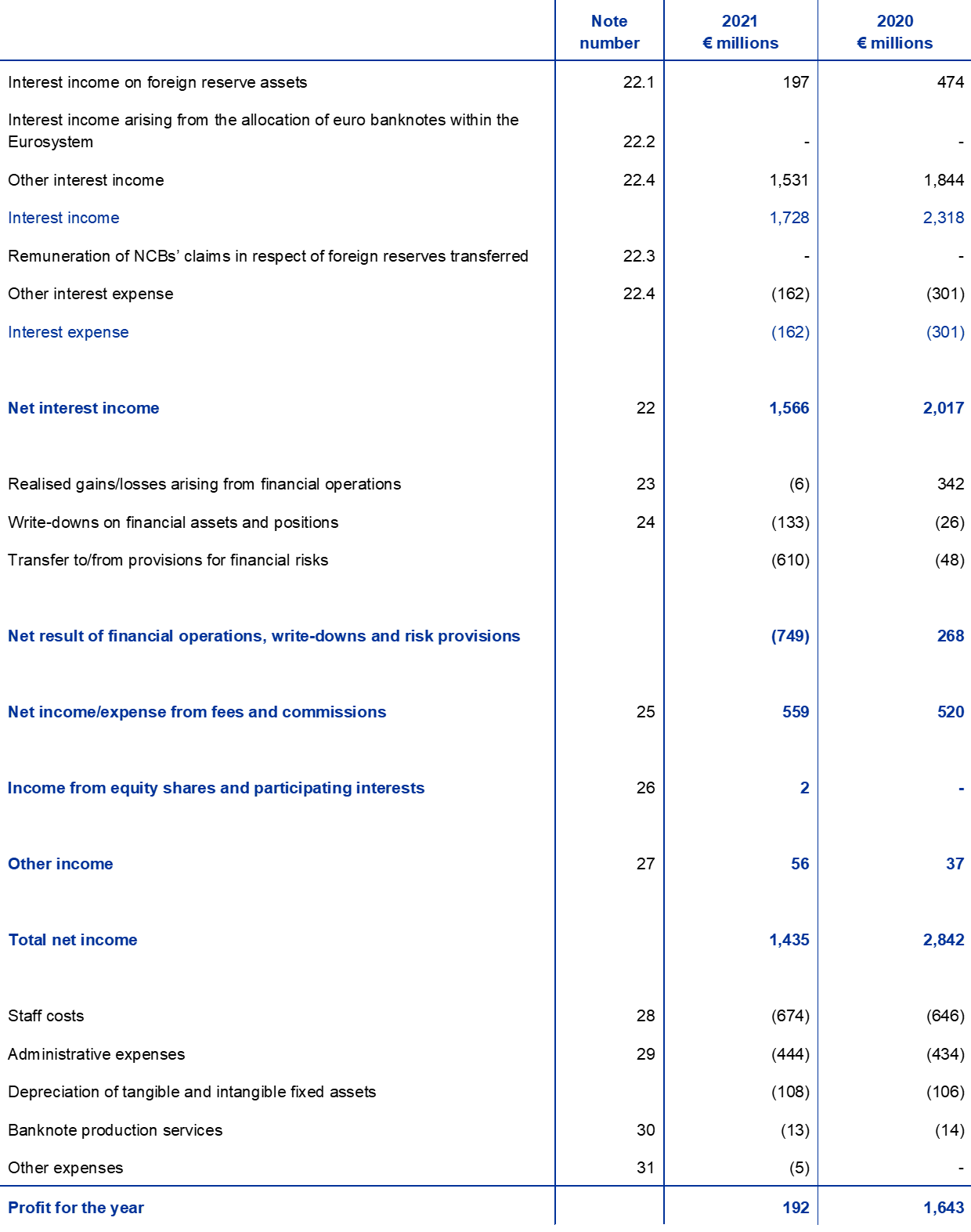

In 2021 the ECB’s profit was €192 million (2020: €1,643 million). The decrease of €1,452 million compared with 2020 was mainly driven by a lower net result of financial operations, write-downs and risk provisions, in particular due to the transfer to the provision for financial risks, and lower net interest income (Chart 13).

Chart 13

Main components of the ECB’s Profit and Loss Account

(EUR millions)

Source: ECB.

Note: “Other income and expenses” consists of “Net income/expense from fees and commissions”, “Income from equity shares and participating interests”, “Other income” and “Other expenses”.

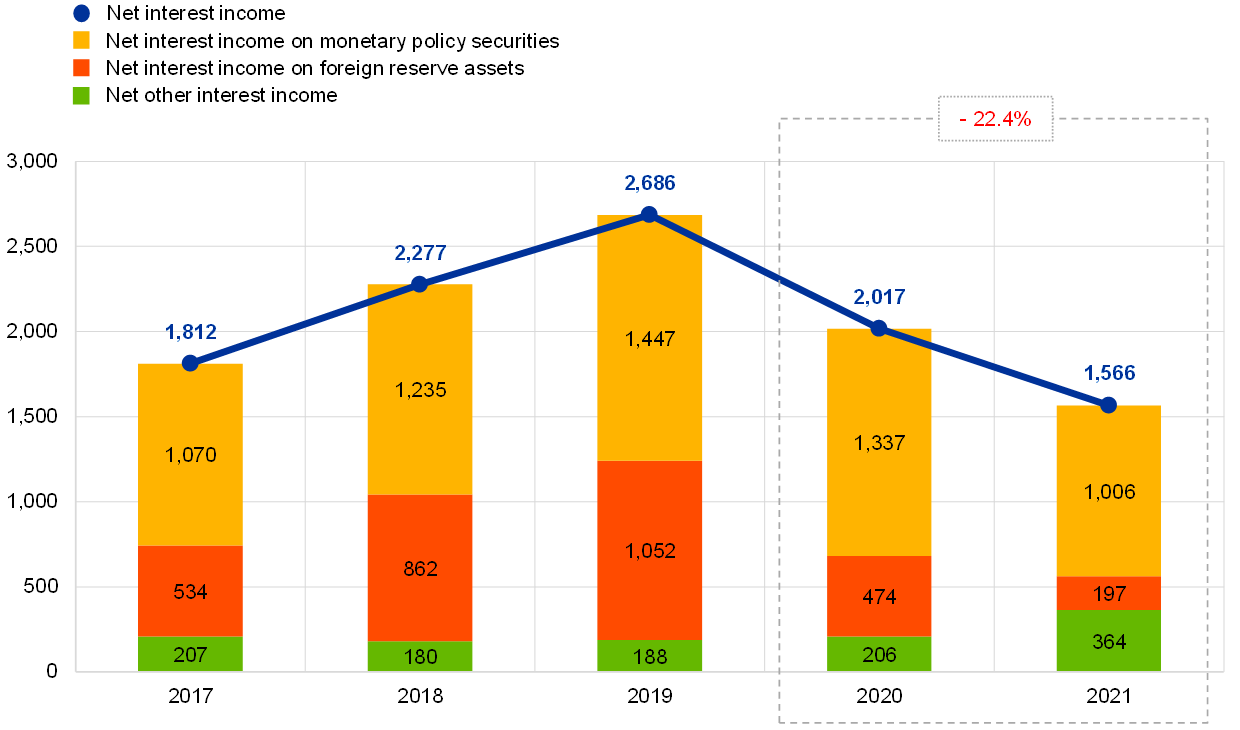

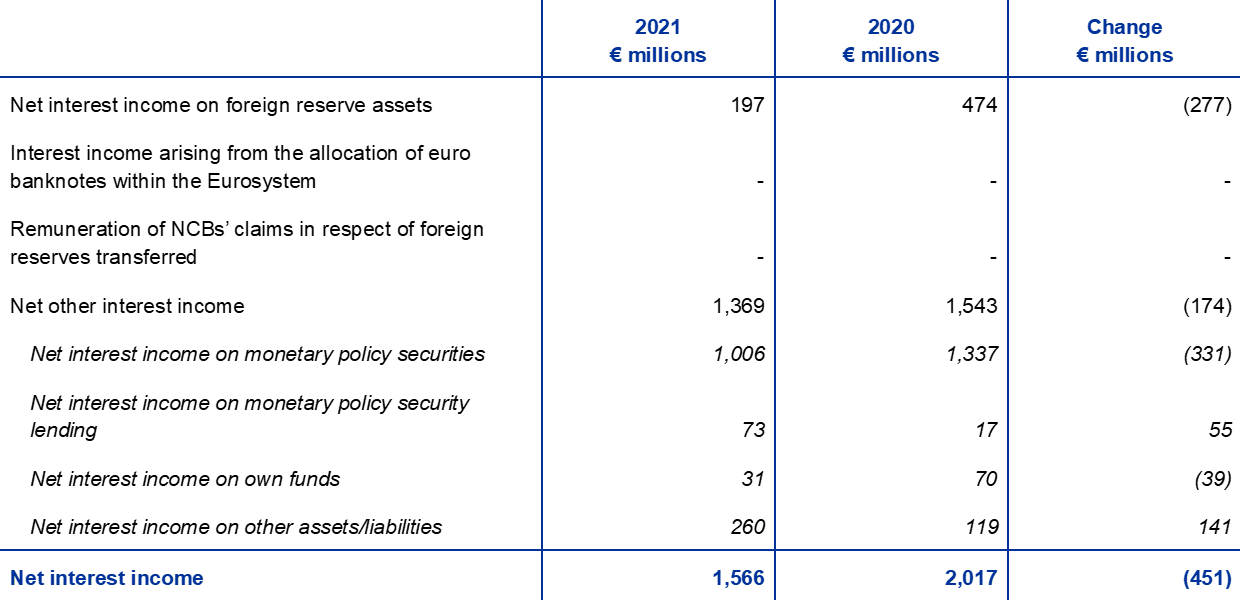

The net interest income of the ECB decreased by €451 million to €1,566 million (Chart 14) owing to lower interest income earned on securities held for monetary policy purposes and on foreign reserve assets. The increase in net other interest income only partially compensated for these decreases.

Chart 14

Net interest income

(EUR millions)

Source: ECB.

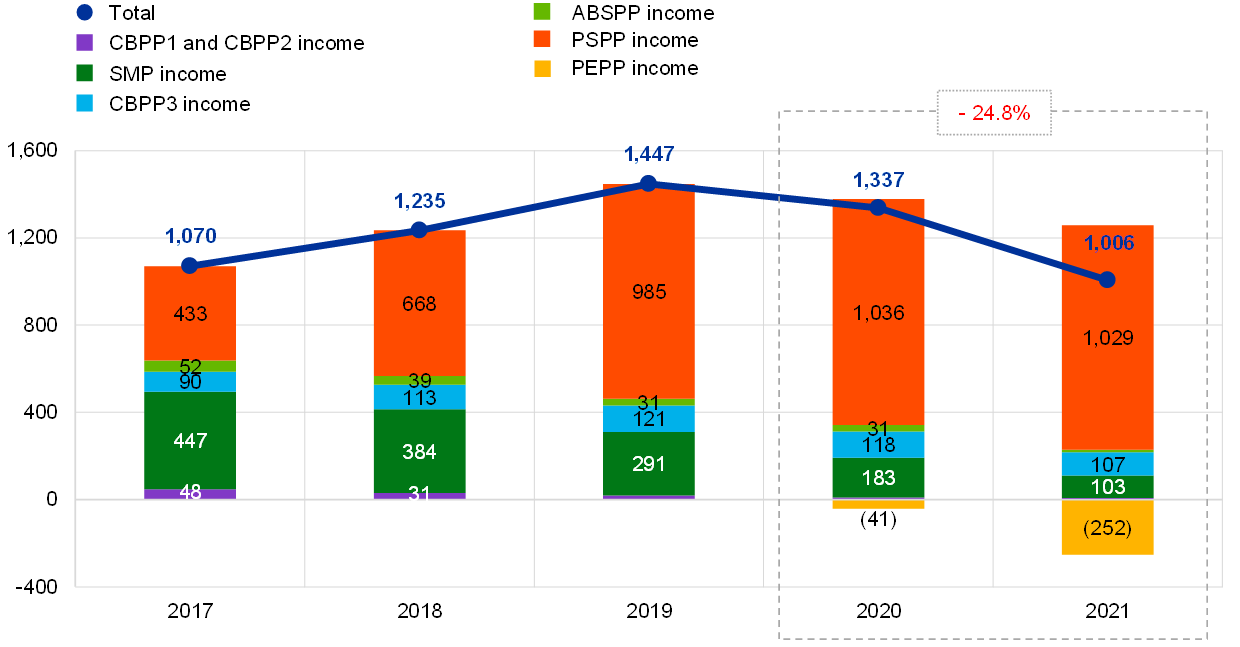

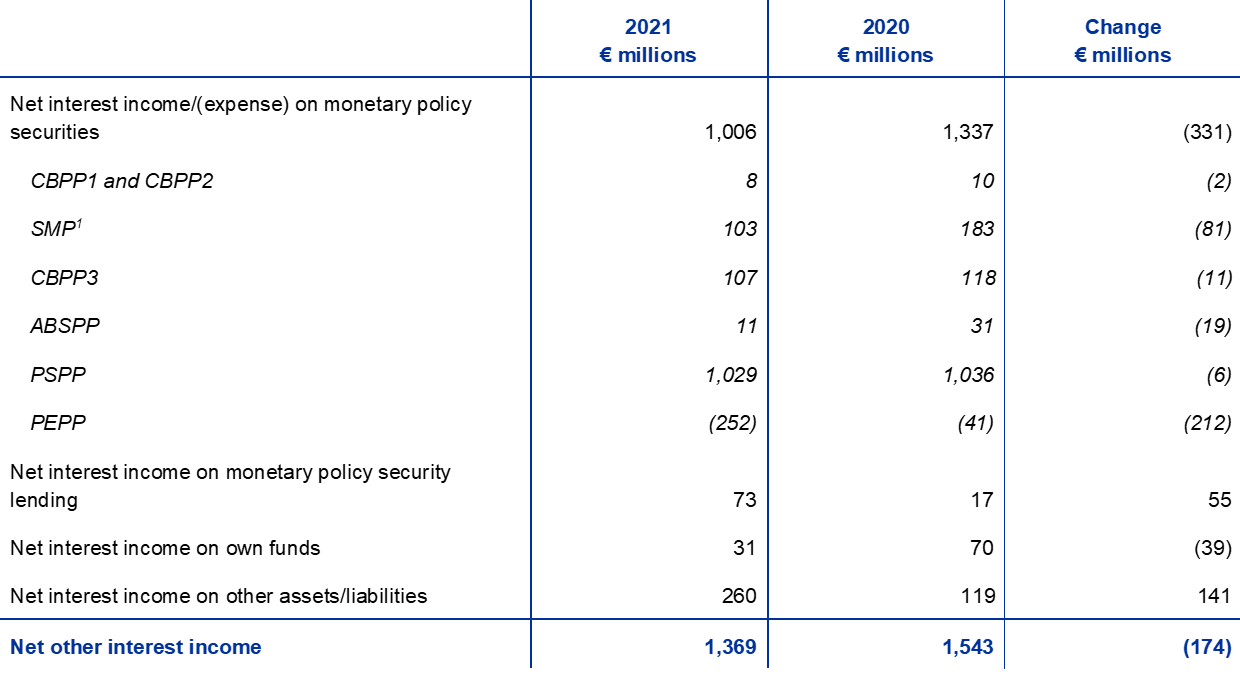

Net interest income generated on securities held for monetary policy purposes decreased by €331 million to €1,006 million in 2021 (Chart 15) mainly owing to negative net interest income on the PEPP portfolio. The continuation of public sector securities purchases under the PEPP – at a negative average yield as a result of the low euro area sovereign bond yields prevailing during the implementation of this programme (Chart 16) – led to increased negative net interest income of €252 million on this portfolio in 2021, compared to negative net interest income of €41 million the year before. In addition, net interest income on the SMP, CBPP1 and CBPP2 portfolios decreased by €82 million to €111 million owing to the decline in the size of these portfolios as a result of maturing securities. Finally, net interest income arising from the APP (from securities held under the ABSPP, CBPP3 and PSPP) decreased by €37 million to €1,147 million, mainly owing to a lower average interest rate earned on securities held under the ABSPP.

In 2021 securities held for monetary policy purposes generated 64% of the ECB’s net interest income.

Chart 15

Net interest income on securities held for monetary policy purposes

(EUR millions)

Source: ECB.

Chart 16

Seven-year sovereign bond yields in the euro area

(percentages per annum; month-end data)

Source: ECB.

Net interest income on foreign reserve assets decreased by €277 million to €197 million, mainly as a result of lower interest income earned on securities denominated in US dollars. Owing to the low US dollar bond yields throughout most of 2020 and 2021 (Chart 17), and sales and redemptions of higher yield bonds purchased in the past, the average interest rate earned on the ECB’s US dollar portfolio further decreased in 2021 compared to the previous year.

Chart 17

Two-year sovereign bond yields in the United States, Japan and China

(percentages per annum; month-end data)

Source: ECB.

Both the interest income on the ECB’s share of total euro banknotes in circulation and the interest expense related to the remuneration of NCBs’ claims in respect of foreign reserves transferred were zero as a result of the 0% interest rate used by the Eurosystem in its main refinancing operations (MROs) in 2021.

Net other interest income increased, mainly owing to higher interest income on (i) the accounts held at the ECB by the ECB’s non-euro area TARGET2 customers, (ii) monetary policy security lending operations and (iii) deposits accepted by the ECB in its role as fiscal agent, each as a result of the higher average balances in 2021. These increases more than compensated for the lower interest income earned on the own funds portfolio as a result of the low-yield environment in the euro area (Chart 16).

The net result of financial operations and write-downs on financial assets amounted to a loss of €139 million in 2021, compared to a gain of €316 million in 2020 (Chart 18). The main drivers of this were net realised price losses in 2021, compared to net realised price gains in 2020, and higher write-downs on US dollar and euro-denominated securities.

The net realised price losses stemmed from euro-denominated securities and US dollar-denominated interest rate futures. These losses were only partially offset by realised price gains on US dollar-denominated securities, which were still positive in 2021 but lower than the previous year, as US dollar bond yields remained stable throughout most of 2020 and 2021 before starting to rise towards the end of 2021.

Chart 18

Realised results and write-downs

(EUR millions)

Source: ECB.

In addition, as at 31 December 2021, €610 million was transferred to the ECB’s provision for financial risks, reducing the ECB’s profit by an equal amount. After taking the results of its risk assessment into account, the Governing Council decided to increase the size of the provision for financial risks to €8,194 million, which is its upper limit as determined by the paid-up capital of the euro area NCBs (see Section 1.3.2 “Financial resources”).

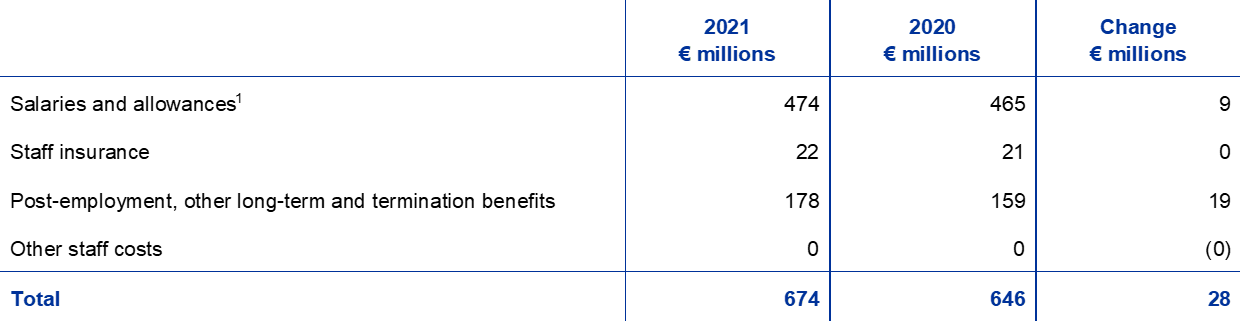

The total operating expenses of the ECB, including depreciation and banknote production services, increased by €39 million to €1,238 million (Chart 19). The increase compared to 2020 was mainly due to higher staff costs resulting from (i) higher costs in relation to post-employment benefits as a result of a higher current service cost following the annual actuarial valuation and (ii) the higher average number of staff in 2021. Administrative expenses increased slightly, mainly owing to higher property maintenance expenses.

Banking supervision-related expenses are fully covered by fees levied on the supervised entities. Based on the actual expenses incurred by the ECB in the performance of its banking supervision tasks, supervisory fee income for 2021 stood at €578 million.[15]

Chart 19

Operating expenses and supervisory fee income

(EUR millions)

Source: ECB.

1.4 Risk management

Risk management is a critical part of the ECB’s activities and is conducted through a continuous process of (i) risk identification and assessment, (ii) review of the risk strategy and policies, (iii) implementation of risk mitigating actions, and (iv) risk monitoring and reporting, all of which are supported by effective methodologies, processes and systems.

Figure 2

Risk management cycle

The following sections focus on the risks, their sources, and the applicable risk control frameworks.

1.4.1 Financial risks

The Executive Board proposes policies and procedures that ensure an appropriate level of protection against the financial risks to which the ECB is exposed. The Risk Management Committee (RMC), which comprises experts from Eurosystem central banks, contributes to the monitoring, measuring and reporting of financial risks related to the balance sheet of the Eurosystem, and it defines and reviews the associated methodologies and frameworks. In this way, the RMC helps the decision-making bodies to ensure an appropriate level of protection for the Eurosystem.

Financial risks arise from the ECB’s core activities and associated exposures. The risk control frameworks and limits that the ECB uses to manage its risk profile differ across types of operation, reflecting the policy or investment objectives of the different portfolios and the risk characteristics of the underlying assets.

To monitor and assess the risks, the ECB relies on a number of risk estimation techniques developed by its experts. These techniques are based on a joint market and credit risk simulation framework. The core modelling concepts, techniques and assumptions underlying the risk measures draw on industry standards and available market data. The risks are typically quantified as the expected shortfall (ES),[16] estimated at the 99% confidence level over a one-year horizon. Two approaches are used to calculate risks: (i) the accounting approach, under which the ECB’s revaluation accounts are considered as a buffer in the calculation of risk estimates in line with all applicable accounting rules; and (ii) the financial approach, under which the revaluation accounts are not considered as a buffer in the risk calculation. The ECB also calculates other risk measures at different confidence levels, performs sensitivity and stress scenario analyses, and assesses longer-term projections of exposures and income to maintain a comprehensive picture of the risks.[17]

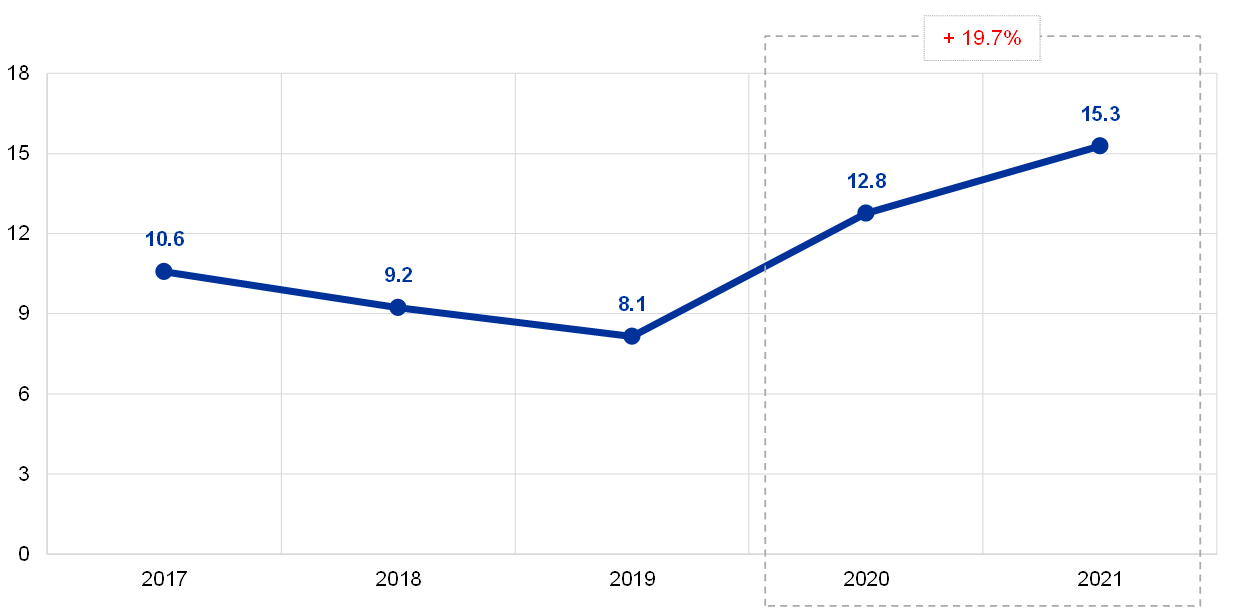

The total risks of the ECB increased during the year. At the end of 2021 the total financial risks for all the ECB’s portfolios combined, as measured by the ES at the 99% confidence level over a one-year horizon under the accounting approach, stood at €15.3 billion, which was €2.5 billion higher than the risks estimated as at the end of 2020 (Chart 20). The rise in estimated risks continues a trend which began in 2020 and reflects the growth of the ECB’s monetary policy portfolios as a result of asset purchases conducted under the PEPP and the APP.

Chart 20

Total financial risks (ES 99% accounting approach)

(EUR billions)

Source: ECB.

Credit risk arises from the ECB’s monetary policy portfolios, its euro-denominated own funds portfolio and its foreign reserve holdings. While securities held for monetary policy purposes are valued at amortised cost subject to impairment and are therefore, in the absence of sales, not subject to price changes associated with credit migrations, they are still subject to credit default risk. Euro-denominated own funds and foreign reserves are valued at market prices and, as such, are subject to credit migration and default risk. Credit risk increased compared with the previous year owing to the expansion of the ECB’s Balance Sheet through purchases of securities under the APP and the PEPP.

Credit risk is mitigated mainly through the application of eligibility criteria, due diligence procedures and limits that differ across portfolios.

Currency and commodity risks arise from the ECB’s foreign currency and gold holdings. The currency risk decreased compared to the previous year owing to higher currency revaluation accounts, which act as buffers against adverse exchange rate movements.

In view of the policy role of these assets, the ECB does not hedge the related currency and commodity risks. Instead, these risks are mitigated through the existence of revaluation accounts and the diversification of the holdings across different currencies and gold.

The ECB’s foreign reserves and euro-denominated own funds are mainly invested in fixed income securities and are subject to mark-to-market interest rate risk, given that they are valued at market prices. The ECB’s foreign reserves are mainly invested in assets with relatively short maturities (see Chart 7 in Section 1.3.1 “Balance Sheet”), while the assets in the own funds portfolio generally have longer maturities (see Chart 9 in Section 1.3.1 “Balance Sheet”). The interest rate risk of these portfolios, as measured under the accounting approach, increased slightly compared to 2020, reflecting developments in market conditions.

The mark-to-market interest rate risk of the ECB is mitigated through asset allocation policies and the revaluation accounts.

The ECB is also subject to interest rate risk arising from mismatches between the interest rate earned on its assets and the interest rate paid on its liabilities, which has an impact on its net interest income. This risk is not directly linked to any particular portfolio but rather to the structure of the ECB’s Balance Sheet as a whole and, in particular, the existence of maturity and yield mismatches between assets and liabilities. It is monitored by means of projections of the ECB’s profitability, which indicate that the ECB is expected to continue to earn net interest income in the coming years.

This type of risk is managed through asset allocation policies and is further mitigated by the existence of unremunerated liabilities on the ECB’s Balance Sheet.

1.4.2 Operational risk

The Executive Board is responsible for and approves the ECB’s operational risk[18] management (ORM) policy and framework. The Operational Risk Committee (ORC) supports the Executive Board in the performance of its role in overseeing the management of operational risks. ORM is an integral part of the ECB’s governance structure[19] and management processes.

The main objective of the ECB’s ORM framework is to contribute to ensuring that the ECB achieves its mission and objectives, while protecting its reputation and assets against loss, misuse and damage. Under the ORM framework, each business area is responsible for identifying, assessing, responding to, reporting on and monitoring its operational risks, incidents and controls. In this context, the ECB’s risk tolerance policy provides guidance with regard to risk response strategies and risk acceptance procedures. It is linked to a five-by-five risk matrix based on impact and likelihood grading scales using quantitative and qualitative criteria.

The environment in which the ECB operates is exposed to increasingly complex and interconnected threats and there are a wide range of operational risks associated with the ECB’s day-to-day activities. The main areas of concern for the ECB include a wide spectrum of non-financial risks resulting from people, information, systems, processes and external third-party providers. Consequently, the ECB has put in place processes to facilitate ongoing and effective management of its operational risks and to integrate risk information into the decision-making process. Moreover, the ECB is focusing on enhancing its resilience, taking a broad view of risks and opportunities from an end-to-end perspective, including sustainability aspects. As such, response structures and contingency plans have been established to ensure the continuity of critical business functions in the event of any disruption or crisis (such as the COVID-19 pandemic).

1.4.3 Conduct risk

The ECB has a dedicated Compliance and Governance Office as a key risk management function to strengthen the ECB’s governance framework in order to address conduct risk[20] at the ECB. Its purpose is to support the Executive Board in protecting the integrity and reputation of the ECB, to promote ethical standards of behaviour and to strengthen the ECB’s accountability and transparency. A high-level ECB Ethics Committee provides advice and guidance to high-level ECB officials on integrity and conduct matters and supports the Governing Council in managing related risks at executive level appropriately and coherently. At the level of the Eurosystem and the Single Supervisory Mechanism (SSM), the Ethics and Compliance Conference works towards achieving coherent implementation of the conduct frameworks for NCBs and national competent authorities (NCAs).

2 Financial statements of the ECB

2.1 Balance Sheet as at 31 December 2021

Notes: Totals in the financial statements and in the tables included in the notes may not add up due to rounding. The figures 0 and (0) indicate positive or negative amounts rounded to zero, while a dash (-) indicates zero.

2.2 Profit and Loss Account for the year ending 31 December 2021

Frankfurt am Main, 8 February 2022

European Central Bank

Christine Lagarde

President

2.3 Accounting policies

Form and presentation of the financial statements

The financial statements of the ECB have been drawn up in accordance with the following accounting policies,[21] which, in the view of the Governing Council of the ECB, achieve a fair presentation of the financial statements, reflecting at the same time the nature of central bank activities.

Accounting principles

The following accounting principles have been applied: economic reality and transparency, prudence, recognition of post-balance sheet events, materiality, going concern, the accruals principle, consistency and comparability.

Recognition of assets and liabilities

An asset or liability is only recognised in the Balance Sheet when it is probable that any associated future economic benefit will flow to or from the ECB, substantially all of the associated risks and rewards have been transferred to the ECB, and the cost or value of the asset or the amount of the obligation can be measured reliably.

Basis of accounting

The accounts have been prepared on a historical cost basis, modified to include the market valuation of marketable securities (other than securities currently held for monetary policy purposes), gold and all other on-balance-sheet and off-balance-sheet assets and liabilities denominated in foreign currency.

Transactions in financial assets and liabilities are reflected in the accounts on the basis of the date on which they were settled.

With the exception of spot transactions in securities, transactions in financial instruments denominated in foreign currency are recorded in off-balance-sheet accounts on the trade date. At the settlement date the off-balance-sheet entries are reversed, and transactions are booked on-balance-sheet. Purchases and sales of foreign currency affect the net foreign currency position on the trade date, and realised results arising from sales are also calculated on that date. Accrued interest, premiums and discounts related to financial instruments denominated in foreign currency are calculated and recorded daily, and the foreign currency position is also affected daily by these accruals.

Gold and foreign currency assets and liabilities

Assets and liabilities denominated in foreign currency are converted into euro at the exchange rate prevailing on the balance sheet date. Income and expenses are converted at the exchange rate prevailing on the recording date. The revaluation of foreign exchange assets and liabilities, including on-balance-sheet and off-balance-sheet instruments, is performed on a currency-by-currency basis.

Revaluation to the market price for assets and liabilities denominated in foreign currency is treated separately from the exchange rate revaluation.

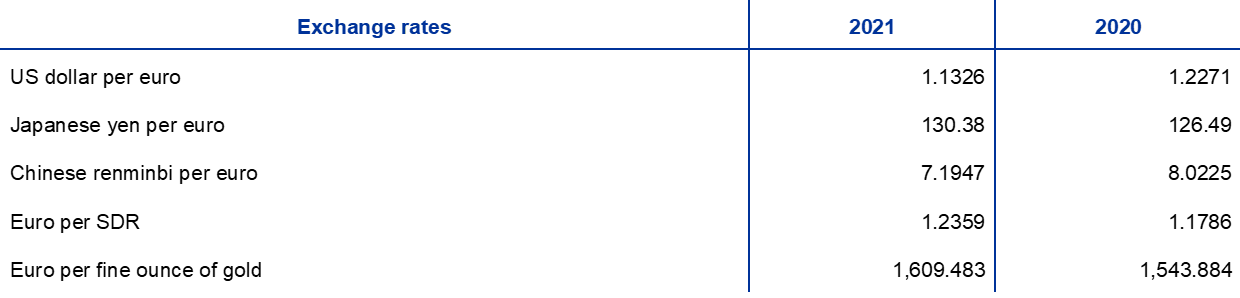

Gold is valued at the market price prevailing at the balance sheet date. No distinction is made between the price and currency revaluation differences for gold. Instead, a single gold valuation is accounted for on the basis of the price in euro per fine ounce of gold, which, for the year ending 31 December 2021, was derived from the exchange rate of the euro against the US dollar on 31 December 2021.

The special drawing right (SDR) is defined in terms of a basket of currencies and its value is determined by the weighted sum of the exchange rates of five major currencies (the US dollar, euro, Chinese renminbi, Japanese yen and pound sterling). The ECB’s holdings of SDRs were converted into euro using the exchange rate of the euro against the SDR as at 31 December 2021.

Securities

Securities held for monetary policy purposes

Securities currently held for monetary policy purposes are accounted for at amortised cost subject to impairment.

Other securities

Marketable securities (other than securities currently held for monetary policy purposes) and similar assets are valued either at the mid-market prices or on the basis of the relevant yield curve prevailing on the balance sheet date, on a security-by-security basis. Options embedded in securities are not separated for valuation purposes. For the year ending 31 December 2021, mid-market prices on 30 December 2021 were used.

Marketable investment funds are revalued on a net basis at fund level, using their net asset value. No netting is applied between unrealised gains and losses in different investment funds.

Illiquid equity shares and any other equity instruments held as permanent investments are valued at cost subject to impairment.

Income recognition

Income and expenses are recognised in the period in which they are earned or incurred.[22] Realised gains and losses resulting from the sale of foreign currency, gold and securities are recorded in the Profit and Loss Account. Such realised gains and losses are calculated by reference to the average cost of the respective asset.

Unrealised gains are not recognised as income and are transferred directly to a revaluation account.

Unrealised losses are recorded in the Profit and Loss Account if, at the year-end, they exceed previous revaluation gains accumulated in the corresponding revaluation account. Such unrealised losses on any one security or currency or on gold are not netted against unrealised gains on other securities or currencies or gold. In the event of such unrealised losses on any item recorded in the Profit and Loss Account, the average cost of that item is reduced to the year-end exchange rate or market price.

Impairment losses are recorded in the Profit and Loss Account and are not reversed in subsequent years unless the impairment decreases and the decrease can be related to an observable event that occurred after the impairment was first recorded.

Premiums or discounts arising on securities are amortised over the securities’ remaining contractual life.

Reverse transactions

Reverse transactions are operations whereby the ECB buys or sells assets under a repurchase agreement or conducts credit operations against collateral.

Under a repurchase agreement, securities are sold for cash with a simultaneous agreement to repurchase them from the counterparty at an agreed price on a set future date. Repurchase agreements are recorded as collateralised deposits on the liability side of the Balance Sheet. Securities sold under such an agreement remain on the Balance Sheet of the ECB.

Under a reverse repurchase agreement, securities are bought for cash with a simultaneous agreement to sell them back to the counterparty at an agreed price on a set future date. Reverse repurchase agreements are recorded as collateralised loans on the asset side of the Balance Sheet, but are not included in the ECB’s security holdings.

Reverse transactions (including securities lending transactions) conducted under a programme offered by a specialised institution are recorded on the Balance Sheet only where collateral has been provided in the form of cash and this cash remains uninvested.

Off-balance-sheet instruments

Currency instruments, namely foreign exchange forward transactions, forward legs of foreign exchange swaps and other currency instruments involving an exchange of one currency for another at a future date, are included in the net foreign currency position for the purpose of calculating foreign exchange gains and losses.

Interest rate instruments are revalued on an item-by-item basis. Daily changes in the variation margin of open interest rate futures contracts, as well as interest rate swaps that are cleared via a central counterparty, are recorded in the Profit and Loss Account. The valuation of forward transactions in securities is carried out by the ECB based on generally accepted valuation methods using observable market prices and rates, as well as discount factors from the settlement dates to the valuation date.

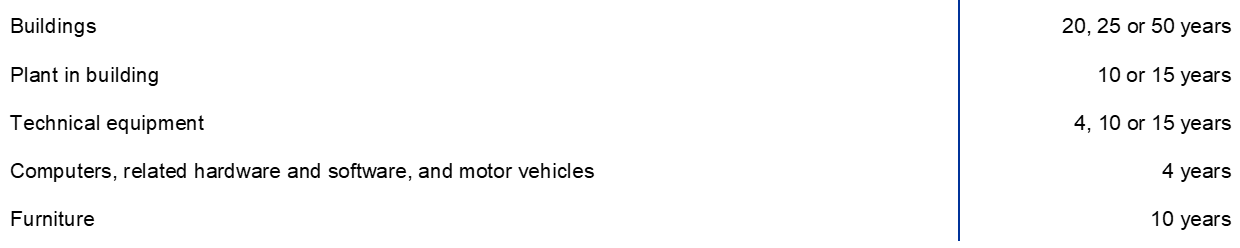

Fixed assets

Fixed assets, including intangible assets, but excluding land and works of art, are valued at cost less depreciation. Land and works of art are valued at cost. The ECB’s main building is valued at cost less depreciation subject to impairment. For the depreciation of the ECB’s main building, costs are assigned to the appropriate asset components, which are depreciated in accordance with their estimated useful lives. Depreciation is calculated on a straight-line basis over the expected useful life of the asset, beginning in the quarter after the asset is available for use. The useful lives applied for the main asset classes are as follows:

The depreciation period for capitalised refurbishment expenditure relating to the ECB’s existing rented premises is adjusted to take account of any events that have an impact on the expected useful life of the affected asset.

The ECB performs an annual impairment test of its main building and right-of-use assets relating to office buildings (see “Leases” below). If an impairment indicator is identified, and it is assessed that the asset may be impaired, the recoverable amount is estimated. An impairment loss is recorded in the Profit and Loss Account if the recoverable amount is less than the net book value.

Fixed assets costing less than €10,000 are written off in the year of acquisition.

Fixed assets that comply with the capitalisation criteria, but are still under construction or development, are recorded under the heading “Assets under construction”. The related costs are transferred to the relevant fixed asset headings once the assets are available for use.

Leases

For all leases involving a tangible asset, the related right-of-use asset and lease liability are recognised on the Balance Sheet at the lease commencement date and included under “Tangible and intangible fixed assets” and “Sundry” (liabilities), respectively. Where leases comply with the capitalisation criteria, but the asset involved is still under construction or adaptation, the incurred costs before the lease commencement date are recorded under the heading “Assets under construction”. The related right-of-use asset and lease liability are recognised under the relevant fixed asset headings once the asset is available for use (lease commencement date).

Right-of-use assets are valued at cost less depreciation. In addition, right-of-use assets relating to office buildings are subject to impairment (regarding the annual impairment test, see “Fixed assets” above). Depreciation is calculated on a straight-line basis from the commencement date to either the end of the useful life of the right-of-use asset or the end of the lease term, whichever is earlier.

The lease liability is initially measured at the present value of the future lease payments (comprising only lease components), discounted using the ECB's incremental borrowing rate. Subsequently, the lease liability is measured at amortised cost using the effective interest method. The related interest expense is recorded in the Profit and Loss Account under “Other interest expense”. When there is a change in future lease payments arising from a change in an index or other reassessment of the existing contract, the lease liability is remeasured. Any such remeasurement results in a corresponding adjustment to the carrying amount of the right-of-use asset.

Short-term leases with a duration of 12 months or less and leases of low-value assets below €10,000 (consistent with the threshold used for the recognition of fixed assets) are recorded as an expense in the Profit and Loss Account.

The ECB’s post-employment benefits, other long-term benefits and termination benefits

The ECB operates defined benefit plans for its staff and the members of the Executive Board, as well as for the members of the Supervisory Board employed by the ECB.

The staff pension plan is funded by assets held in a long-term employee benefit fund. The compulsory contributions made by the ECB and the staff are reflected in the defined benefit pillar of the plan. Staff can make additional contributions on a voluntary basis in a defined contribution pillar that can be used to provide additional benefits.[23] These additional benefits are determined by the amount of voluntary contributions together with the investment returns arising from those contributions.

Unfunded arrangements are in place for the post-employment and other long-term benefits of members of the Executive Board and members of the Supervisory Board employed by the ECB. For staff, unfunded arrangements are in place for post-employment benefits other than pensions and for other long-term benefits and termination benefits.

Net defined benefit liability

The liability recognised in the Balance Sheet under “Sundry” (liabilities) in respect of the defined benefit plans, including other long-term benefits and termination benefits, is the present value of the defined benefit obligation at the balance sheet date, less the fair value of plan assets used to fund the related obligation.

The defined benefit obligation is calculated annually by independent actuaries using the projected unit credit method. The present value of the defined benefit obligation is calculated by discounting the estimated future cash flows using a rate which is determined by reference to market yields at the balance sheet date on high-quality euro-denominated corporate bonds that have similar terms to maturity to the related obligation.

Actuarial gains and losses can arise from experience adjustments (where actual outcomes are different from the actuarial assumptions previously made) and changes in actuarial assumptions.

Net defined benefit cost

The net defined benefit cost is split into components reported in the Profit and Loss Account and remeasurements in respect of post-employment benefits shown in the Balance Sheet under “Revaluation accounts”.

The net amount charged to the Profit and Loss Account comprises:

- the current service cost of the defined benefits accruing for the year;

- the past service cost of the defined benefits resulting from a plan amendment;

- net interest at the discount rate on the net defined benefit liability;

- remeasurements in respect of other long-term benefits and termination benefits of a long-term nature, if any, in their entirety.

The net amount shown under “Revaluation accounts” comprises the following items:

- actuarial gains and losses on the defined benefit obligation;

- the actual return on plan assets, excluding amounts included in the net interest on the net defined benefit liability;

- any change in the effect of the asset ceiling, excluding amounts included in the net interest on the net defined benefit liability.

These amounts are valued annually by independent actuaries to establish the appropriate liability in the financial statements.

Intra-ESCB balances/intra-Eurosystem balances

Intra-ESCB balances result primarily from cross-border payments in the European Union (EU) that are settled in central bank money in euro. These transactions are for the most part initiated by private entities (i.e. credit institutions, corporations and individuals). They are settled in TARGET2 – the Trans-European Automated Real-time Gross settlement Express Transfer system – and give rise to bilateral balances in the TARGET2 accounts of EU central banks. These bilateral balances are netted and then assigned to the ECB on a daily basis, leaving each national central bank (NCB) with a single net bilateral position vis-à-vis the ECB only. Payments conducted by the ECB and settled in TARGET2 also affect the single net bilateral positions. These positions in the books of the ECB represent the net claim or liability of each NCB against the rest of the European System of Central Banks (ESCB). Intra-Eurosystem balances of euro area NCBs vis-à-vis the ECB arising from TARGET2, as well as other intra-Eurosystem balances denominated in euro (e.g. the ECB’s interim profit distribution to NCBs), are presented on the Balance Sheet of the ECB as a single net asset or liability position under either “Other claims within the Eurosystem (net)” or “Other liabilities within the Eurosystem (net)”. Intra-ESCB balances of non-euro area NCBs vis-à-vis the ECB, arising from their participation in TARGET2,[24] are disclosed under “Liabilities to non-euro area residents denominated in euro”.

Intra-Eurosystem balances arising from the allocation of euro banknotes within the Eurosystem are included as a single net asset under “Claims related to the allocation of euro banknotes within the Eurosystem” (see “Banknotes in circulation” below).

Intra-Eurosystem balances arising from the transfer of foreign reserve assets to the ECB by NCBs joining the Eurosystem are denominated in euro and reported under “Liabilities equivalent to the transfer of foreign reserves”.

Banknotes in circulation

The ECB and the euro area NCBs, which together comprise the Eurosystem, issue euro banknotes.[25] The total value of euro banknotes in circulation is allocated to the Eurosystem central banks on the last working day of each month in accordance with the banknote allocation key.[26]

The ECB has been allocated an 8% share of the total value of euro banknotes in circulation, which is disclosed in the Balance Sheet under the liability item “Banknotes in circulation”. The ECB’s share of the total euro banknote issue is backed by claims on the NCBs. These claims, which bear interest,[27] are disclosed under the sub-item “Intra-Eurosystem claims: claims related to the allocation of euro banknotes within the Eurosystem” (see “Intra-ESCB balances/intra-Eurosystem balances” above). Interest income on these claims is included in the Profit and Loss Account under the item “Interest income arising from the allocation of euro banknotes within the Eurosystem”.

Interim profit distribution

An amount that is equal to the sum of the ECB’s income on euro banknotes in circulation and income arising from the securities held for monetary policy purposes purchased under (i) the Securities Markets Programme, (ii) the third covered bond purchase programme, (iii) the asset-backed securities purchase programme, (iv) the public sector purchase programme, and (v) the pandemic emergency purchase programme is distributed in January of the following year by means of an interim profit distribution, unless otherwise decided by the Governing Council.[28] It is distributed in full unless it is higher than the ECB’s net profit for the year and subject to any decisions by the Governing Council to make transfers to the provision for financial risks. The Governing Council may also decide to reduce the amount of the income on euro banknotes in circulation to be distributed in January by the amount of the costs incurred by the ECB in connection with the issue and handling of euro banknotes.

Post-balance sheet events

The values of assets and liabilities are adjusted for events that occur between the annual balance sheet date and the date on which the Executive Board authorises the submission of the ECB’s Annual Accounts to the Governing Council for approval, if such events materially affect the condition of assets and liabilities at the balance sheet date.

Important post-balance sheet events that do not affect the condition of assets and liabilities at the balance sheet date are disclosed in the notes.

Changes to accounting policies

In 2021 there were no changes to the accounting policies applied by the ECB.

Other issues

In accordance with Article 27 of the Statute of the ESCB, and on the basis of a recommendation of the Governing Council, the EU Council has approved the appointment of Baker Tilly GmbH & Co. KG Wirtschaftsprüfungsgesellschaft, Düsseldorf (Federal Republic of Germany) as the external auditors of the ECB for a five-year period up to the end of the financial year 2022. This five-year period can be extended for up to two additional financial years.

2.4 Notes on the Balance Sheet

Note 1 - Gold and gold receivables

As at 31 December 2021 the ECB held 16,229,522 ounces of fine gold[29], the market value of which amounted to €26,121 million (2020: €25,056 million). No gold operations took place in 2021 and the ECB’s holdings therefore remained unchanged compared with their level as at 31 December 2020. The increase in the euro equivalent value of these holdings was due to the rise in the market price of gold in euro terms (see “Gold and foreign currency assets and liabilities” in Section 2.3 “Accounting policies” and note 15 “Revaluation accounts”).

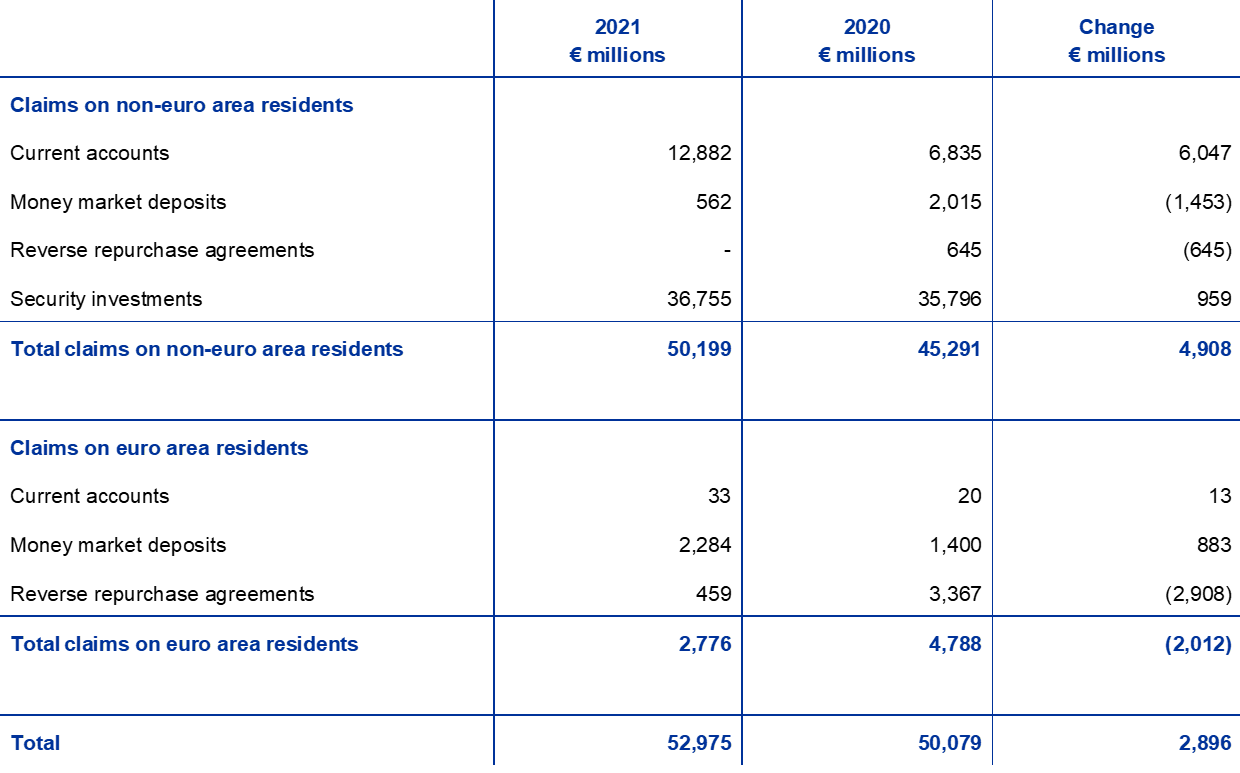

Note 2 - Claims on non-euro area and euro area residents denominated in foreign currency

Note 2.1 - Receivables from the IMF

This asset represents the ECB’s holdings of SDRs and amounted to €1,234 million as at 31 December 2021 (2020: €680 million). It arises as the result of a two-way SDR buying and selling voluntary trading arrangement with the International Monetary Fund (IMF), whereby the IMF is authorised to arrange sales or purchases of SDRs against euro, on behalf of the ECB, within minimum and maximum holding levels. For accounting purposes, SDRs are treated as a foreign currency (see “Gold and foreign currency assets and liabilities” in Section 2.3 “Accounting policies”). The ECB’s holdings in SDRs increased in 2021, mainly as a result of transactions that took place in the context of the above-mentioned voluntary trading arrangement. The appreciation of the SDR against the euro during 2021 also contributed to the increase in the euro equivalent value of these holdings.

Note 2.2 - Balances with banks and security investments, external loans and other external assets; and claims on euro area residents denominated in foreign currency

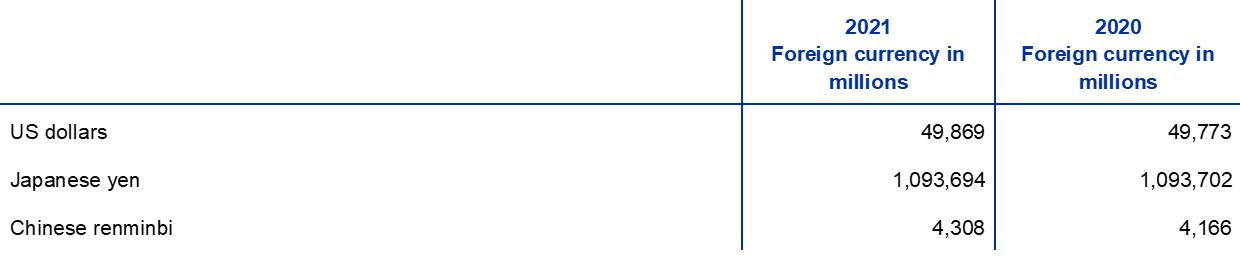

These two items consist of balances with banks and loans denominated in foreign currency, and investments in securities denominated in US dollars, Japanese yen and Chinese renminbi.

The total value of these items increased in 2021, mainly owing to the appreciation of the US dollar against the euro.

The ECB’s net foreign currency holdings[30] were as follows:

No foreign exchange interventions took place during 2021.

Note 3 - Claims on non-euro area residents denominated in euro

Note 3.1 - Balances with banks, security investments and loans

As at 31 December 2021 this item consisted of a claim amounting to €3,070 million (2020: €1,830 million) in relation to liquidity facility arrangements between the Eurosystem and non-euro area central banks. Under these arrangements, the Eurosystem provides euro liquidity to non-euro area central banks in exchange for eligible collateral[31] to address euro liquidity needs in their jurisdictions in case of market dysfunction and thereby minimise the risk of adverse spillover effects on euro area financial markets and economies.

Note 4 - Other claims on euro area credit institutions denominated in euro

As at 31 December 2021 this item consisted of current account balances with euro area residents amounting to €38 million (2020: €81 million).

Note 5 - Securities of euro area residents denominated in euro

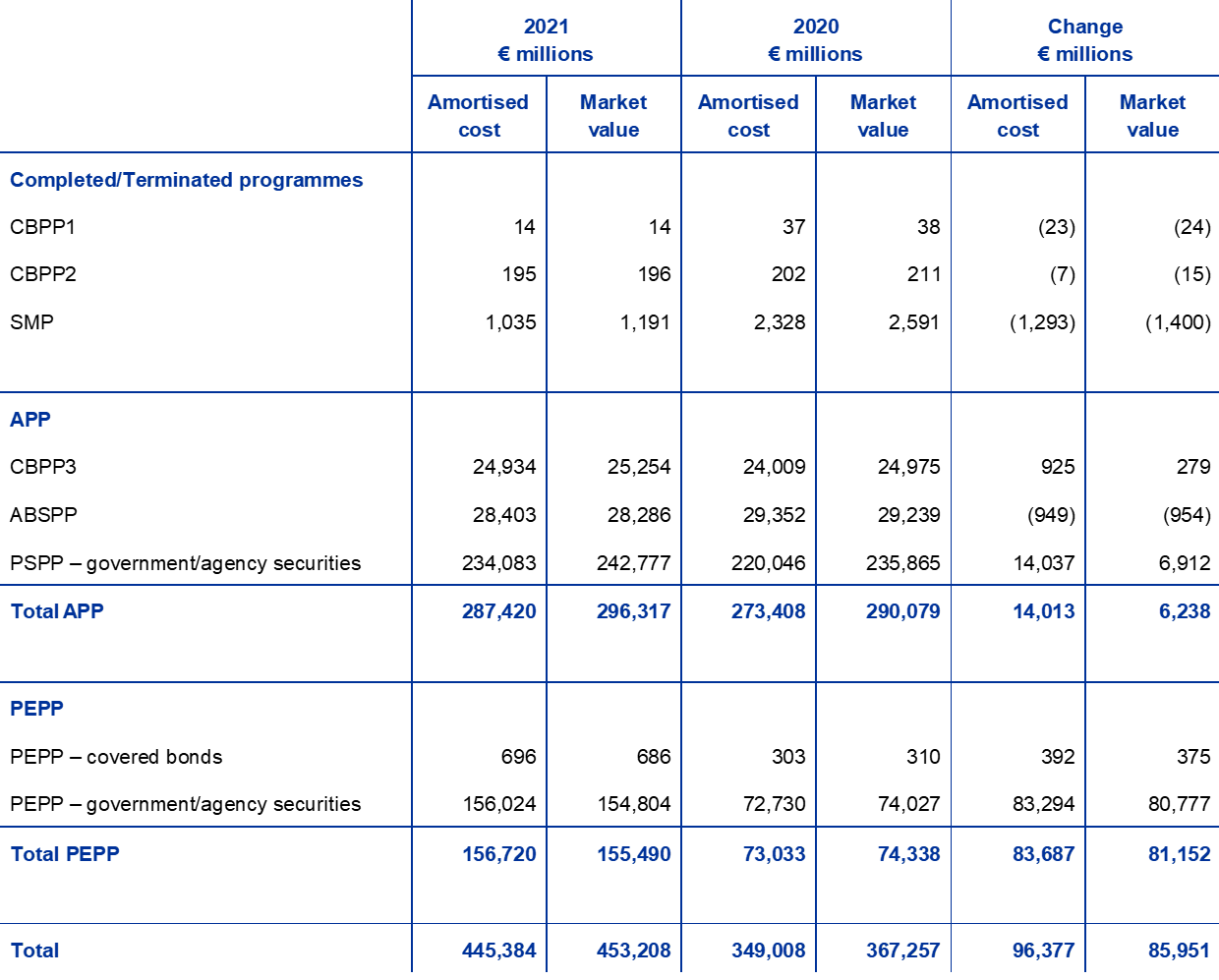

Note 5.1 - Securities held for monetary policy purposes

As at 31 December 2021 this item consisted of securities acquired by the ECB within the scope of the three covered bond purchase programmes (CBPPs), the Securities Markets Programme (SMP), the asset-backed securities purchase programme (ABSPP), the public sector purchase programme (PSPP) and the pandemic emergency purchase programme (PEPP).

1) Further eligibility criteria for the specific programmes can be found in the Governing Council’s decisions.

2) Only public debt securities issued by five euro area treasuries were purchased under the SMP.

3) The ECB does not acquire securities under the corporate sector purchase programme (CSPP).

4) A waiver of the eligibility requirements was granted for securities issued by the Greek Government.

In 2021 the Eurosystem conducted net purchases under the asset purchase programme (APP)[32] at a monthly pace of €20 billion on average. In December 2021 the Governing Council decided[33] on a monthly net purchase pace of €40 billion in the second quarter and €30 billion in the third quarter of 2022. From October 2022 onwards, the Governing Council will maintain net asset purchases at a monthly pace of €20 billion for as long as necessary to reinforce the accommodative impact of its policy rates, and expects to end these purchases shortly before it starts raising the key ECB interest rates. The Governing Council also intends to continue the reinvestments for an extended period of time past the date when the Governing Council starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

In addition, in 2021 the Eurosystem continued its net asset purchases under the PEPP[34], with a total envelope of €1,850 billion[35]. Purchases were conducted in a flexible manner based on the assessment of financing conditions and the inflation outlook. In December 2021 the Governing Council also decided to discontinue net asset purchases under the PEPP at the end of March 2022, but these could be resumed, if necessary, to counter negative shocks related to the coronavirus (COVID-19) pandemic. Furthermore, the Governing Council extended the reinvestment horizon for the principal payments from maturing securities purchased under the PEPP until at least the end of 2024. PEPP reinvestments can be adjusted flexibly across time, asset classes and jurisdictions and at any time. The future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

The securities purchased under these programmes are valued on an amortised cost basis subject to impairment (see “Securities” in Section 2.3 “Accounting policies”).

The amortised cost of the securities held by the ECB and their market value[36] (which is not recorded on the Balance Sheet or in the Profit and Loss Account and is provided for comparison purposes only) are as follows:

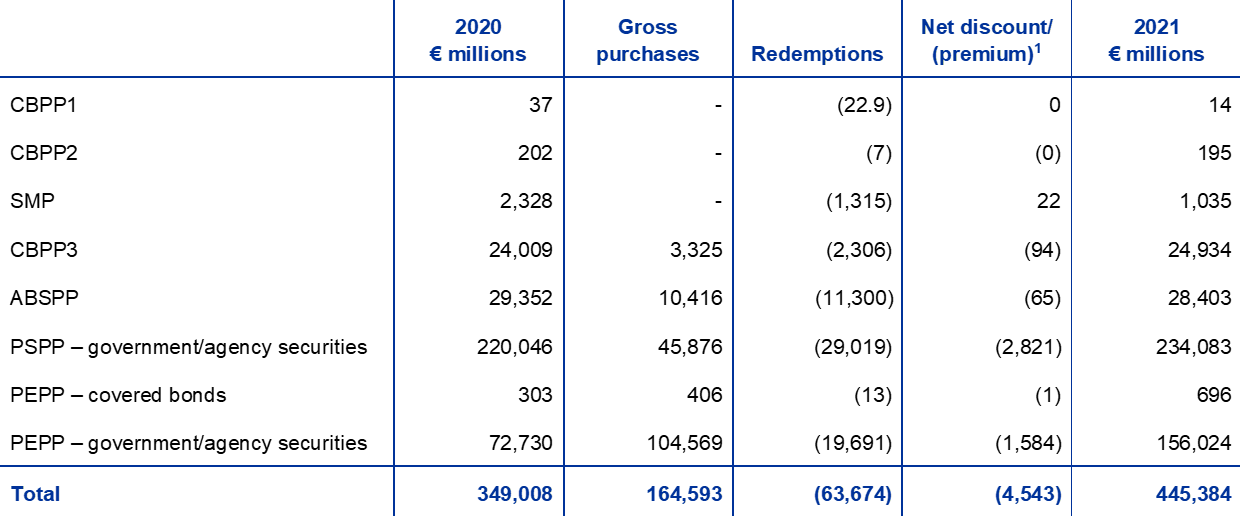

The amortised cost value of the securities held by the ECB changed during the year as follows:

1) "Net discount/(premium)" includes net realised gains/(losses), if any.

The Governing Council assesses on a regular basis the financial risks associated with the securities held under these programmes.

In this context, impairment tests are conducted on an annual basis, using data as at the year-end, and are approved by the Governing Council. In these tests, impairment indicators are assessed separately for each programme. In cases where impairment indicators are observed, further analysis is performed to confirm that the cash flows of the underlying securities have not been affected by an impairment event. Based on the results of this year’s impairment tests, no losses have been recorded by the ECB for the securities held in its monetary policy portfolios in 2021.

The amortised cost value of the securities held by the Eurosystem is as follows:

Note: “Euro area NCBs” figures are preliminary and may be subject to revision, which would also result in an equivalent change in the “Total Eurosystem” figures.

Note 6 - Intra-Eurosystem claims

Note 6.1 - Claims related to the allocation of euro banknotes within the Eurosystem

This item consists of the claims of the ECB vis-à-vis the euro area NCBs relating to the allocation of euro banknotes within the Eurosystem (see “Banknotes in circulation” in Section 2.3 “Accounting policies”) and as at 31 December 2021 amounted to €123,551 million (2020: €114,761 million). The remuneration of these claims is calculated daily at the latest available marginal interest rate used by the Eurosystem in its tenders for main refinancing operations[37] (see note 22.2 “Interest income arising from the allocation of euro banknotes within the Eurosystem”).

Note 7 - Other assets

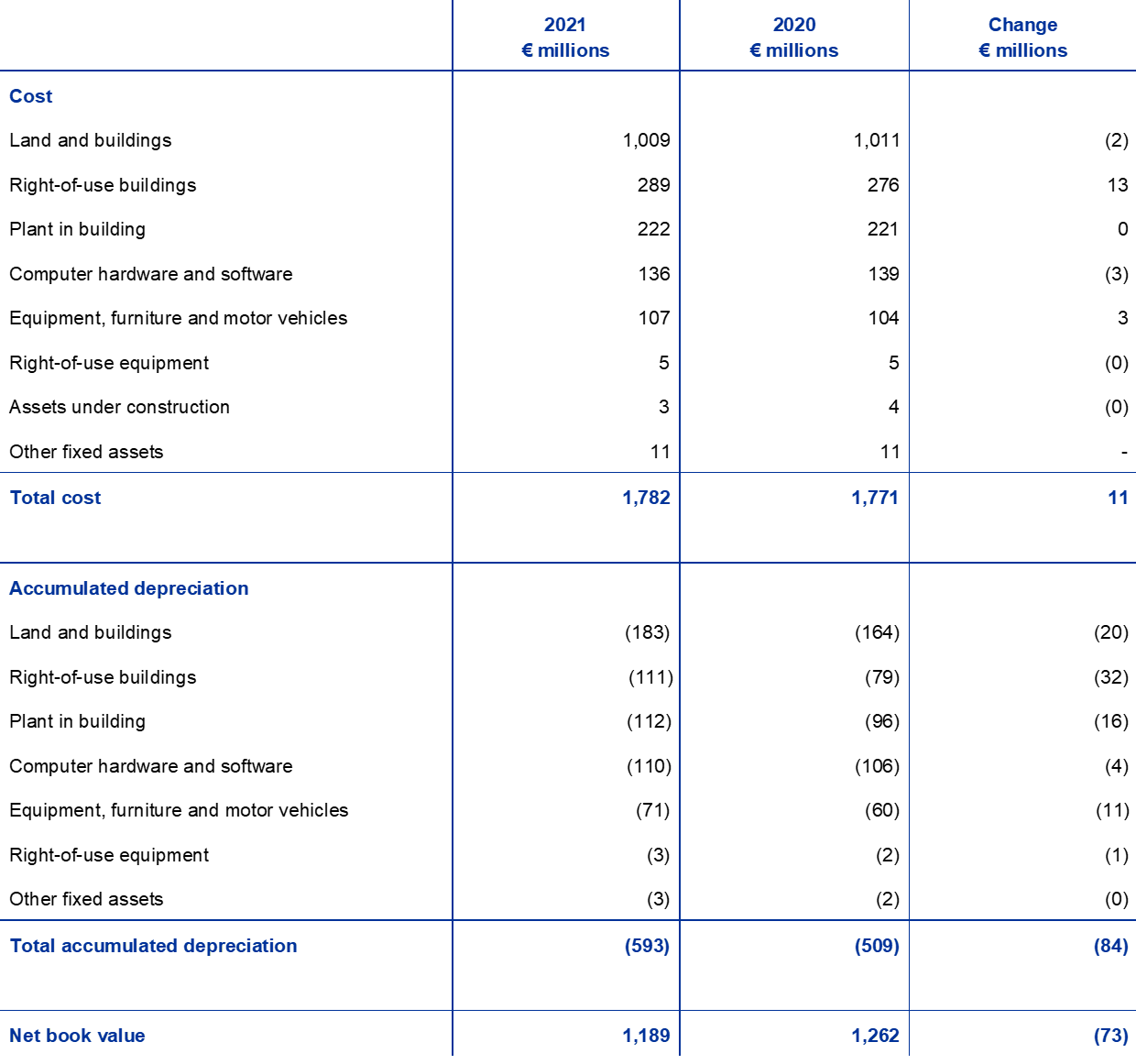

Note 7.1 - Tangible and intangible fixed assets

These assets comprised the following items:

In respect of the ECB’s main building and right-of-use office buildings, an impairment test was conducted at the end of the year and no impairment loss has been recorded.

Note 7.2 - Other financial assets

This item consists mainly of the ECB’s own funds portfolio, which predominantly consists of investments of the ECB’s financial resources, namely the paid-up capital and amounts held in the reserves and the provision for financial risks. It also includes 3,211 shares in the Bank for International Settlements (BIS) at the acquisition cost of €42 million and other current accounts denominated in euro.

The components of this item are as follows:

The net increase in this item in 2021 was primarily due to the investment in the ECB’s own funds portfolio of (i) the amounts paid up by the euro area NCBs in 2021 in respect of the first instalment of their increased subscriptions in the ECB’s capital (see note 16 “Capital and reserves”); (ii) the interest income generated on this portfolio in 2021; and (iii) the counterpart of the amount transferred to the ECB’s provision for financial risks in 2020. The increase in this item was partially offset, mainly by the decline in the market value of securities held in the ECB’s own funds portfolio.

Note 7.3 - Off-balance-sheet instruments revaluation differences

This item is composed of valuation changes in swap and forward transactions in foreign currency that were outstanding on 31 December 2021 (see note 20 “Foreign exchange swap and forward transactions”). These valuation changes amounted to €620 million (2020: €388 million) and are the result of the conversion of such transactions into their euro equivalents at the exchange rates prevailing on the balance sheet date, compared with the euro values resulting from the conversion of the transactions at the average cost of the respective foreign currency on that date (see “Off-balance-sheet instruments” and “Gold and foreign currency assets and liabilities” in Section 2.3 “Accounting policies”).

Note 7.4 - Accruals and prepaid expenses

On 31 December 2021 this item stood at €4,055 million (2020: €3,390 million). It comprised mainly accrued coupon interest on securities, including outstanding interest paid at acquisition, amounting to €3,332 million (2020: €2,757 million) (see note 2.2 “Balances with banks and security investments, external loans and other external assets; and claims on euro area residents denominated in foreign currency”, note 5 “Securities of euro area residents denominated in euro” and note 7.2 “Other financial assets”).

This item also included an amount of €577 million corresponding to the supervisory fees to be received for the fee period 2021 (see note 25 “Net income/expense from fees and commissions”).[38] This amount will be collected in 2022.

This item also includes (i) accrued income from common Eurosystem projects (see note 27 “Other income”); (ii) miscellaneous prepayments; and (iii) accrued interest income on other financial assets and liabilities.

Note 7.5 - Sundry

On 31 December 2021 this item amounted to €749 million (2020: €1,970 million) and mainly comprised balances with a value of €573 million (2020: €692 million) related to swap and forward transactions in foreign currency outstanding on 31 December 2021 (see note 20 “Foreign exchange swap and forward transactions”). These balances arose from the conversion of such transactions into their euro equivalents at the respective currency’s average cost on the balance sheet date, compared with the euro values at which the transactions were initially recorded (see “Off-balance-sheet instruments” in Section 2.3 “Accounting policies”).

It also included the accrued amount of the ECB’s interim profit distribution of €150 million (2020: €1,260 million) (see “Interim profit distribution” in Section 2.3 “Accounting policies” and note 12.2 “Other liabilities within the Eurosystem (net)”).

Note 8 - Banknotes in circulation

This item consists of the ECB’s share (8%) of total euro banknotes in circulation (see “Banknotes in circulation” in Section 2.3 “Accounting policies”) and as at 31 December 2021 amounted to €123,551 million (2020: €114,761 million).

Note 9 - Other liabilities to euro area credit institutions denominated in euro

The Eurosystem central banks have the possibility of accepting cash as collateral in their PSPP securities lending facilities without having to reinvest it. In the case of the ECB, these operations are conducted via a specialised institution. The same conditions apply to the public sector PEPP holdings.

As at 31 December 2021 the outstanding value of such lending transactions against cash collateral conducted with euro area credit institutions was €9,473 million (2020: €2,559 million). Cash received as collateral was transferred to TARGET2 accounts. As the cash remained uninvested at the year-end, these transactions were recorded on the Balance Sheet (see “Reverse transactions” in Section 2.3 “Accounting policies”).[39]

Note 10 - Liabilities to other euro area residents denominated in euro

Note 10.1 - General government

As at 31 December 2021 this item amounted to €3,200 million (2020: €10,012 million) and included deposits of the European Financial Stability Facility (EFSF) and the European Stability Mechanism (ESM). In accordance with Article 21 of the Statute of the ESCB, the ECB may act as fiscal agent for Union institutions, bodies, offices or agencies, central governments, regional, local or other public authorities, other bodies governed by public law, or public undertakings of Member States.

Note 10.2 – Other liabilities

This item consists of balances of the ECB’s euro area TARGET2 customers and as at 31 December 2021 amounted to €4,404 million (2020: €3,688 million).

Note 11 - Liabilities to non-euro area residents denominated in euro

As at 31 December 2021 this item amounted to €112,492 million (2020: €11,567 million). The largest component was an amount of €71,875 million (2020: €4,685 million) consisting of TARGET2 balances of non-euro area NCBs vis-à-vis the ECB (see “Intra-ESCB balances/intra-Eurosystem balances” in Section 2.3 “Accounting policies”) and of the ECB’s non-euro area TARGET2 customers. The increase in these balances in 2021 corresponds to higher balances of the ECB’s non-euro area TARGET2 customers.

It also comprised an amount of €21,750 million (2020: €3,425 million) arising from outstanding PSPP and public sector PEPP securities lending transactions conducted with non-euro area residents in which cash was received as collateral and transferred to TARGET2 accounts (see note 9 “Other liabilities to euro area credit institutions denominated in euro”).

This item also included an amount of €18,033 million relating to the administration of EU borrowing and lending activities, where the ECB acts as fiscal agent for the European Commission (see note 21 “Administration of borrowing and lending operations”). No such balances were outstanding as at 31 December 2020.

The remainder of this item consists of an amount of €834 million (2020: €3,457 million) arising from the standing reciprocal currency arrangement with the Federal Reserve System. Under this arrangement, US dollars are provided by the Federal Reserve Bank of New York to the ECB by means of swap transactions, with the aim of offering short-term US dollar funding to Eurosystem counterparties. The ECB simultaneously enters into back-to-back swap transactions with euro area NCBs, which use the resulting funds to conduct US dollar liquidity-providing operations with Eurosystem counterparties in the form of reverse transactions. The back-to-back swap transactions result in intra-Eurosystem balances between the ECB and the euro area NCBs. Furthermore, the swap transactions conducted with the Federal Reserve Bank of New York and the euro area NCBs result in forward claims and liabilities that are recorded in off-balance-sheet accounts (see note 20 “Foreign exchange swap and forward transactions”).

Note 12 - Intra-Eurosystem liabilities

Note 12.1 - Liabilities equivalent to the transfer of foreign reserves

These represent the liabilities to euro area NCBs that arose from the transfer of foreign reserve assets to the ECB when they joined the Eurosystem. Pursuant to Article 30.2 of the Statute of the ESCB, these contributions are fixed in proportion to the NCBs’ shares in the subscribed capital of the ECB. No changes occurred in 2021.

The remuneration of these liabilities is calculated daily at the latest available marginal interest rate used by the Eurosystem in its tenders for main refinancing operations, adjusted to reflect a zero return on the gold component (see note 22.3 “Remuneration of NCBs’ claims in respect of foreign reserves transferred”).

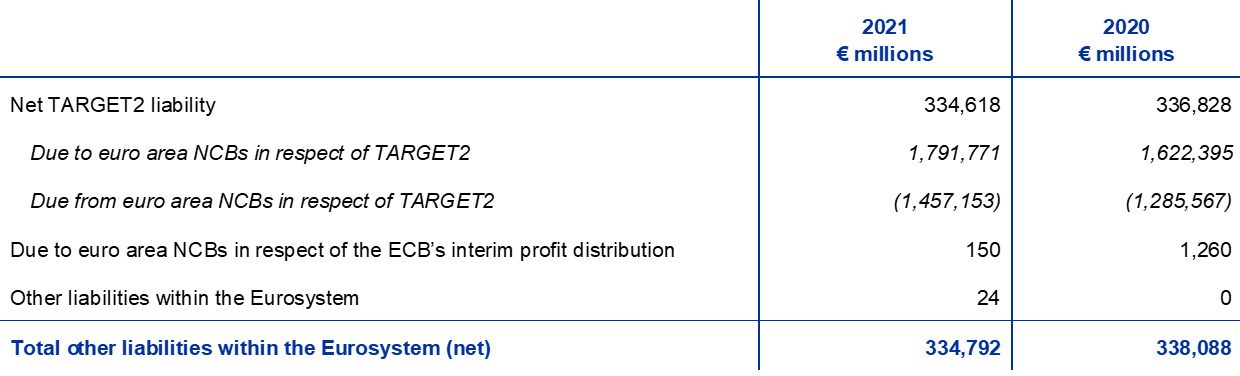

Note 12.2 - Other liabilities within the Eurosystem (net)

In 2021 this item consisted predominantly of the TARGET2 balances of euro area NCBs vis-à-vis the ECB and the amount due to euro area NCBs in respect of the ECB’s interim profit distribution (see “Intra-ESCB balances/intra-Eurosystem balances” and “Interim profit distribution”, respectively, in Section 2.3 “Accounting policies”).

The decrease in the net TARGET2 liability was mainly attributable to (i) the cash inflows as a result of the higher balances of the ECB’s non-euro area TARGET2 customers (see note 11 “Liabilities to non-euro area residents denominated in euro”); (ii) the increase in cash received as collateral against the lending of PSPP and public sector PEPP securities (see note 9 “Other liabilities to euro area credit institutions denominated in euro” and note 11 “Liabilities to non-euro area residents denominated in euro”); and (iii) the cash inflows as a result of the higher deposits of non-euro area residents accepted by the ECB in its role as fiscal agent (see note 11 “Liabilities to non-euro area residents denominated in euro”). The impact of these factors was largely offset by the net purchases of securities under the PEPP and the APP, which were settled via TARGET2 accounts (see note 5 “Securities of euro area residents denominated in euro”).

The remuneration of TARGET2 positions, with the exception of balances arising from back-to-back swap transactions in connection with US dollar liquidity-providing operations, is calculated daily at the latest available marginal interest rate used by the Eurosystem in its tenders for main refinancing operations.

Note 13 - Other liabilities

Note 13.1 - Off-balance-sheet instruments revaluation differences

This item is composed primarily of valuation changes in swap and forward transactions in foreign currency that were outstanding on 31 December 2021 (see note 20 “Foreign exchange swap and forward transactions”). These valuation changes amounted to €568 million (2020: €636 million) and are the result of the conversion of such transactions into their euro equivalents at the exchange rates prevailing on the balance sheet date, compared with the euro values resulting from the conversion of the transactions at the average cost of the respective foreign currency on that date (see “Off-balance-sheet instruments” and “Gold and foreign currency assets and liabilities” in Section 2.3 “Accounting policies”).

Valuation losses on outstanding forward transactions in securities are also included in this item (see note 19 “Forward transactions in securities”).

Note 13.2 - Accruals and income collected in advance

This item comprised the following components:

Note 13.3 - Sundry

On 31 December 2021 this item stood at €2,277 million (2020: €2,419 million). It included balances amounting to €535 million (2020: €507 million) related to swap and forward transactions in foreign currency that were outstanding on 31 December 2021 (see note 20 “Foreign exchange swap and forward transactions”). These balances arose from the conversion of such transactions into their euro equivalents at the respective currency’s average cost on the balance sheet date, compared with the euro values at which the transactions were initially recorded (see “Off-balance-sheet instruments” in Section 2.3 “Accounting policies”).

The item also includes a lease liability of €175 million (2020: €199 million) (see “Leases” in Section 2.3 “Accounting policies”).

In addition, this item includes the ECB’s net defined benefit liability in respect of the post-employment and other long-term benefits of its staff[40] and the members of the Executive Board, as well as the members of the Supervisory Board employed by the ECB. The termination benefits of ECB staff are also included.

The ECB’s post-employment benefits, other long-term benefits and termination benefits

Balance Sheet

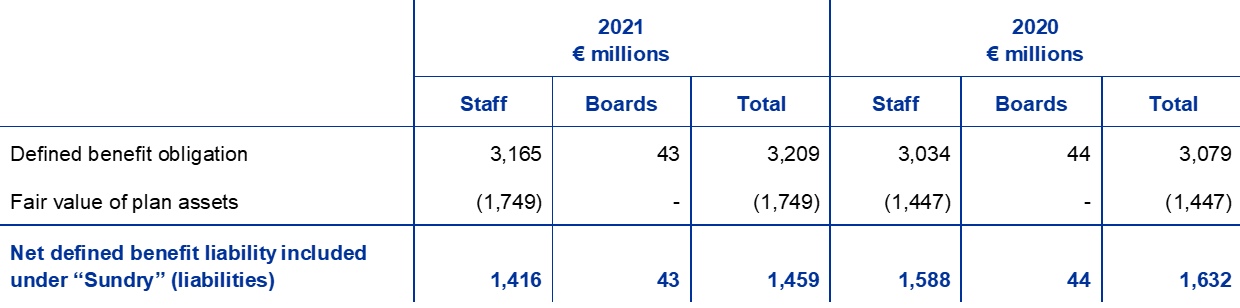

The amounts recognised in the Balance Sheet under the item “Sundry” (liabilities) in respect of post-employment, other long-term and staff termination benefits were as follows:

Note: The columns labelled “Boards” report amounts in respect of both the Executive Board and the Supervisory Board.

In 2021 the present value of the defined benefit obligation vis-à-vis staff of €3,165 million (2020: €3,034 million) included unfunded benefits amounting to €373 million (2020: €364 million) relating to post-employment benefits other than pensions, to other long-term benefits and to staff termination benefits. The present value of the defined benefit obligation vis-à-vis the members of the Executive Board and the members of the Supervisory Board of €43 million (2020: €44 million) relates solely to unfunded arrangements in place for post-employment and other long-term benefits.

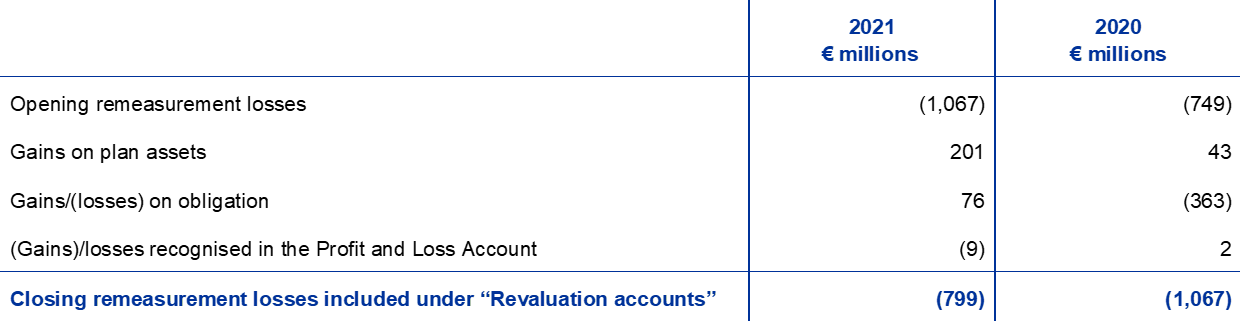

Remeasurements of the ECB’s net defined benefit liability in respect of post-employment benefits are recognised in the Balance Sheet under liability item “Revaluation accounts”. In 2021 remeasurement losses under that liability item amounted to €799 million (2020: €1,067 million) (see note 15 “Revaluation accounts”).

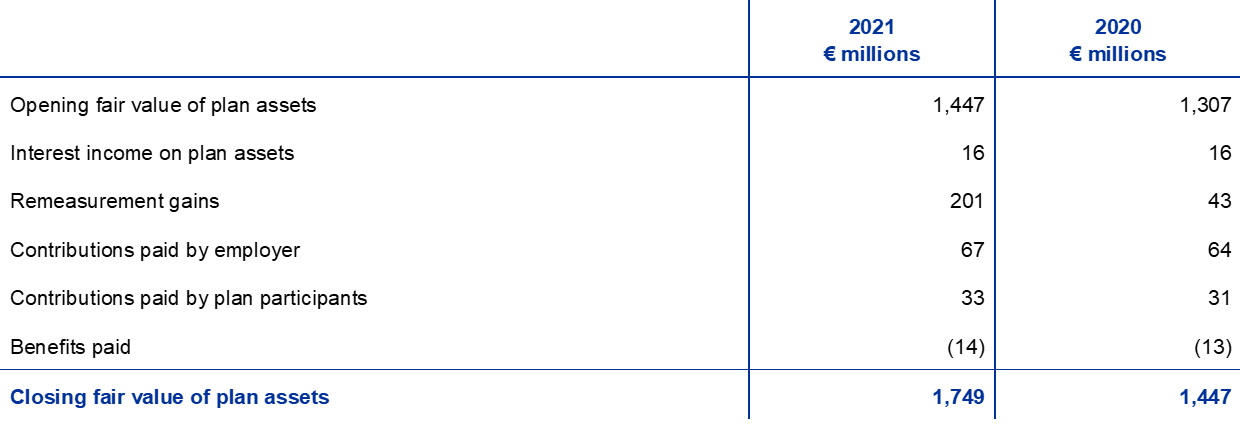

Changes in the defined benefit obligation, plan assets and remeasurement results

Changes in the present value of the defined benefit obligation were as follows:

Note: The columns labelled “Boards” report amounts in respect of both the Executive Board and the Supervisory Board.

1) Net figure including compulsory contributions and transfers into/out of the plans. The compulsory contributions paid by staff are 7.4%, whilst those paid by the ECB are 20.7% of the basic salary.

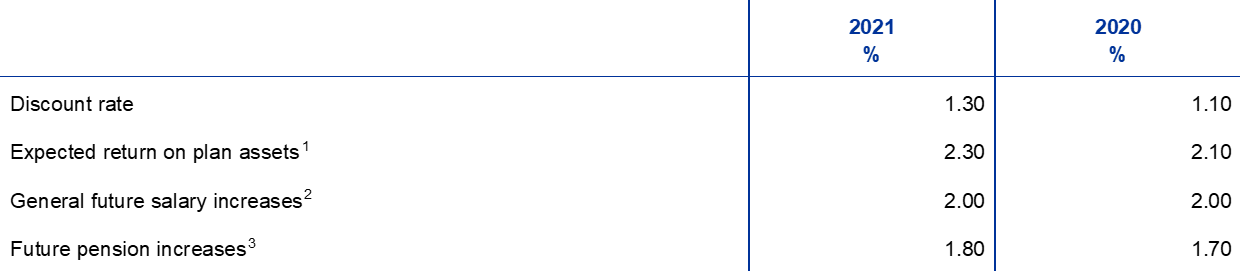

The total remeasurement gains of €76 million on the defined benefit obligation in 2021 arose primarily as a result of the rise in the discount rate used for the valuation from 1.1% in 2020 to 1.3% in 2021. The resulting gains were partially offset by remeasurement losses stemming from experience adjustments reflecting the difference between the actuarial assumptions made in the previous year’s report and actual experience.

Changes in the fair value of plan assets in the defined benefit pillar relating to staff were as follows:

The remeasurement gains on plan assets in 2021 reflected the fact that the actual return on the fund units was higher than the assumed interest income on plan assets, which was based on the discount rate assumption of 1.1%.

Changes in the remeasurement results were as follows:

Profit and Loss Account

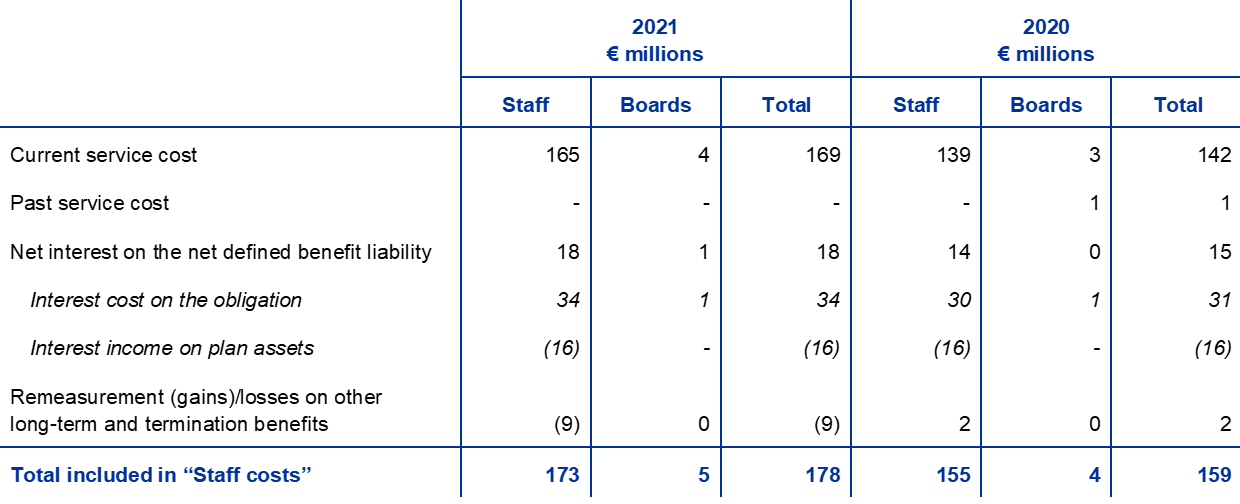

The amounts recognised in the Profit and Loss Account were as follows:

Note: The columns labelled “Boards” report amounts in respect of both the Executive Board and the Supervisory Board.

The current service cost increased in 2021 to €169 million (2020: €142 million), owing mainly to the rise in the future pension increase rate from 1.0% in 2019 to 1.7% in 2020. In addition, the discount rate further decreased from 1.2% in 2019 to 1.1% in 2020.[41]

Key assumptions

In preparing the valuations referred to in this note, the independent actuaries have used assumptions which the Executive Board has accepted for the purposes of accounting and disclosure. The principal assumptions used for the purposes of calculating the liability for post-employment benefits and other long-term benefits are as follows:

1) These assumptions were used for calculating the part of the ECB’s defined benefit obligation which is funded by assets with an underlying capital guarantee.

2) In addition, allowance is made for prospective individual salary increases of up to 1.8% per annum, depending on the age of the plan participants.

3) In accordance with the ECB’s pension plan rules, pensions will be increased annually. If general salary adjustments for ECB employees are below price inflation, any increase in pensions will be in line with the general salary adjustments. If the general salary adjustments exceed price inflation, they will be applied to determine the increase in pensions, provided that the financial position of the ECB’s pension plans permits such an increase.

Note 14 - Provisions