- SPEECH

The rise of non-bank finance and its implications for monetary policy transmission

Speech by Isabel Schnabel, Member of the Executive Board of the ECB, at the Annual Congress of the European Economic Association (EEA)

Frankfurt am Main, 24 August 2021

Introduction

The financial system plays a central role in transmitting monetary policy to the real economy.[1] Whenever a central bank adjusts its policy instruments, it relies on private financial intermediaries to translate the monetary impulse into the financing conditions for firms and households. In today’s speech, I will discuss how this process is shaped by the structure of the financial system and, specifically, by the relative importance of bank versus non-bank finance in the economy.

This question is motivated by the pronounced rise in non-bank financial intermediation in the euro area, especially after the global financial crisis. Non-bank financial intermediaries now make up a much larger share of the financial system than they did in the early years of our common currency. Likewise, a growing number of firms resort to market finance to satisfy their demand for credit. For central banks, it is therefore crucial to understand whether and how these developments matter for the transmission of monetary policy.

I will argue that the rise in non-bank finance is likely to have broadened monetary policy transmission, while it has also created new risks for the conduct of monetary policy.

Specifically, for the euro area as a whole, the increase in non-bank finance seems to have strengthened the impulse of policy measures that work primarily via longer-term interest rates, in particular central bank asset purchases. Yet, as the relative role of bank and non-bank finance varies markedly across countries, sectors and firm sizes, such instruments may affect different parts of the euro area economy unevenly.

Therefore, with the overwhelming majority of euro area firms still relying on bank loans as their prime source of credit, the key ECB interest rates remain the main tool to steer economic conditions in the euro area as the bank lending channel continues to act as the central element of the monetary policy transmission process.

At the same time, the increase in non-bank finance has created new hazards for monetary policy. Non-banks have taken on substantial duration, liquidity and credit risks on their balance sheets. Increased risk-taking, in turn, can give rise to liquidity mismatches and affect the capacity of non-bank financial entities to absorb losses in a downturn, thus potentially creating systemic risk and impairing the monetary policy transmission mechanism. To preserve financial stability and protect policy transmission, the current regulatory landscape needs to better reflect the fact that credit intermediation increasingly takes place outside the banking sector.

The rise in non-bank finance

I would like to highlight three key stylised facts about the development of non-bank financial intermediation in the euro area.

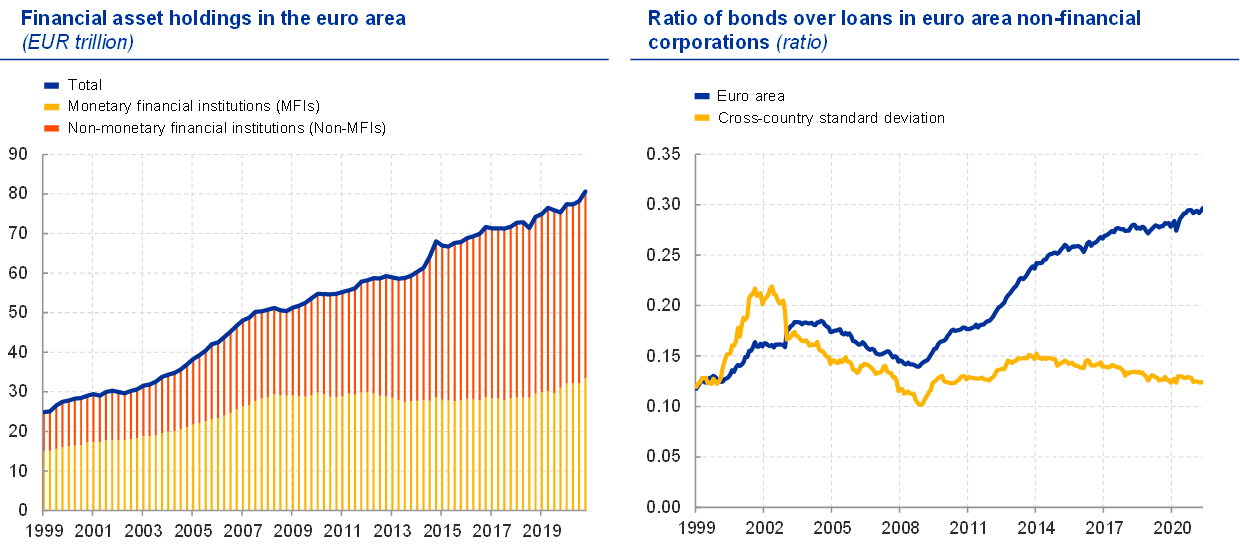

First, based on the evolution of total financial assets, non-bank financial intermediaries – money market funds, investment funds, insurance companies, pension funds and a host of other, more specialised, financial institutions – have become increasingly relevant in the euro area (see Chart 1, left-hand panel).[2]

In the early years of the common currency, the bulk of financial assets were held on the balance sheets of banks. But since the global financial crisis in 2008, the overall growth in financial assets can almost entirely be traced to non-bank entities which by now represent more than half of the total financial asset holdings in the euro area.[3]

A good proportion of the asset growth of non-banks is due to the increased holdings of public sector assets and the growing size of other financial intermediaries (OFIs), some of which may reflect intra-corporate financing. As a consequence, not all of the aforementioned developments necessarily reflect changes in the financing structure of non-financial firms.

Chart 1

Evolution of bank and non-bank finance

Left-hand panel:

Source: Euro area accounts.

Notes: Non-MFIs include insurance companies and pension funds (ICPFs), investment funds (IFs), and other financial intermediaries (OFIs). MFIs exclude the Eurosystem. Calculations based on market values. Latest observations are for Q1 2021.

Right-hand panel:

Sources: ECB (BSI, SEC).

Notes: Data cover non-financial corporations (NFCs); loans and bonds are notional stocks. Cross-country standard deviation is calculated excluding Greece. Latest observations are for May 2021.

But some of them do, which brings me to the second – and closely related – observation: the role of different types of financial instruments has also changed over time. Bank loans clearly remain the dominant debt instrument to finance the corporate sector (see Chart 1, right-hand panel). But corporate bonds have become more relevant since the global financial crisis, with their volume having more than doubled relative to that of bank loans over this period.

However, the use of bonds remains highly uneven across euro area firms. Although the set of issuers has broadened over recent years, with many of the new entrants consisting of smaller and riskier firms, corporate bond markets in the euro area are still mainly populated by larger companies.[4] The euro area is home to some 19 million firms. But there are only around 400 issuers in the euro area whose bonds are eligible for purchases under our corporate sector purchase programme. In total, around 2,000 issuers may currently be active in euro area corporate bond markets, many of whom are non-rated.

In other words, despite the notable rise in bond issuance, the overwhelming majority of euro area firms, in particular small and medium-sized enterprises, still rely on banks for accessing external finance. There is also evidence that firms that have started issuing bonds have often not cut back on their borrowing from banks.[5] So bonds often complement rather than substitute firms’ existing sources of financing their investments.

The third key fact is that financing structures differ across euro area countries (see Chart 1, right-hand panel). While firms in some countries, such as France, make ample use of bond markets, issuance in others, like Spain, remains moderate.[6] The variation of countries’ relative reliance on bond finance has fluctuated widely over time but is now close to the level it was when the euro was introduced (see Chart 1, right-hand panel).

Broadening monetary policy transmission through non-banks

From the ECB’s perspective, it is crucial to understand the impact of the rise and heterogeneity of non-bank finance on the implementation and effectiveness of our single monetary policy, and hence on the transmission of monetary policy.

Early stages of transmission

One reason why the sustained increase in non-bank financial intermediation may indeed matter are systematic differences in the balance sheet structures of banks and non-banks.

Loans make up most of banks’ assets – some 60% – while they only account for under 10% of investment fund assets. Conversely, debt securities play a much larger role for investment funds: approximately 40% of their assets comprise debt securities, compared with around 10% for banks. And, even within asset classes, the composition differs across banks and non-banks, with the bond portfolios of investment funds tending to carry much higher credit and duration risk than those of banks (see Chart 2, left-hand panel).

These differences in balance sheet composition, in turn, may translate into heterogeneous responses to different types of monetary policy measures. For instance, asset purchases tend to exert stronger effects on duration and credit risk premia,[7] whereas policy rate changes have a more direct impact on shorter-term loan market conditions, although they also affect longer-term rates through adjustments in the expected future path of short-term interest rates. Hence, the compositional difference in the balance sheets of banks and non-banks may give rise to different sensitivities to a given type of policy instrument.

Chart 2

Banks versus investment funds

Left-hand panel:

Sources: ECB Securities Holdings Statistics by Sector and ECB calculations.

Note: The latest observations are for Q2 2021.

Right-hand panel:

Source: Cappiello, L., Holm-Hadulla, F., Maddaloni, A., Mayordomo, S., Unger, R. et al. (forthcoming), “Non-bank financial intermediation”, ECB Strategy Review Workstream Report.

Notes: Chart shows the response to monetary policy easing shocks after 12 months, identified via high-frequency surprises in a monthly euro area local projections model, that leads to a 25 basis point decline in interest rates. Dependent variables are total notional stocks of bank assets and investment fund (IF) shares, respectively. Short-rate (long-rate) shocks refer to surprises in the three-month overnight index swap (OIS) rate (ten-year Bund yield). Diamonds are point estimates; whiskers are 90% confidence intervals.

Recent ECB staff analysis has tested this intuition. The analysis is based on a standard empirical framework used to study the transmission of monetary policy, augmented by data on the balance sheet size of banks and investment funds.[8]

The analysis distinguishes between two types of monetary policy shocks. The first is a short-term interest rate shock, which would arise primarily in the context of the ECB adjusting its main policy rates. The second is a longer-term interest rate shock, which would occur in response to the use of other monetary policy measures, such as central bank asset purchases. This differentiation allows us not only to get a sense of the overall transmission implications of non-bank intermediation, but also to assess its ramifications for the relative effectiveness of different types of instruments in the ECB toolkit.

The exercise highlights differential impacts of policy easing shocks across different types of financial intermediaries, as measured by changes in the size of balance sheets (see Chart 2, right-hand panel). The assets of both banks and investment funds expand in response to an accommodative short-rate shock. The size of the response is broadly similar, albeit a little faster for banks and a little larger in aggregate for investment funds.

These findings confirm that the key ECB interest rates remain a powerful policy instrument also in a world in which market-based finance has expanded measurably. By contrast, long-rate shocks transmit quite differently across these two types of intermediaries. Only investment funds appear to be affected in a persistent fashion, whereas the response of banks is short-lived and turns insignificant after a few months.[9]

The uncertainty around these estimates is large, however. For example, earlier findings in the literature suggest that asset purchases incentivise banks to extend credit to the real economy.[10] By reducing the return of risk-free assets, asset purchases may make lending to firms more attractive for banks.

At any rate, these results provide a tentative indication that the rise in non-bank finance has effectively broadened the transmission of monetary policy in the euro area by reinforcing the impulse coming from measures that act directly on the long-term interest rate. This is encouraging news in an environment in which the risk of hitting the zero lower bound, and hence the need to activate asset purchases, has increased.

Later stages of transmission

The balance sheet response of intermediaries is only the first step of the transmission process. What matters most for monetary policy is the impact on the later stages of the transmission process, namely on the economic behaviour of the private sector.

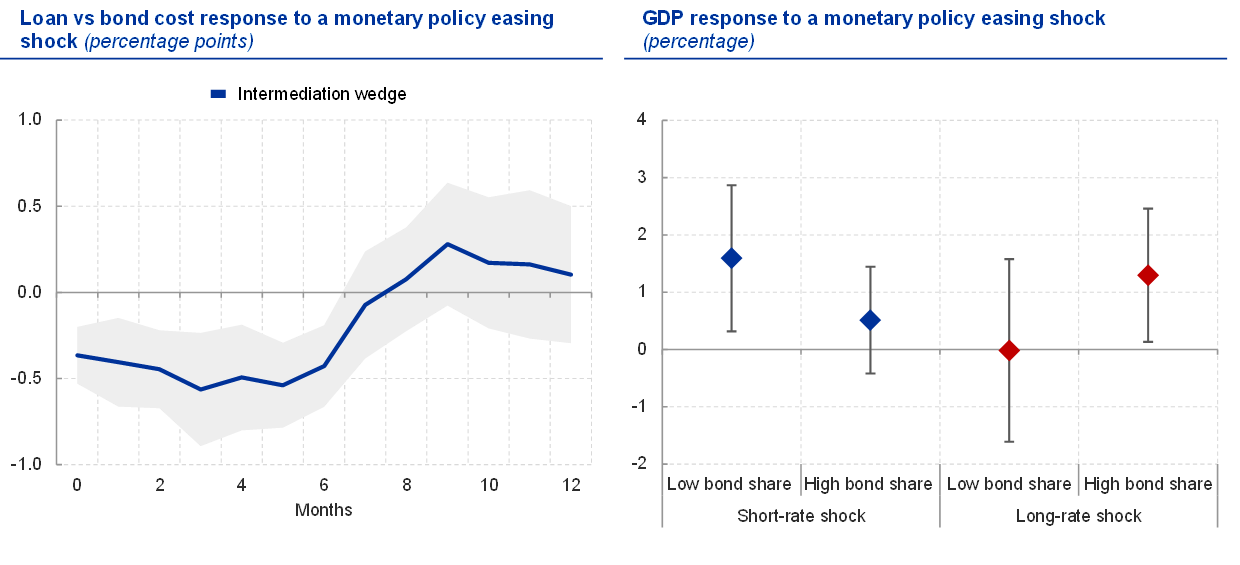

A first important aspect to consider is whether monetary policy triggers different adjustments in the credit conditions prevailing in corporate bond and loan markets. ECB analysis suggests that this is indeed the case (see Chart 3, left-hand panel). In particular, standard monetary policy shocks running through changes in short-term rates have a stronger impact on the rates charged for bank loans than for corporate bonds.[11]

This has important implications for the link between monetary policy and the financing structure of an economy. In primarily bank-based economies, a larger share of corporate debt is remunerated at loan rates rather than bond rates. It follows, then, that the overall cost of credit is more responsive to conventional monetary policy measures in these economies than in economies with a higher share of bond finance.[12]

These changes in credit market conditions appear significant further along the transmission chain (see Chart 3, right-hand panel). The impact of short-rate policy shocks on GDP is much more marked in economies that have more bank-based financial systems, which is in line with other recent findings in the literature. Conversely, when considering shocks to longer-term interest rates, the pattern reverses. Long-rate shocks seem to exert stronger real effects on economies that are more reliant on bond finance.

For the euro area, these findings reinforce the evidence found for the earlier stages of transmission, namely that the key ECB interest rates remain the most important instrument not only for the balance sheet response of financial intermediaries but also for steering the overall path of our economy.[13]

Given the continuing bank-based nature of credit intermediation, these estimates underline the importance of the bank lending channel in the euro area and the instruments we use to protect lending through banks in crisis times, such as our targeted longer-term refinancing operations.

At the same time, it is likely that recent changes in the euro area’s financing structure have strengthened the impact of our asset purchases on real economic activity. A deepening of the capital markets union may reinforce these effects further in the future, and thereby also increase the resilience of policy transmission in the euro area.

This is because a more balanced funding mix is important as a shock absorber, or a “spare tyre” to quote Alan Greenspan.[14] When the global financial crisis and later the sovereign debt crisis hit the euro area, the disproportionate reliance on the banking sector as a source of external finance proved to be a major vulnerability.

A more diverse financial system has the capacity to distribute risk more efficiently. There is evidence that economies with a higher share of bond finance tend to recover faster from recessions.[15] This finding likely reflects the fact that recessions are often followed by long-lasting impairments in banks’ intermediation capacity, which raises the value of bond markets as an alternative source of firm credit.[16]

Chart 3

Monetary policy transmission conditional on debt financing structures

Source: Holm-Hadulla, F. and Thürwächter, C. (2021) “Heterogeneity in corporate debt structures and the transmission of monetary policy”, European Economic Review, Vol. 137.

Notes: Charts show impulse response functions (IRFs) to a monetary policy easing shock, identified via high-frequency surprises in a panel local projections model, using monthly data for euro area countries, that leads to a 25 basis point fall in interest rates. Shocks refer to surprises in the one-month overnight index swap (OIS) rate, except for the “long-rate shock” which refers to five-year Bund yields. Intermediation wedge is the difference between a loan-financing vs bond-financing spread. Bond share is the ratio of bond volume to the sum of bond and loan volumes in non-financial corporation (NFC) sector of each country. Low (high) bond share refers to lower (upper) quintile of cross-country bond share distribution. The range in the left-hand panel denotes the 90% confidence interval. IRFs in the right-hand panel are smoothed. Diamonds are point estimates; whiskers are 90% confidence intervals.

Risks for monetary policy transmission from the rise of non-banks

The increase of non-bank finance may, however, also come with new risks for the monetary policy transmission mechanism. At the heart of these concerns is the question as to whether, and to what extent, monetary policy induces excessive risk-taking by non-banks, thereby potentially becoming a source of financial distress and hampering transmission.

For example, there is evidence that money market funds invest in riskier asset classes when interest rates are low.[17] In the same vein, bond mutual funds reaching for yield appear to generate higher returns and attract more inflows, especially in periods of low-interest rates, but they underperform on a risk-adjusted basis and are exposed to high liquidity risk.[18]

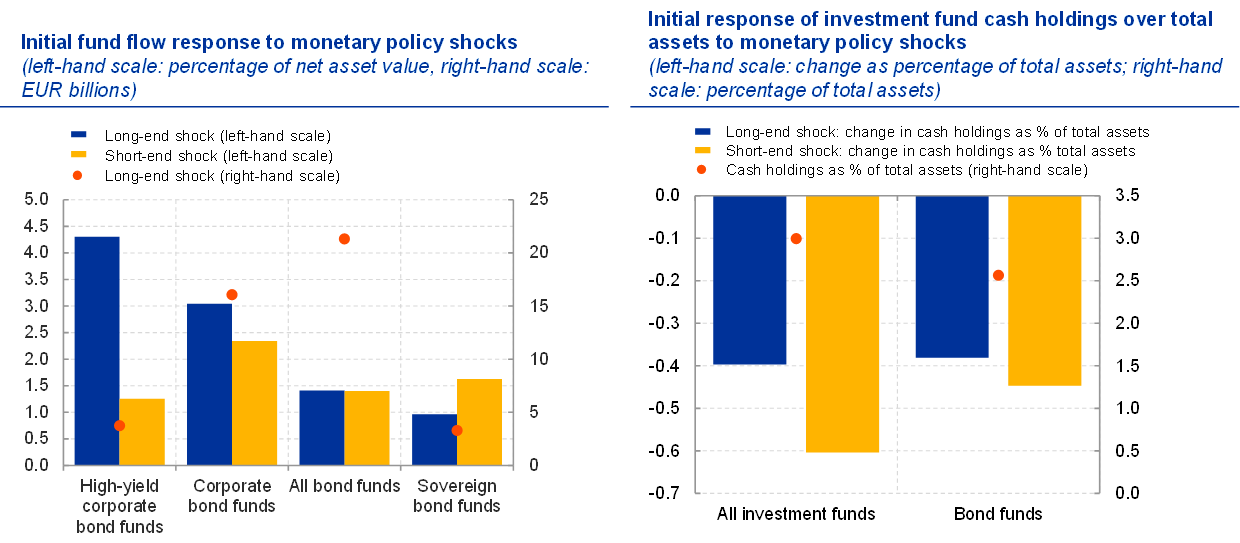

Recent ECB research suggests that incentives for investors to take on risk may differ with the choice of the policy instrument. Asset purchases, which leave their strongest footprint at the long end of the yield curve, are typically associated with persistent net inflows into bond investment funds, with the inflows being larger for riskier fund types (see Chart 4, left-hand panel).[19] There is less evidence of higher risk-taking by investors following shocks to the short-end of the yield curve.

Asset managers also persistently reduce fund cash holdings following expansionary monetary policy shocks, with changes in short-term rates having a stronger impact on funds’ cash holdings than shocks to long-term rates (see Chart 4, right-hand panel). If such reductions are sizeable, low liquidity holdings and the corresponding liquidity mismatch leave funds vulnerable to large outflows during periods of stress.

Chart 4

Investment fund risk-taking

Source: Giuzio, M., Kaufmann, C., Ryan, E., and Cappiello, L. (2021, forthcoming), “Investment funds, risk-taking, and monetary policy in the euro area”, Working Paper Series, ECB.

Notes: Estimates in both panels are based on a Bayesian vector autoregression (BVAR) model using monthly data between April 2007 and June 2019. Monetary policy shocks are identified using an adapted version of the method in Jarociński, M. and Karadi, P. (2020), “Deconstructing monetary policy surprises – the role of information shocks”, American Economic Journal: Macroeconomics, Vol. 12, No 2, American Economic Association, April, pp. 1-43, and using data provided by Altavilla, C., Brugnolini, L., Gürkaynak, R., Motto, R. and Ragusa, G. (2019), “Measuring euro area monetary policy”, Journal of Monetary Economics, Vol. 108, December, pp. 162-179. The model includes the five-year Bund yield, the five-year euro area NFC bond spread, the EURO STOXX index and its volatility (VSTOXX). The left panel shows the median impulse response function (IRF), with areas shaded blue (grey) denoting 68% (90%) credibility intervals after a monetary policy shock equivalent to a 25 basis point reduction of the five-year euro area risk-free rate. The right panel shows the first-month response for different fund types. The monetary policy shocks are equivalent to a 25 basis point reduction in the five-year euro area risk-free rate for long-end shocks and in the three-month overnight index swap (OIS) for short-end shocks. Flows examined are to funds with euro area domicile and European investment focus.

The market turbulence in March 2020 vividly illustrated that investment funds can be subject to runs in the form of large investor redemptions, leading to fire sales and thus exacerbating market disruptions through self-reinforcing price spirals. Investment funds shed assets on a large scale and this sell-off was much larger than the outflows they were facing.

Recent analysis shows that less regulated investment funds tended to engage in more procyclical selling and cash hoarding than more strictly regulated funds classified as undertakings for the collective investment in transferable securities (UCITS).[20] While it can be individually rational for fund managers to sell assets in excess of current outflows when uncertainty about future redemptions is high, such cash hoarding can be detrimental to wider financial stability.

The ECB’s monetary policy interventions in the wake of the unfolding coronavirus (COVID-19) pandemic were successful in preserving financial stability in the euro area.[21] But the success of the ECB’s interventions in that particular episode should not distract from the fact that the underlying vulnerabilities in the non-bank sector need a structural fix, not least to mitigate the risk of moral hazard.

Macroprudential policies need to be significantly enhanced to address the structural vulnerabilities exposed by the market turmoil of March 2020, in particular with respect to liquidity mismatches in money market and investment funds. The Financial Stability Board (FSB) is expected to soon issue recommendations aimed at both strengthening the resilience of the non-bank financial sector and ensuring a globally consistent approach to policy reforms, drawing from the ongoing FSB work on money market funds, open-ended investment funds and margining practices.

Conclusion

Let me conclude.

The euro area remains a bank-based economy, but the rising prominence of non-bank finance has important ramifications for the transmission of monetary policy.

Although significant cross-country heterogeneities in financing structures persist in the euro area, the rise in non-bank finance has strengthened policy transmission through capital markets. However, this also comes with new risks that may impair policy transmission in periods of financial stress. The current macroprudential policy framework needs to be developed further with a view to strengthening the ability of authorities to limit the build-up of systemic risk in the non-bank financial sector and curb stress, if and when it arises.

Despite the relevance of these questions for policy conduct in the euro area, the academic literature on non-bank finance and monetary policy is still nascent, and I see substantial scope for insightful research to be devoted to this topic in the future.

Thank you.

- I would like to thank Fédéric Holm-Hadulla and Miles Parker for their contributions to this speech.

- See European Central Bank (2016), “The role of euro area non-monetary financial institutions in financial intermediation”, Economic Bulletin, Issue 4.

- Part of this increase is due to valuation gains but, also based on notional stocks (which net out these valuation gains), non-banks have clearly become more relevant relative to banks since the great financial crisis; see Cappiello, L., Holm-Hadulla, F., Maddaloni, A., Mayordomo, S., Unger, R. et al. (forthcoming), “Non-bank financial intermediation”, ECB Strategy Review Workstream Report.

- Darmouni, O. and Papoutsi, M. (2021), “The rise of bond financing in Europe”, paper presented at the ECB-RFS Macro-Finance Conference, March.

- ibid.

- In part, these differences reflect the size distribution of companies. In some countries, the corporate structure is tilted towards small and medium-sized companies, which tend to face higher barriers to access bond markets; see Cappiello, L., Holm-Hadulla, F., Maddaloni, A., Mayordomo, S., Unger, R. et al. (forthcoming), “Non-bank financial intermediation”, ECB Strategy Review Workstream Report.

- See Vayanos, D., and Vila, J. L. (2021), “A preferred-habitat model of the term structure of interest rates”, Econometrica, Vol. 89, No 1 and Altavilla, C., Carboni, G., and Motto, R. (2021, forthcoming), “Asset purchase programmes and financial markets: evidence from the euro area”, International Journal of Central Banking.

- See Cappiello, L., Holm-Hadulla, F., Maddaloni, A., Mayordomo, S., Unger, R. et al. (forthcoming), “Non-bank financial intermediation”, ECB Strategy Review Workstream Report. The focus of the analysis on investment funds is motivated by the finding that they represent the non-bank financial intermediaries whose role has expanded most over the past decade and a half.

- For the full profile of the results, see Cappiello, L., Holm-Hadulla, F., Maddaloni, A., Mayordomo, S., Unger, R. et al. (forthcoming), “Non-bank financial intermediation”, ECB Strategy Review Workstream Report. Since the analysis uses notional stocks for balance sheet size, the differences in the responses between the two intermediary types do not appear to be driven by differences in valuation effects between loans and bonds.

- See, for example, Altavilla, C., Canova, F., and Ciccarelli, M. (2020), “Mending the broken link: Heterogeneous bank lending rates and monetary policy pass-through”, Journal of Monetary Economics, Vol. 110, pp. 81-98 and Albertazzi, U., Becker, B., and Boucinha, M. (2020), “Portfolio rebalancing and the transmission of large-scale asset purchase programs: Evidence from the euro area”, Journal of Financial Intermediation, in press; and Betz, F., and De Santis, R. A. (2021, forthcoming), “ECB corporate QE and the loan supply to bank-dependent firms”, International Journal of Central Banking.

- In addition, the more muted response in economies with a high share of bond finance derives from composition effects: firms in these economies have greater scope to adjust their financing structure by substituting between loans and bonds, depending on each instrument’s relative cost. See Kashyap, A.K. and Stein, J.C. (1994), “Monetary policy and bank lending”, in Mankiw, N.G. (Ed.), Monetary Policy, The University of Chicago Press, Chicago, pp. 221-261, and Kashyap, A. K., Stein, J.C. and Wilcox, D.W. (1993), “Monetary Policy and Credit Conditions: Evidence from the Composition of External Finance”, American Economic Review, Vol. 83, No 1, pp. 78-98.

- See Holm-Hadulla, F. and Thürwächter, C. (2021), “Heterogeneity in corporate debt structures and the transmission of monetary policy”, European Economic Review, Vol. 137. For empirical evidence of a substitution from bank loans to bonds at times of tight monetary policy, see Ivashina, V. and Becker, B. (2014), “Cyclicality of credit supply: Firm level evidence”, Journal of Monetary Economics, Vol. 62, pp. 76-93.

- See Holm-Hadulla, F. and Thürwächter, C. (2021), “Heterogeneity in corporate debt structures and the transmission of monetary policy”, European Economic Review, Vol. 137.

- See Greenspan, A. (1999), “Do efficient financial markets mitigate financial crises?”, speech before the 1999 Financial Markets Conference of the Federal Reserve Bank of Atlanta, Sea Island, Georgia, 19 October.

- Grjebine, T., Szczerbowicz, U. and Tripier, F. (2018), “Corporate debt structure and economic recoveries”, European Economic Review, Vol. 101, pp. 77-100.

- Further evidence shows that companies eligible for the ECB's corporate bond purchase programme significantly increased their investment in research and development, particularly those with low leverage and high prior innovation, although not those with low cash flow or dividend pay-out ratio. See Grimm, N., Laeven, L. and Popov, A. (2021, forthcoming), “Quantitative easing and corporate innovation”, Working Paper Series, ECB.

- Di Maggio, M. and Kacperczyk, M. (2017), “The unintended consequences of the zero lower bound policy”, Journal of Financial Economics, Vol. 123, No 1, pp. 59-80.

- Choi, J. and Kronlund, M. (2017), “Reaching for yield in corporate bond mutual funds”, The Review of Financial Studies, Vol. 31, No 5, pp. 1930-1965.

- See Giuzio, M., Kaufmann, C., and Ryan, E. (2021), “Investment fund flows, risk-taking and monetary policy”, Financial Stability Review, Box 5, ECB, May, pp. 74-77.

- See Schnabel, I. (2020), “COVID-19 and the liquidity crisis of non-banks: lessons for the future”, speech at the Financial Stability Conference on “Stress, Contagion, and Transmission” organised by the Federal Reserve Bank of Cleveland and the Office of Financial Research, Frankfurt am Main, 19 November; Cera, K., Fache Rousová, L., Ghiselli, A., Kaufmann, C. and O’Sullivan, S. (2021), “Investment funds’ procyclical selling and cash hoarding: a case for strengthening regulation from a macroprudential perspective”, Financial Stability Review, Box 6, ECB, May, pp. 88–90. The classification of funds as UCITS and non-UCITS depends on whether they fall under Directive 2009/65/EC of the European Parliament and of the Council of 13 July 2009 on the coordination of laws, regulations and administrative provisions relating to undertakings for collective investment in transferable securities (UCITS) (OJ L 302 17.11.2009, p. 32). UCITS funds are mutual funds that can be sold to retail investors and are perceived as non-speculative, diversified and well-regulated investments.

- Breckenfelder, J., Grimm, N. and Hoerova, M. (2021, forthcoming), “Do non-banks need access to the lender of last resort? Evidence from mutual fund runs”, Working Paper Series, ECB.

Banque centrale européenne

Direction générale Communication

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Allemagne

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction autorisée en citant la source

Contacts médias- 24 August 2021